Running a Business in Colorado Is a Real Thing

Colorado’s business environment is genuinely good. Low unemployment, a growing population, a strong outdoor economy, a booming tech sector along the Front Range — the state has a lot going for it. And with all of that growth comes a lot of small and mid-size business owners who are figuring out insurance for the first time or realizing their current coverage doesn’t quite fit anymore.

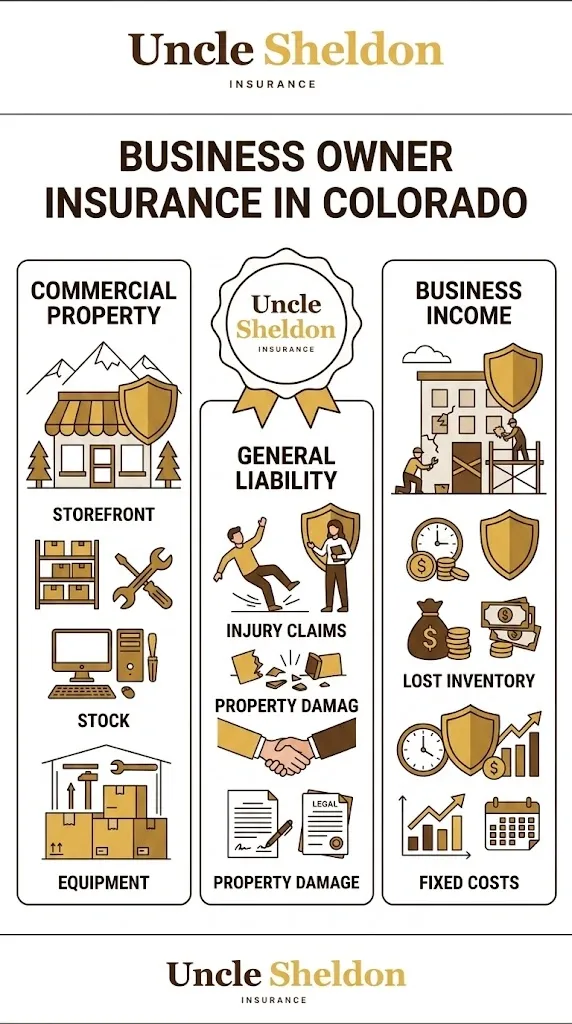

A Business Owner Policy — most people call it a BOP — is the foundation for most small business coverage. It bundles general liability and commercial property into one policy, and usually includes business interruption coverage as well. That package handles a lot of the basic risks: a customer slips and falls in your store, a fire damages your equipment, a covered event shuts you down for six weeks. The BOP is where most Colorado business owners start.

But Colorado has some specific wrinkles that a generic online quote doesn’t always account for. Wildfire exposure affects commercial property rates in a big way across the state. Hail on the Front Range can damage storefronts, outdoor equipment, and vehicles. Seasonal businesses that depend on snowpack or tourist traffic have interruption risk that looks different from a year-round suburban retail store. And Colorado has a few industries — craft beer, outdoor recreation, cannabis, construction — that need specialized coverage most standard BOPs don’t fully address.

At Uncle Sheldon, we’re an independent agency. We work with multiple carriers, we don’t have a single product to push, and we have real agents who actually explain what you’re buying. That’s the whole point of working with us.

What a Business Owner Policy Covers

Before getting into the city breakdown, here’s what’s typically inside a standard BOP and what each piece actually does.

General Liability covers your business if a third party — a customer, a vendor, someone walking by — is injured on your premises or as a result of your operations. It also covers property damage you accidentally cause to someone else’s stuff and advertising injury claims like copyright infringement or defamation. This is the coverage most landlords require before they’ll let you sign a commercial lease.

Commercial Property covers the physical stuff your business owns or is responsible for — your building if you own it, your equipment, your inventory, your furniture, your signage. It also covers improvements you’ve made to a leased space. Standard commercial property covers fire, theft, vandalism, and some weather events. Flood and earthquake are almost always excluded and require separate policies.

Business Interruption kicks in when a covered event forces your business to close or reduce operations. If a fire damages your shop and you have to shut down for three months, business interruption helps replace lost income and covers ongoing expenses like rent and payroll. In Colorado, where natural disasters can genuinely close a business for an extended period, this piece of the policy is not optional in our opinion.

| Coverage | What It Protects | Common Exclusions |

|---|---|---|

| General Liability | Customer injuries, property damage, advertising claims | Professional errors, auto accidents, intentional acts |

| Commercial Property | Building, equipment, inventory, tenant improvements | Flood, earthquake, employee theft (needs separate endorsement) |

| Business Interruption | Lost income, ongoing expenses during closure | Utilities outage only (needs endorsement), flood, earthquake |

| Medical Payments | Minor injuries to customers regardless of fault | Employee injuries (workers’ comp handles those) |

Beyond the core BOP, many Colorado businesses need additional coverage that isn’t bundled in by default. Professional liability (errors and omissions) for consultants, accountants, and real estate professionals. Cyber liability for any business handling customer data. Commercial auto if your team drives for work. Workers’ compensation, which is required in Colorado for any business with employees. Liquor liability if you serve alcohol. The list varies by what you actually do.

Colorado-Specific Business Risks Worth Knowing About

There are a few things about doing business in Colorado that are different from most other states. Some of them affect your coverage options and pricing in ways that aren’t immediately obvious.

Wildfire is the big one. Colorado has seen some of the most destructive wildfires in state history over the past decade — the Marshall Fire, the Cameron Peak Fire, the East Troublesome Fire. Commercial property near the wildland-urban interface can be harder to insure, and rates have climbed in affected counties. If your business is located in a fire-prone area, getting the right coverage may take more effort than a standard quote tool can handle.

Hail hits the Front Range hard every summer. Denver, Aurora, Colorado Springs, Pueblo — this corridor sits in what’s sometimes called Hail Alley. Commercial roofs, outdoor signage, equipment stored outside, and storefronts with large windows all take hits. Making sure your commercial property coverage includes hail and that you understand your deductible structure is important for Front Range businesses.

Altitude and Outdoor Operations — Colorado businesses that operate outdoors, guide trips, run adventure tourism, or manage resort-adjacent services face a set of liability exposures that don’t exist most places. High altitude activities, extreme weather, remote terrain — these all affect general liability underwriting.

Seasonal Revenue — A lot of Colorado businesses depend on ski season, summer tourism, or outdoor recreation in ways that create real business interruption exposure. A bad snow year in Aspen or Telluride affects every restaurant, shop, and rental operation in town. A summer wildfire closing a national park corridor can gut the season for Estes Park businesses. Standard business interruption that doesn’t account for this kind of seasonal exposure isn’t doing the job.

Cannabis Industry — Colorado was the first state to legalize recreational cannabis and the industry is large. However, cannabis businesses face significant insurance challenges because federal classification creates problems with most standard carriers. BOPs for dispensaries, cultivators, and distributors exist but require specialized insurers. Uncle Sheldon can help navigate this — it’s not the kind of thing a standard online quote handles.

Denver

Denver is the engine of Colorado’s economy. Over 700,000 people in the city proper, and the metro area pushes past three million. The business landscape is as diverse as you’d expect from a major American city — tech, healthcare, professional services, retail, hospitality, construction, energy, and more.

Business owners in Denver operate in one of the more competitive commercial insurance markets in the Mountain West. The good news is that competition means options. The challenge is knowing which carriers actually write the class of business you’re in at rates that make sense.

Denver’s core commercial districts — downtown, the RiNo Arts District, Baker, Cherry Creek, LoHi — vary significantly in terms of commercial property risk. Older buildings in denser neighborhoods have different property profiles than new construction in developing corridors. Retail operations in high foot-traffic areas have different liability exposure than professional offices.

Hail is a real issue in Denver. The city has been hit by costly hailstorms that have damaged commercial roofs and outdoor equipment. Business owners with outdoor seating, signage, or rooftop equipment should specifically ask about hail coverage when reviewing their policy.

Aurora

Aurora is one of Colorado’s most economically diverse cities and has a large small-business community that reflects its population. A huge range of businesses call Aurora home — restaurants, medical offices, auto shops, retail, personal services, logistics, and more.

Commercial property in Aurora ranges widely in age and condition. Some of the older commercial strips have buildings that are more expensive to insure or that have had prior claims. Businesses leasing in older strip malls or commercial corridors should make sure their tenant improvements and betterments are included in their property coverage — landlords’ policies typically don’t cover what you’ve built out inside the space.

Aurora sits in hail territory, same as Denver. Outdoor equipment, signage, and vehicles are all exposure points.

Fort Collins

Fort Collins has one of the more entrepreneurial small business cultures in Colorado. Colorado State University drives a lot of it — graduate students and faculty starting companies, the agricultural innovation sector around CSU, the craft beer industry (Fort Collins is legitimately one of the craft beer capitals of the country), and a strong outdoor and recreation economy.

Breweries and taprooms need more than a standard BOP. Liquor liability is a significant piece, equipment for brewing is specialized (and expensive), and if you have a taproom with seating and events, your liability exposure is different from a standard retail operation. Fort Collins has enough breweries that local agents are familiar with what the right policy looks like.

Retail and restaurant businesses along College Avenue and Old Town need liability coverage appropriate for high foot-traffic operations, and business interruption that accounts for the seasonal nature of some of that foot traffic.

Lakewood

Lakewood is a large Denver suburb with a significant commercial base — retail, medical offices, professional services, restaurants, and personal services are all well-represented. The Belmar district has become a genuine urban hub and has attracted a range of local businesses.

For business owners in Lakewood, a standard BOP is usually the right starting point. The wildfire risk increases as you move toward the foothills in the western parts of the city, and businesses in those areas should make sure their commercial property coverage reflects that.

Thornton

Thornton is a northern Denver suburb that has seen steady population growth. Its commercial sector is a mix of retail, food service, construction, and service businesses. Rents are generally lower than Denver proper, which attracts small business owners looking to minimize overhead.

Business interruption coverage is worth thinking about for Thornton businesses that depend on steady foot traffic — because the city’s commercial corridors can feel the impact of larger regional disruptions. Hail is a factor here as well.

Westminster

Westminster sits on the US-36 corridor between Denver and Boulder. It has a diverse commercial economy with strong retail anchors, restaurant clusters, and a growing professional services sector. The Orchard Town Center area has become a significant commercial destination.

For Westminster business owners, the BOP conversation is fairly standard Front Range stuff — hail, property coverage, general liability for customer-facing operations. Businesses in newer commercial construction may find more favorable property rates than those in older strip mall settings.

Arvada

Arvada is a northwest Denver suburb with a revitalized downtown in Olde Town and a strong small business community. The city has invested significantly in walkable commercial development, and local retail and restaurant businesses have benefited.

Business owners in Arvada who lease in older commercial buildings should pay attention to the building’s loss history and the condition of the roof — insurers look at both when writing commercial property. Liquor liability is relevant for any Arvada business that serves alcohol, and Olde Town has a good number of them.

Centennial

Centennial is an affluent southeastern Denver suburb with a strong professional services and tech presence driven by proximity to the Denver Tech Center. Medical offices, law firms, financial advisors, consultants, and corporate offices are common here.

For Centennial professional services businesses, professional liability is just as important as general liability — sometimes more so. A BOP gives you the property and GL foundation, but a standalone E&O policy is often the real risk management tool for this type of business. Cyber liability is also very relevant given the amount of client data these businesses handle.

Pueblo

Pueblo is Colorado’s steel city — an industrial heritage that shaped the community and still defines part of its character. The business landscape is a mix of manufacturing, trades, retail, and services. It’s a more affordable market than the Front Range metros, and small businesses operating here often have lower overheads but also tighter margins.

Wind and hail are real factors in Pueblo. The city sits in an area that gets significant weather, and commercial roofs and outdoor equipment take damage. Business owners who operate in older commercial buildings should get a property valuation that actually reflects replacement cost — not just market value, which can be very different for Pueblo commercial real estate.

Grand Junction

Grand Junction is the economic hub of the Western Slope. Energy, agriculture, retail, healthcare, and government are all significant employers. The business climate here is distinct from the Front Range — more conservative, more tied to resource industries, and with its own set of insurance considerations.

Wildfire is a major risk on the Western Slope and has affected communities in Mesa County. Commercial properties in more rural settings or near open land need proper coverage, and some carriers are more comfortable writing in fire-prone areas than others. Working with an independent agent who has access to multiple carriers is genuinely useful in this market.

Grand Junction also has a growing retail and services economy as the region’s population has grown. Standard BOPs are available and appropriate for most of these businesses.

Aspen

Aspen is in its own category. The cost of doing business here is among the highest in Colorado, and the type of businesses operating in Aspen skews heavily toward luxury retail, high-end restaurants, hospitality, real estate, and resort-adjacent services.

Commercial property values in Aspen are extremely high, and replacement costs for build-outs in premium commercial spaces can be significant. Business owners leasing in Aspen need to make sure their coverage reflects what it would actually cost to rebuild their space and replace their equipment — and that number is usually higher than it seems.

Seasonal revenue concentration is a real issue in Aspen. If your business does 60% of its annual revenue in ski season and something happens in December, business interruption coverage matters a lot. Understanding how your BI coverage calculates lost income — based on historical revenue, projected revenue, or a fixed amount — is something to nail down with your agent before you need it.

Events are a significant part of the Aspen business calendar — from the food and wine festivals to music festivals to corporate retreats. If your business is involved in event production, catering, or event services, your general liability needs to reflect that work.

Vail

Vail’s commercial environment is shaped almost entirely by the ski industry and its related tourism economy. Restaurants, ski shops, hospitality businesses, rental operations, retail boutiques, and real estate offices — these are the core of Vail’s commercial landscape.

Ski and outdoor equipment retail and rental businesses have specific inventory and liability needs. High-value inventory that moves in and out seasonally, equipment that gets used by customers in high-risk conditions, and the liability exposure of fitting and renting gear to skiers — these all factor into the right coverage structure.

Businesses in Vail that depend on ski season traffic need to think hard about business interruption and what triggers it. A low-snow year doesn’t trigger BI. A covered event like a fire does. Understanding the difference and whether your policy has any provisions for extended coverage is the kind of conversation worth having with a real agent.

Breckenridge

Breckenridge has a strong year-round tourism economy built around skiing, summer hiking and cycling, and events throughout the year. The business community is a mix of local operators who’ve been there for decades and newer entrants drawn by the mountain lifestyle.

Commercial property in Breckenridge and Summit County has gotten more expensive to insure as wildfire risk awareness has increased. Mountain town properties also face snow load risks — roofs built for mountain conditions are the norm, but older commercial buildings can have structural vulnerabilities that affect underwriting.

Restaurants and bars in Breckenridge do significant volume and need appropriate general liability and liquor liability coverage. Food service is one of those categories where coverage gaps — like inadequate products liability or insufficient per-occurrence limits — show up at the worst possible times.

Telluride

Telluride might be the most remote major resort in Colorado. Getting there requires either a long drive or a flight into a high-altitude regional airport. That remoteness shapes the business community — businesses that operate in Telluride tend to be deeply committed to the town, and competition is limited by geography.

Like Aspen, commercial costs in Telluride are high. Commercial property values reflect the market, and replacement costs for premium build-outs are significant. Business interruption exposure is concentrated around the ski season, the summer festival season (Telluride hosts major film and music festivals), and the periods between.

Any Telluride business that runs or participates in outdoor events should review their general liability carefully. Festival environments, outdoor venues, and high-altitude conditions create specific liability exposures that standard BOPs don’t always address fully.

Estes Park

Estes Park is the gateway to Rocky Mountain National Park, and its business community exists almost entirely to serve visitors. Retail, restaurants, lodging, outdoor outfitters, guided experiences, and services for the roughly four million people who visit RMNP each year — that’s the Estes Park economy.

The seasonal concentration of revenue here is extreme. A summer that gets disrupted — by wildfire, by road closures, by flood, by a global event — can be devastating for Estes Park businesses. The 2013 Colorado floods hit this area hard. The Cameron Peak Fire and other recent fires have at various points affected access and air quality.

Business interruption coverage for Estes Park businesses needs to be evaluated carefully. Access disruption — like a closed highway — may not trigger standard BI. Civil authority coverage, which kicks in when government orders prevent access to your business, is worth asking about specifically.

Outdoor guiding and adventure businesses operating near RMNP also need liability coverage appropriate for their operations. Standard BOPs can cover some of this, but the specific activities and environments involved often need endorsements or specialty policies.

Steamboat Springs

Steamboat has a personality all its own — agricultural roots, a legitimate ranching tradition, a world-class ski resort, and a community that’s been there long enough to have opinions about how things should be done. The commercial mix reflects all of that: ag services, outdoor recreation businesses, hospitality, retail, and real estate.

Agricultural and ranching-adjacent businesses have insurance needs that go beyond a standard BOP. Farm equipment, livestock, outbuilding coverage, and the specific liability of operating on large tracts of land all factor in. If your business intersects with agriculture at all in Routt County, it’s worth a conversation with an agent who understands that sector.

For ski-season and tourism businesses in Steamboat, the seasonal concentration risk and wildfire risk considerations are similar to other mountain resort towns. Rates here have historically been a bit more reasonable than in the Aspen/Vail/Breckenridge corridor.

Durango

Durango is a college town, a mountain town, a Four Corners hub, and a genuinely livable city that’s attracted a lot of small business owners over the years. Fort Lewis College drives part of the economy, outdoor recreation drives another part, and tourism from the Durango and Silverton Narrow Gauge Railroad and surrounding public lands rounds it out.

Wildfire in the San Juan Mountains area is a serious and recurring concern. Durango and La Plata County have seen significant fire activity. Commercial property here — especially properties near forested areas or on the outskirts of town — needs coverage that accounts for that risk. Some carriers have pulled back from writing commercial property in fire-exposed Colorado counties, which is exactly why having an independent agent who can shop across multiple carriers matters.

Outdoor recreation businesses operating out of Durango — guides, outfitters, equipment rental operations — need to pay attention to their general liability and what activities are specifically covered. High-risk outdoor activities can require specialty coverage or endorsements.

Glenwood Springs

Glenwood Springs sits at a critical point along I-70 and is a destination in its own right — the hot springs, the canyon, Glenwood Caverns, and its position as a gateway to Aspen and the Roaring Fork Valley. It’s a hub for both tourism businesses and businesses that serve the surrounding regional economy.

The Grizzly Creek Fire in 2020 closed Glenwood Canyon and I-70 for weeks, which affected businesses up and down the corridor. Access disruption as a business risk is very real in Glenwood Springs — it’s a town where road closures due to fire, rockslides, or weather can cut off customer access entirely.

Commercial property in Glenwood Springs sits in a canyon environment with its own set of risks — rockfall exposure in some areas, flood history from the Colorado River, and wildfire risk. Property underwriting here is not always straightforward.

What Colorado Business Owners Often Get Wrong About Their Coverage

A few things come up consistently when we talk to Colorado business owners about their insurance. Not because people are careless — it’s usually because nobody explained it clearly upfront.

Underinsuring commercial property. The most common mistake we see is business owners insuring their commercial property for market value or purchase price rather than replacement cost. In a market like Colorado where construction costs have risen significantly over the past several years, there can be a big gap between what you paid for your build-out and what it would cost to rebuild it today. If your policy has a coinsurance clause and you’re underinsured, you may not receive a full payout even for a partial loss.

Assuming the landlord’s insurance covers you. It doesn’t. A commercial landlord’s policy covers the building. It doesn’t cover your equipment, your inventory, your tenant improvements, or your loss of income. Your lease may even hold you responsible for damage you cause to the building. Your own BOP is what protects you.

Skipping business interruption or buying too little. Business interruption coverage is often where the real argument happens after a claim. The question of how your BI limit was calculated — and whether it actually reflects your real revenue exposure — matters a lot. A policy with a 30-day waiting period and a 6-month max payout may not be enough for a Colorado business that gets shut down by a major wildfire or a severe weather event.

Not reviewing coverage as the business changes. A policy that was right for your business two years ago may be significantly wrong now if you’ve added employees, expanded locations, changed what you do, or grown revenue substantially. Coverage gaps created by growth are one of the most avoidable problems we see.

| Common Gap | What It Costs You | How to Fix It |

|---|---|---|

| Underinsured property | Partial payout on a full loss | Replacement cost appraisal, adequate limits |

| No BI coverage | Zero income during closure | Add business interruption to BOP |

| Missing professional liability | Defense costs and settlements out of pocket | Add E&O policy |

| No cyber coverage | Data breach response costs, regulatory fines | Add cyber endorsement or standalone policy |

| Excluded wildfire in fire zones | Full property loss with no payout | Work with a carrier who writes the zone |

| No liquor liability for events | Uncovered claims from alcohol-related incidents | Add liquor liability endorsement |

Business Owner Insurance Cost Ranges in Colorado

Pricing varies significantly based on business type, location, revenue, number of employees, and the specific risks involved. The table below gives a general sense of what different types of Colorado businesses might expect to pay.

| Business Type | Estimated Annual BOP Cost | Key Factors |

|---|---|---|

| Small retail shop (Front Range) | $800 to $2,500 | Square footage, inventory value, hail exposure |

| Restaurant or bar | $2,000 to $6,000+ | Revenue, liquor liability, square footage, location |

| Office or professional services | $500 to $1,500 | Square footage, professional liability needs |

| Contractor or trades business | $1,500 to $5,000+ | Payroll, type of work, equipment value |

| Outdoor recreation / guiding | $1,500 to $4,000+ | Activities covered, participant volume |

| Mountain resort area business | $1,500 to $5,000+ | Property value, seasonal revenue, wildfire zone |

| Brewery or taproom | $2,500 to $7,000+ | Equipment, liquor liability, event coverage |

These are rough ranges. Your actual quote depends on the specifics of your situation, and the only way to know is to go through the process with a real agent.

Working With Uncle Sheldon on Business Owner Insurance in Colorado

Uncle Sheldon is an independent agency. That means we represent multiple carriers — we’re not tied to one company’s products. When we look at your business, we look for the carrier that’s actually the right fit for your industry, your location, and your coverage needs.

Colorado is a state we know. We understand why a Boulder tech startup has different needs than a Steamboat Springs outfitter or an Aspen restaurant. We’re not going to hand you a generic policy and call it done.

Our agents are real people. They’ll ask you questions about your business, help you think through coverage gaps you might not know you have, and explain things in plain language. You’re not going to get a chatbot or an algorithm — you’re going to get someone who actually listens.

If your situation is complicated — if you’re in a wildfire-exposed area, if you run an outdoor recreation business, if you’re in an industry that’s tough to write — that’s exactly the kind of situation where working with an independent agent pays off. We can get to carriers and products that a standard online quote won’t surface.

Reach out to Uncle Sheldon and let’s take a look at what you actually need. Colorado’s a great state to run a business. Let’s make sure you’re covered to do it.