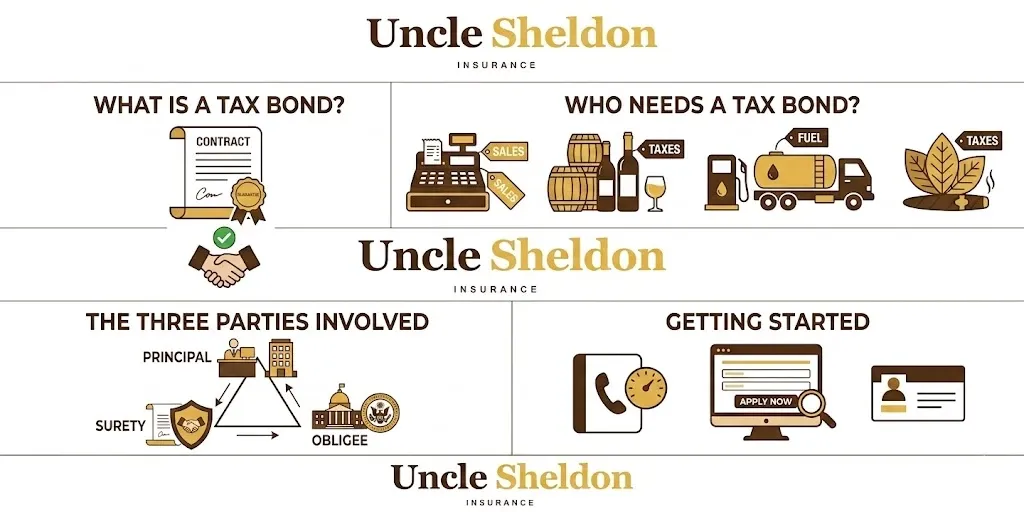

What a Tax Bond Actually Is

Not everyone has heard of tax bonds before they’re required to get one. If you’ve received a notice from a state tax authority, a department of revenue, or a federal agency telling you that you need to post a surety bond as a condition of your license or permit, a tax bond is what they’re asking for.

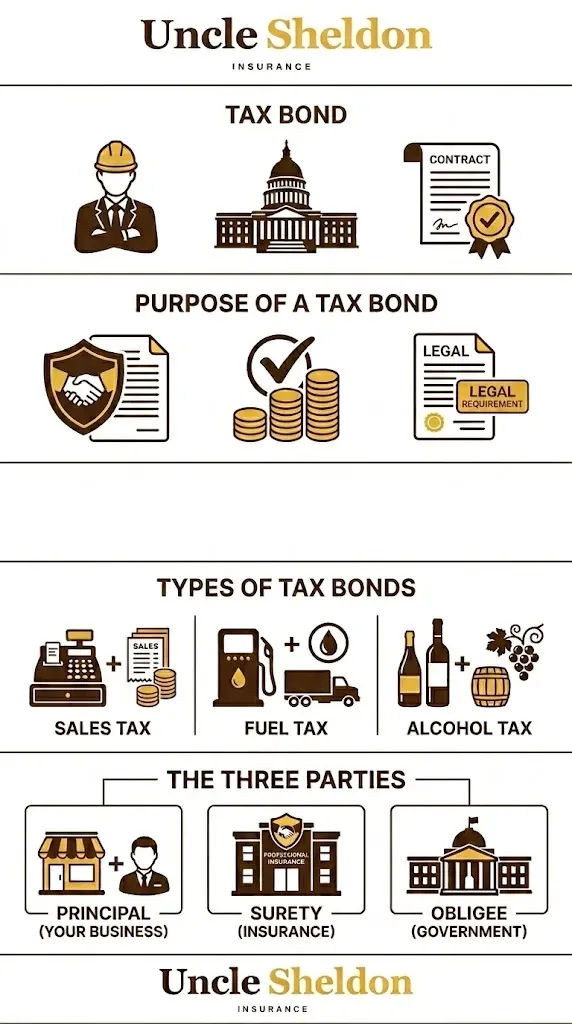

A tax bond is a type of surety bond that guarantees a business will properly collect and remit taxes to the appropriate government agency. The bond provides the taxing authority with financial protection if the business fails to fulfill its tax obligations — meaning if you collect tax money from customers and then don’t send it to the government, the government can make a claim on the bond to recover what’s owed.

The business purchasing the bond is the principal. The government agency requiring the bond is the obligee. The surety company is the bonding company that issues the bond and backs the guarantee. If the business doesn’t pay, the surety steps in — but like all surety bonds, the business is still ultimately responsible for reimbursing the surety for any claims paid.

Uncle Sheldon helps businesses across all kinds of industries get the tax bonds they need with a real agent walking them through the process — no mystery, no confusion about what you’re buying.

Why Tax Bonds Exist

Taxing authorities require tax bonds in situations where there’s a meaningful risk that a business might collect tax from customers or transactions and then fail to remit it to the government. This is more of a real risk than it might sound.

In industries where businesses are essentially acting as tax collectors on behalf of the government — collecting fuel excise taxes, collecting sales tax on transactions, collecting alcohol or tobacco taxes, collecting motor carrier taxes — the aggregate amount of tax flowing through private businesses is enormous. When a business in these categories fails financially, goes out of business, or simply stops paying, the government is the one holding the bag.

Tax bonds are the government’s way of ensuring there’s a financial backstop before the license is issued, not after a problem develops.

The bond doesn’t replace the tax obligation. It guarantees it. The business is still responsible for paying every dollar of tax it owes. The bond just gives the taxing authority an avenue for recovery if that doesn’t happen.

The Most Common Types of Tax Bonds

Tax bonds come up in a range of industries and for a range of tax obligations. Here are the most common categories.

Fuel Tax Bonds

Fuel excise taxes are among the most significant tax bond requirements. In most states, businesses that are licensed as fuel distributors, wholesale fuel dealers, or retailers selling motor fuel are required to post a bond guaranteeing their state and federal fuel tax obligations.

Fuel tax bonds are required because the tax on motor fuel — gasoline, diesel, aviation fuel — is collected throughout the distribution chain. Distributors who buy fuel and sell it to retailers are typically the party responsible for collecting and remitting the state motor fuel tax. If a distributor defaults on that obligation, the state needs to recover the funds. The bond is the mechanism for doing that.

The required bond amount for fuel tax bonds is typically based on a multiple of the average monthly tax liability — often two or three months’ worth. For high-volume fuel distributors, this can be a substantial bond amount.

Motor Vehicle Dealer Bonds

Auto dealers in most states are required to be licensed, and the licensing requirements typically include a surety bond. While these are often referred to as dealer bonds or DMV bonds, some states specifically frame them as tax-related bonds because they guarantee compliance with sales tax and motor vehicle excise tax obligations on vehicle transactions.

Used car dealers, new car dealers, motorcycle dealers, and RV dealers typically all fall under licensing and bonding requirements that include a tax compliance component.

Sales Tax Bonds

Some states require certain businesses to post a sales tax bond as a condition of obtaining a sales tax permit, particularly if the state has concerns about the business’s financial stability or compliance history. These bonds guarantee that the business will properly collect and remit sales tax on taxable transactions.

Sales tax bonds are more commonly required for businesses with a history of sales tax compliance issues, businesses in certain higher-risk industries, or in states that use bonding as a standard part of their permit application process for certain business categories.

Alcohol and Liquor Tax Bonds

Alcohol is heavily taxed at both the federal and state level, and the alcohol industry operates under licensing and bonding requirements that reflect this. Federal basic permit bonds may be required for producers, importers, and wholesalers. State bonds are required for various license types in the alcohol distribution chain — brewery licenses, distillery licenses, wine shipper licenses, wholesale distributor licenses.

The alcohol tax bond guarantees that the licensee will pay the applicable federal excise taxes and state taxes on the alcohol products they produce or distribute.

Tobacco Tax Bonds

Tobacco products carry significant federal and state excise taxes, and the distribution chain for tobacco — distributors, wholesalers, retailers — is subject to bonding requirements in many states. These bonds guarantee that cigarette tax stamps are properly purchased and that applicable taxes on tobacco products are paid.

International Fuel Tax Agreement (IFTA) Bonds

Motor carriers operating commercial vehicles in multiple states are generally required to participate in the International Fuel Tax Agreement, which provides a consolidated reporting and payment system for fuel taxes owed across jurisdictions. Some states require IFTA bonds as part of the licensing process for motor carriers, guaranteeing the carrier’s fuel tax obligations across the jurisdictions where they operate.

Cannabis Tax Bonds

As more states have legalized cannabis, they’ve built out licensing and tax compliance frameworks for the cannabis industry. Tax bonds are increasingly required for cannabis businesses — cultivators, processors, and retailers — as part of their state licensing requirements. Given the volume of cannabis-related tax revenue states are collecting, these bond requirements are taken seriously.

Federal Tax Payment Bonds

In specific circumstances — particularly in certain types of federal contracting or for certain IRS compliance programs — federal tax bonds may be required. These are less common than state tax bonds but do exist in specific contexts.

How the Bond Amount Is Determined

The required bond amount for a tax bond is set by the taxing authority requiring the bond, not by the business or the surety company. The amount is typically based on the estimated tax liability the bond is meant to guarantee.

Common approaches to setting the bond amount include a fixed amount set by statute or regulation, a multiple of the average monthly tax liability (often two to three months), a percentage of the annual tax obligation, or a tiered amount based on the volume of business done. For a new business applying for a license for the first time, the required amount may be based on projected volume or on a standard minimum set by the state.

If a business’s volume grows significantly, the taxing authority may require an increase in the bond amount to keep pace with the increased tax obligation being guaranteed.

It’s important to understand that the bond amount is not the premium you pay for the bond. The bond amount is the face value of the guarantee — the maximum the surety will pay out to the obligee if a valid claim is made. The premium is a fraction of the bond amount, typically a percentage.

What the Bond Costs

Tax bond premiums depend on the bond amount required and the creditworthiness of the applicant. Like other surety bonds, the premium is calculated as a percentage of the bond amount. For applicants with good credit, rates are often in the range of 1% to 3% of the bond amount annually.

For a $50,000 tax bond at a 2% rate, the annual premium would be $1,000. For a $100,000 bond at 2%, it’s $2,000 per year. Larger bond amounts, lower credit scores, or high-risk industries may see rates higher than this.

Unlike insurance, tax bonds don’t provide open-ended coverage — the surety will investigate any claim and, if valid, pay the obligee and then seek reimbursement from the principal. The applicant’s personal credit and financial situation are meaningful factors in surety underwriting because the surety is essentially co-signing for the applicant’s financial obligations.

Business owners with poor credit can still often get bonded, though the rate will be higher. Some sureties specialize in serving applicants with credit challenges in the bonding market.

Renewing and Maintaining Your Tax Bond

Tax bonds are typically annual — they need to be renewed each year to keep your license in good standing. When the bond is up for renewal, you’ll pay the next year’s premium to keep the bond active.

Letting a tax bond lapse can create serious problems. Most taxing authorities require continuous bond coverage as a condition of your license, meaning if the bond lapses, your license could be suspended until the bond is reinstated. For businesses that depend on their license to operate — a fuel distributor, an alcohol wholesaler, a car dealer — a lapsed bond creates an immediate operational problem.

Keep track of your bond’s expiration date and renew it before it lapses. Your surety company or your agent should send renewal notices, but it’s worth having your own calendar reminder so you’re not dependent on a renewal notice that might get lost in the mail or the inbox.

If your business situation changes — higher volume, changes in ownership, changes in the business structure — notify your agent and review whether your bond amount and terms still reflect your current situation.

What Happens When a Claim Is Made

If a business fails to remit taxes it was obligated to pay, the taxing authority can file a claim against the tax bond. The surety will investigate the claim, and if it’s valid, they’ll pay the obligee (the taxing authority) up to the bond amount.

Here’s the critical thing to understand: the surety paying the claim does not end the business’s obligation. The business still owes those taxes to the government. The surety also has the right to recover what it paid from the principal. In practice, a tax bond claim is typically associated with a business in serious financial distress or one that has simply stopped operating. The claim process ends with the surety seeking repayment from the principal.

From a practical standpoint, having a tax bond is not a way to avoid your tax obligations. It’s a guarantee that if you fail to meet those obligations, there’s a financial backstop for the government agency. And it creates a direct financial consequence for the principal if a claim is paid.

Working With Uncle Sheldon on Tax Bonds

Surety bonds are our thing. Whether you need an ERISA bond, a contractor license bond, a bid bond, or a tax bond for your fuel distributor license or your alcohol distribution license, Uncle Sheldon is your local independent agency that can help you find the right bond with real personalized service.

We work with businesses that are getting licensed for the first time and need to figure out what’s required, businesses that have outgrown their current bond amount, and businesses that are looking for better rates at renewal. We’ll take the time to understand what you need and help you get it done.

From surety bonds to insurance, Uncle Sheldon has you covered. We’re real agents helping real businesses, and we treat our clients like family. If you’re not sure what bond you need or what amount is required for your specific license, give us a call. We’re here to help.