What You Actually Need to Know About Janitorial Bonds

When you run a cleaning business, your clients are basically handing you the keys to thier most valuable spaces. Whether that’s someone’s home, a retail shop, or a big commercial office building — they’re trusting you and your crew with access to everything they own. Thats a huge responsibility. And yeah, you might trust your team completly after working alongside them for years, but your clients? They don’t know your people like you do.

That’s where a janitorial bond comes in. Its one of the smartest tools you have to prove you’re trustworthy, protect your business if things go sideways, and honestly — help you win more clients in a competitive market. But what exactly is it, and how does it actually work in the real world?

Let’s break it all down without the confusing insurance jargon.

What Is a Janitorial Bond, Exactly?

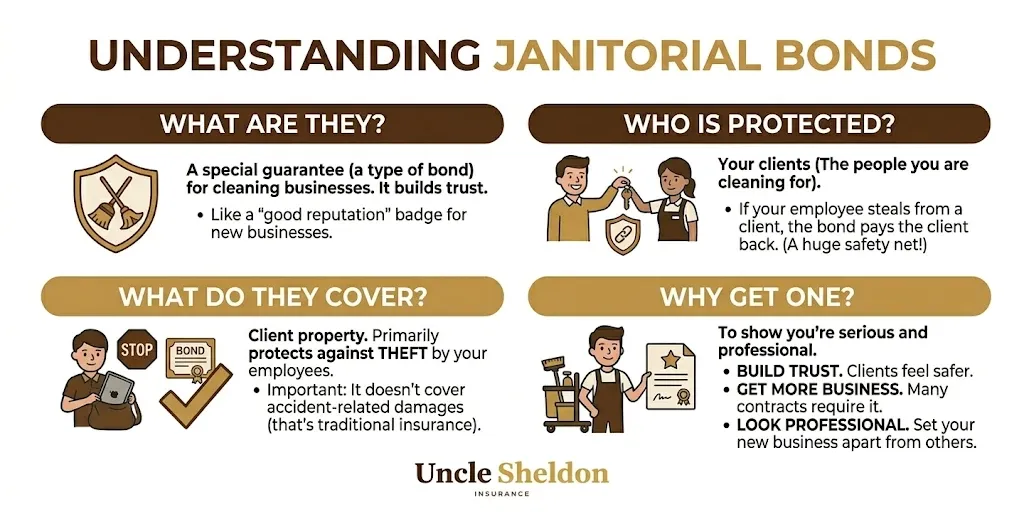

A janitorial bond — sometimes called a cleaning service bond, a custodian bond, or an employee dishonesty bond — is a specific type of surety bond built for businesses that do cleaning work.

In the simplest terms: its a financial guarantee that protects your clients if one of your employees decides to steal from them.

Say one of your crew is cleaning a residential home and pockets an expensive watch or some cash. If the homeowner finds out and files a claim, the bond is there to reimburse them for the loss.

One thing thats really important to understand: a bond is not the same thing as regular insurance. When you buy general liability insurance, it protects your business from financial damage if someone sues you for an accident or if you break something while working. A bond, though, is bought by you but it actually protects your clients. It acts as a safety net for the people who hire you — giving them a gaurantee that they wont be left empty-handed if one of your employees acts dishonestly.

How Do Janitorial Bonds Actually Work?

To understand how this works, it helps to look at the three different parties involved. Sounds technical at first, but its actually a pretty straightforward relationship.

The Principal: That’s you — the cleaning business owner. You purchase the bond, pay the premium, and agree to run your business honestly and legally.

The Obligee: This is your client. They’re the ones the bond protects.

The Surety: The company that issues the bond. If a valid claim gets filed and proven, the surety steps in and pays the client for their loss.

Here’s how a real-world scenario might look:

Your team is hired to clean a law office over the weekend. Monday morning the office manager notices a laptop is gone from a desk. Security footage shows one of your newer hires took it.

The law office (the obligee) files a claim against your janitorial bond. The surety investigates. Once the theft is proven — which usually requires a police report and sometimes a conviction, depending on the bond terms — the surety pays for the stolen laptop.

Now here’s the part that trips a lot of people up. Because a bond is more like a line of credit than a traditional insurance policy, the surety company will then come back to you (the principal) to get reimbursed for what they paid out.

Wait — if I have to pay it back anyway, whats the point of having a bond?

Great question, and we hear it all the time. The real value of a bond isn’t just the financial payout. Its the fact that a third-party financial company has vetted you and is willing to put their own money on the line to vouch for your business. That matters to clients. Without the bond, a client would have to sue you directly, which could drag things out for months or even years. The bond handles the immediate crisis, makes the client whole, and lets your business keep moving while you sort things out with the surety.

The Big Difference Between Bonding and Insurance

We talk about this a lot because its one of the most common points of confusion in the cleaning industry. You see “Licensed, Bonded, and Insured” on vans all the time, like its all one package. They often go hand-in-hand, but they do very different things.

General Liability Insurance: This covers bodily injury and property damage that happens as a result of accidents or negligence. Employee leaves a mop bucket in the hallway and a client trips? Liability. You accidentally knock over an antique vase while dusting? Liability. It protects your business from lawsuits related to accidents and mistakes.

Janitorial Bond: This strictly covers intentional theft. If your employee steals that antique vase, the bond covers it. If they accidentally break it with a vacuum cleaner, thats a job for your liability insurance.

You really need both to be fully protected. Think of liability insurance as your protection against honest accidents, and the bond as your protection against employees doing something they know they shouldn’t. Just having one leaves a pretty big gap in your coverage.

Who Actually Needs This Type of Coverage?

If your business sends employees into other peoples’ homes or businesses when the owners aren’t around to watch, you should seriously consider getting bonded. This applies to a wide range of cleaning businesses, including:

- Residential maid services and housekeepers

- Commercial janitorial companies cleaning office buildings

- Carpet and upholstery cleaning businesses

- Window washing services

- Move-in and move-out cleaning crews

- Post-construction clean-up teams

- Sanitation services for medical or industrial facilities

Even if you’re a solo cleaner with no employees at all, a bond can still be really worthwhile. It might seem strange — after all, you know you’re not gonna steal from your clients. But many commercial clients, property management firms, and HOAs just won’t hire a cleaning service thats not bonded, period. Its a box on their vendor checklist, and if you can’t check it, they move on. In that situation the bond is more of a marketing key than anything else — it still opens doors you otherwise wouldn’t be able to get through.

Why Getting Bonded Is a Smart Business Move

Getting a bond isn’t just about covering your bases and hoping nothing bad happens. Its an active tool that can help your business grow and stand out from the competition. Here’s why we think its one of the best investments you can make.

It Builds Trust Right Away

Trust is everything in the cleaning industry. You’re asking people to give you alarm codes, keys, and access to their most personal spaces. Advertising that you’re “fully bonded and insured” puts prospective clients at ease immediately. It tells them you take your business seriously and there’s a formal, professional system in place if something goes wrong. It separates you from the fly-by-night operations working out of the trunk of their car who might just disappear if a problem ever comes up.

You’ll Win More Commercial Contracts

If you want to scale up from a few residential homes to serious commercial contracts — offices, banks, retail spaces, medical facilties — a bond is almost always a strict requirement. Corporate risk managers won’t sign a contract with an unbonded cleaning company, no matter how good your referances are. Having your bond already in place means you can bid on bigger, better-paying jobs without any hesitation or delay.

Not Scrambling When Something Goes Wrong

You do background checks, you interview carefully, you check referances, you train your people well. But humans are unpredictable, and sometimes things still go wrong. If an employee does steal from a client, the bond means you’re not scrambling to find thousands of dollars to cover the loss out of your own pocket right in that moment. The bond handles the immediate crisis so you can deal with the situation more calmly and professionally.

What Does a Janitorial Bond Cover?

The primary purpose of a janitorial bond is employee dishonesty. Specifically, it covers instances where an employee steals:

- Cash, currency, or negotiable instruments

- Jewelry, watches, and precious metals

- Electronics like laptops, tablets, or phones

- Equipment, tools, or valuable supplies

- Personal belongings of the client or their employees

Its worth noting the burden of proof here. A client can’t just casually say “I think your cleaner took my $50 bill” and have the bond automatically pay out. Typically the surety requires a police report. Depending on the specific wording of the bond contract, sometimes a formal conviction of the employee is required before the surety releases any funds. This protects everyone — including you — from fraudulent or baseless claims.

What is NOT Covered by a Bond?

Just as important as knowing what’s covered is knowing what isn’t. A janitorial bond is not a catch-all safety net. It won’t help you in these situations:

- Accidental property damage: Dropping a heavy vacuum down a flight of hardwood stairs or using the wrong chemical on a marble countertop — that’s a matter for your general liability policy.

- Poor workmanship: If a client refuses to pay because they think you did a bad job cleaning the floors, the bond isn’t going to help with that.

- Injuries on the job: Employee hurts their back? Workers’ comp. Client trips over your extension cord? General liability.

- Wage and labor disputes: If an employee claims you didn’t pay their overtime or sues for wrongful termination, the bond provides zero help there. You’d need employment practices liability insurance for that kind of situation.

- Owner theft: The bond protects clients from your employees. It generally does not cover theft committed by the business owner or a partner.

How Much Does a Janitorial Bond Cost?

Honestly — less than most people expect. The annual premium is usually a pretty small percentage of the total bond amount, and the coverage it buys you is well worth it.

A few things that affect the price:

The Coverage Amount: Common bond amounts for small residential cleaning businesses range from $5,000 to $25,000. Larger commercial operations handling sensitive environments might need $50,000, $100,000, or more. Higher coverage = higher premium.

Number of Employees: More employees means statistically higher risk, so the premium goes up accordingly.

Your Business History: A few years in business with no prior claims may qualify you for a better rate than a brand-new startup.

Coverage Features: Some bonds don’t require a criminal conviction to pay out — which is more convienent for clients but might cost a little more.

Generally speaking, a $10,000 janitorial bond for a small cleaning service with under 5 employees might run anywhere from $100 to $300 per year. Thats an incredibly small price to pay for being able to advertise yourself as “fully bonded” on every piece of marketing material you put out.

How Do You Actually Get Bonded?

The process is usually fast and pretty painless. Here’s what to expect:

- Figure out how much coverage you need. Think about the types of clients you serve and what they actually have on site. Cleaning small apartments — $5,000 or $10,000 might be fine. High-end estates or tech offices with expensive equipment — you’ll want a higher limit.

- Gather your basic business info. Legal business name, address, years in operation, the type of cleaning you do, and the total number of employees on your roster.

- Apply through an agent. We work with multiple surety companies and can shop around to find the best rate and coverage terms for your specific situation. We can often package it with your general liability policy too.

- Pay the premium. Once approved — which often happens the same day — you pay your annual premium. Most standard janitorial bonds don’t even require a credit check, which is nice.

- Get your certificate. The surety issues your official bond certificate. This is the document you show prospective clients, post on your website, or include in bid packages to prove you’re fully bonded and ready to work.

The whole thing can often be done in a matter of hours, so you can start using that bonded status in your marketing almost right away.

Common Myths We Hear All the Time

Because the bonding world can be confusing and full of jargon, there’s a lot of misconceptions floating around out there. Let’s clear up a few of the most common ones.

”I Only Hire Family Members, So I Don’t Need a Bond”

This is a big trap. Even if you only employ siblings, cousins, or your own kids, your clients don’t know them. A prospective client isn’t going to just take your word that your family is inherently trustworthy. Having a bond proves that an objective third party is willing to back your business financially. Its about client percieved confidence — not just your personal trust in your own people.

”My General Liability Covers Everything Bad That Happens”

We can’t hammer this point enough because it causes real financial pain. General liability absolutely does not cover employee theft. If you only have liability insurance and an employee steals a client’s laptop, the liability carrier will deny the claim, and you’ll be personally on the hook to pay for that laptop.

”Bonds Are Way Too Expensive for a Small Startup”

A basic janitorial bond often costs less than $200 for the entire year. When you consider that having a bond might be the deciding factor in winning a $5,000-a-month commercial cleaning contract, the return on investment is massive. Think of it like a marketing expense that also happens to provide real catastrophic protection.

”If I Have a Bond, I Don’t Need Background Checks”

The bond is a safety net — not a replacement for good hiring. You should still be running thorough background checks and calling references. If you have multiple theft claims filed against your bond, the surety company will likely cancel your coverage, and you’ll have a very hard time getting bonded by anyone else after that.

What to Do If You Suspect Employee Theft

This is the nightmare call for any cleaning business owner — a furious client saying something valuable is missing after your crew was there. Handling this right is critical to protecting your reputation and making sure the bond process goes smoothly.

First, stay completely calm and listen. Don’t get defensive or immediately accuse the client of lying. But also don’t admit fault, apologize profusely for the theft, or promise to pay for the item out of pocket right then and there.

Ask for detailed, specific information: What’s missing? When was it last seen? Where was it? Who else had access to the building?

Next, conduct your own internal investigation. Talk to the employees who were on that specific job privately. Ask them directly if they saw the item or moved it. Sometimes things just get accidentally moved during cleaning and turn up somewhere unexpected.

If the item genuinely can’t be located and the client believes it was stolen, advise them they need to file an official police report. This is almost always required by the surety before they’ll even open a claim file. It also sometimes deters clients who might be making a fraudulent claim.

Once the police report is filed, contact your agent or the surety company directly to report the potential claim. They’ll walk you through next steps.

Its stressful — no question about it. But having the bond means you have a formal, structured process to rely on instead of just panicking and trying to find the cash to make the problem disappear on your own.

How to Prevent Theft in the First Place

The best claim is the one that never happens. Here’s how to keep your record clean.

Run Comprehensive Background Checks: Every single employee before they ever set foot on a client’s property. And actually call their references — don’t just collect them.

Create a Culture of Accountability: Make it crystal clear from day one that your company has a zero-tolerance policy for theft. Tell your employees what the bond is and explain that if they steal, its not just the company looking into it — its an insurance company and the police.

Use a Team Approach: Whenever possible, avoid sending employees to clean large locations alone. Two-person teams create a natural system of checks and balances. People are less likely to do something dishonest when a coworker is right there in the next room.

Be Meticulous About Keys and Alarm Codes: Keep them locked up at your office, only distribute them for the specific job, and never put the client’s name or address on the key tag itself.

Show Up Unannounced Sometimes: Knowing the boss might walk in at any moment is a strong deterrent to bad behavior.

Frequently Asked Questions About Janitorial Bonds

Can I get bonded if I have a criminal record?

It depends. Surety companies do run background checks on the business owner. Minor old stuff might not be a deal-breaker, but a recent conviction for theft or fraud will likely disqualify you from getting a standard janitorial bond.

Do I need a separate bond for every client?

Nope. One janitorial bond covers your business as a whole up to the coverage limit, regardless of how many clients you service.

What happens if a claim exceeds my bond limit?

If your bond is $10,000 and an employee steals $15,000 worth of jewelry, the surety pays out the maximum of $10,000. The client could then potentially sue your business for the remaining $5,000. This is why choosing the right coverage amount from the start matters.

Are sub-contractors covered under my bond?

Generally no. Janitorial bonds usually only cover your W-2 employees. Independent contractors should really carry thier own separate bonds and insurance.

Is a janitorial bond tax deductible?

Yes, in almost all cases. The premium is considered a standard business expense, just like your liability insurance premiums or cleaning supplies.

Maintaining Your Bond and Building a Strong Reputation

Getting bonded is really just the first step. To truly benefit from it, make it a core part of your brand identity and your daily operations.

Put “Fully Bonded and Insured” prominently on your website, your business cards, your company vehicles, and any flyers or brochures you hand out in the community. When you meet with a potential client for an estimate or walkthrough, physically hand them a copy of your bond certificate along with your liability certificate in a professional folder. That level of preparedness and transparency is incredibly reassuring to clients and sets you apart from competitors who show up empty-handed.

Also use it in your hiring process. Let potential hires know during the interview that your company is bonded — which means a clean background check is required — and that you take client security seriously. This can help weed out bad actors before they ever fill out an application.

A janitorial bond is way more than just a piece of paper. Its a visible commitment to running a legitimate, professional operation that puts clients first.

If you’ve been putting this off because it seemed too complicated, too expensive, or just unnecesary for your size of business — hopefully this guide made it clear that it’s actually pretty accessible and genuinely vital for any cleaning company looking to grow. Our team is knowledgeable in these specific types of bonds and we’re here to help make the process quick and painless. We want you to succeed, and getting the right foundational protection in place is the best way to start. Reach out and lets talk.