When Personal Auto Isn’t Enough

A lot of business owners don’t realize there’s a problem with their auto coverage until something happens. They’ve been driving their truck to job sites, making deliveries in their van, or hauling equipment around town for years—and they’ve got a personal auto policy that seems to cover everything just fine. Until it doesn’t.

Personal auto insurance is written for personal use. When you’re using a vehicle for business purposes—hauling tools to a job, delivering products, transporting clients, making service calls—your personal policy may exclude coverage for accidents that happen in the course of business activities. The insurer can and often does deny a claim when they determine the vehicle was being used for commercial purposes at the time of the accident.

That’s a situation nobody wants to be in. Commercial auto insurance exists specifically to close that gap. It covers vehicles that are owned, leased, or regularly used by a business, and it’s built around the kinds of use and liability exposure that come with operating vehicles commercially.

Who Actually Needs Commercial Auto Coverage

The list is broader than most people assume. You don’t need to be running a fleet of delivery trucks to need commercial auto insurance. If any of the following applies to you, it’s worth having a conversation about whether you have the right coverage:

- You use your personal vehicle regularly to visit clients, job sites, or customers

- You transport tools, equipment, or materials for your business

- Your business owns, leases, or finances any vehicle

- Employees drive on behalf of your business, including using their own personal vehicles

- You use a van, truck, or other vehicle to make deliveries

- Your vehicle is lettered or wrapped with business branding

- You haul a trailer with business equipment or supplies

- You transport passengers for a fee

That last category—employees using their own cars for business—is one that a lot of small business owners overlook entirely. If an employee drives their own vehicle to pick up supplies, make a deposit, or run any kind of errand for the company and gets into an accident, that creates potential liability for the business. We’ll come back to how that gets handled in a minute.

Vehicles That Typically Fall Under Commercial Coverage

| Vehicle Type | Common Example | Likely Coverage Needed |

|---|---|---|

| Business-owned passenger vehicles | Company car, owner’s truck used for work | Commercial auto policy |

| Vans and cargo vehicles | Plumbing vans, delivery vehicles | Commercial auto policy |

| Pickup trucks used commercially | Contractor’s truck with tools and equipment | Commercial auto policy |

| Light-duty service vehicles | Landscaping, HVAC, pest control trucks | Commercial auto policy |

| Heavier trucks (over 10,000 lbs GVW) | Box trucks, medium-duty work trucks | Commercial auto; may involve DOT regulations |

| Large commercial trucks/semis | Tractor-trailers | Trucking insurance program |

| Trailers | Utility trailers, equipment trailers | Physical damage; may need separate coverage |

For heavy commercial trucking—semis, tractor-trailers, and the like—the coverage gets more specialized and falls under what’s typically called trucking insurance, which is a whole category of its own with FMCSA requirements and federal filings involved. Commercial auto for most small businesses is different from that.

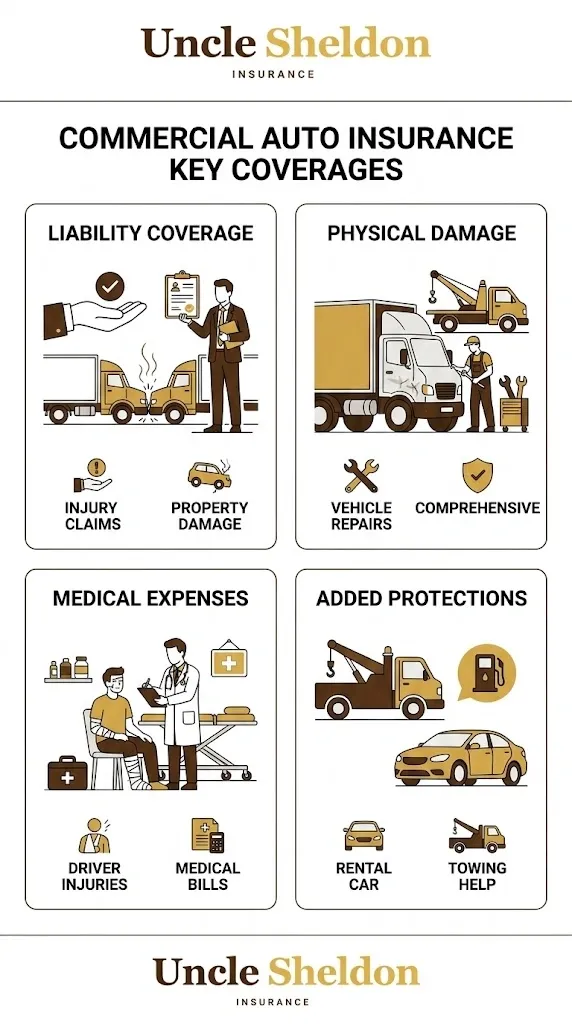

The Coverage Types Inside a Commercial Auto Policy

Commercial auto policies have a similar structure to personal auto, but the limits and some of the specifics are built for business use.

Commercial Auto Liability

This is the core of any commercial auto policy. Liability coverage pays for bodily injury and property damage you cause to other people when you or your employees are driving a covered vehicle. If one of your service vans runs a red light and hits another car, liability coverage pays for the other driver’s medical bills, vehicle repairs, legal defense if you get sued, and any damages awarded.

State minimums for commercial auto liability exist, but they’re often not enough for a business. A serious accident involving a commercial vehicle can easily result in claims far exceeding personal auto minimums. Businesses typically carry higher liability limits than individuals because the exposure is higher and the consequences of being underinsured are more serious.

Physical Damage — Collision and Comprehensive

Collision coverage pays for damage to your own vehicle when it’s involved in a collision, regardless of fault. Comprehensive covers non-collision damage—theft, fire, vandalism, hail, hitting a deer, and so on.

If you have a loan or lease on a business vehicle, the lender will require you to carry physical damage coverage. If you own the vehicle outright, it’s your call, but for any vehicle with significant value, going without physical damage is taking on a risk that most businesses shouldn’t absorb.

Physical damage is rated based on the stated value of the vehicle, so keeping your vehicle values up to date on the policy matters. If you’ve added significant equipment or upfitting to a truck—toolboxes, a lift, specialized body work—that increases the actual value of the vehicle and should be reflected in your coverage.

Uninsured and Underinsured Motorist

Covers you and your employees if you’re hit by a driver who either has no insurance or doesn’t have enough insurance to cover the damages they caused. This is surprisingly important. A significant percentage of drivers on the road are uninsured or carrying state minimum limits that wouldn’t come close to covering a serious injury.

Medical Payments / Personal Injury Protection

Covers medical expenses for you and your passengers after an accident, regardless of who was at fault. The availability and specifics of this coverage vary by state.

Hired and Non-Owned Auto — The Coverage Most Businesses Miss

This is one of the most commonly misunderstood and most commonly missing pieces of commercial auto coverage for small businesses.

Hired auto coverage applies when your business rents or borrows vehicles. If you rent a car while traveling for business or rent a van for a big delivery, hired auto coverage extends your commercial auto liability to that vehicle.

Non-owned auto coverage is the one that protects your business when employees use their own personal vehicles for company business. If an employee drives their personal car to the bank to make a deposit for your company and causes an accident, the employee’s personal auto policy is going to be the primary coverage. But depending on how the claim goes, your business could be brought into the lawsuit as well. Non-owned auto liability coverage is there to protect the business in those situations.

A lot of small businesses—especially service businesses where employees run errands or make deliveries in their own cars—should have non-owned auto coverage and either don’t know it exists or don’t realize they’re exposed without it. It’s not expensive to add to a commercial auto policy and it closes a gap that can otherwise be a real problem.

Fleets vs. Single Vehicles

If your business has multiple vehicles, how they’re covered—individually or together on a fleet policy—makes a difference.

A fleet policy covers multiple vehicles under a single policy, which simplifies things considerably. One renewal date, one carrier, one set of terms. Fleet pricing can also be more favorable than insuring vehicles separately, depending on the size of the fleet and your loss history.

There’s no universal definition of what constitutes a “fleet” for insurance purposes—some carriers start fleet programs at five vehicles, others at three, and some will write multi-vehicle policies for just two. If you have more than one business vehicle, it’s worth asking whether a fleet approach makes more sense than separate policies.

As your fleet grows and the total exposure increases, carriers look more closely at driver history, vehicle maintenance practices, and loss history. A business with a clean record of no claims and well-maintained vehicles is going to get better treatment than one with a pattern of accidents. Safety programs, written driver policies, and MVR checks on drivers can all work in your favor.

What Affects the Price

Commercial auto premiums vary quite a bit from business to business. Here’s what underwriters look at:

Driver history — The driving records of everyone who’ll be operating your vehicles. At-fault accidents, moving violations, DUIs—these follow drivers and significantly affect premiums. Newer drivers and those with violations cost more to insure.

Type of vehicle — A cargo van has a different risk profile than a pickup truck or a passenger car. Heavier vehicles cause more damage in accidents. Higher-value vehicles cost more to repair or replace.

How the vehicle is used — Radius of operation matters. A vehicle making local deliveries in a 25-mile radius is rated differently than one traveling regionally or nationally. The nature of the work matters too—a catering company’s van and a contractor’s truck are used differently.

What’s being hauled — If you’re carrying tools, equipment, or products in the vehicle, the value and nature of that cargo can affect how the risk is rated, especially if you also want cargo coverage.

Prior claims history — A clean loss history helps. Prior claims, especially at-fault accidents, push premiums up.

Industry — Some industries are higher risk by nature. A construction company’s vehicles get into more scrapes than a consulting firm’s company car.

Number of vehicles — More vehicles means more exposure. Fleet discounts can offset some of this for larger operations.

Contractors and Trades — A Specific Note

Contractors—electricians, plumbers, HVAC technicians, roofers, general contractors—are one of the biggest groups that need commercial auto coverage and sometimes don’t have it structured correctly. A pickup truck that’s your primary work vehicle, loaded with tools and equipment, driven to job sites daily, and lettered with your company name is not a candidate for personal auto insurance. It’s a commercial vehicle doing commercial work, and it needs to be covered accordingly.

Beyond the truck itself, a lot of contractors pull trailers—equipment trailers, landscaping trailers, utility trailers. Trailer coverage is a separate question and depends on whether the trailer is owned, borrowed, or rented, and what’s on it. Talk to your agent specifically about how trailers are handled in your situation so there aren’t any gaps.

Does Your Business Also Need General Liability?

This comes up a lot when we talk to business owners about commercial auto, so it’s worth mentioning. Commercial auto covers accidents that happen in connection with operating a vehicle. It does not cover general business liability—injuries that happen on a job site, property damage you cause while doing your work, slip-and-falls at your place of business, and so on.

A business that needs commercial auto almost always also needs a general liability policy. These are different coverages addressing different risks, and having one doesn’t substitute for the other. If you don’t have both in place, there are probably gaps in your overall coverage picture.

The State Requirement Side of Things

Every state requires minimum liability coverage for vehicles operated on public roads, and those minimums apply to commercial vehicles as much as personal ones. In some states, commercial vehicles may be subject to higher minimums depending on the vehicle type and how it’s used.

If you’re operating vehicles across state lines or your business is subject to any federal or state commercial vehicle regulations, additional requirements may apply. Businesses that cross into regulated trucking territory—based on vehicle weight, type of cargo, or operating in interstate commerce—face requirements from the Federal Motor Carrier Safety Administration on top of state requirements.

For most small businesses operating lighter commercial vehicles within a single state, state minimums and your carrier’s standard commercial auto options are the relevant framework. Your agent should know the requirements that apply to your specific vehicles and operations.

Getting Started With Uncle Sheldon

When you reach out about commercial auto coverage, it helps to have a few things ready:

- The year, make, model, and approximate value of each vehicle you need covered

- How each vehicle is used and your typical operating area

- A list of drivers who’ll be operating the vehicles and their license information

- Any prior accidents or claims from the past three to five years

- What types of work your business does and what if anything is typically carried in the vehicles

The more we understand your operation, the better we can match you to carriers that actually want to write your class of business and will treat you right when a claim comes up. We’re an independent agency, so we work across multiple insurance companies—not just one. That means we can find the right fit for your business rather than forcing your situation into whatever a single carrier offers.

We’re real people who take the time to understand what you do. Give us a call or reach out and let’s figure out the right commercial auto setup for your business.