You Can’t Skip This Part

If you’re trying to get your mortgage broker license, the bond is not optional. Most states require it before they’ll even look at your application through the NMLS. And it’s not just a formality — the bond is a real financial guarantee that you’re going to operate your business the right way. Understanding what it is, why it exists, and how the cost is determined will save you time and help you get this piece of your licensing handled the right way.

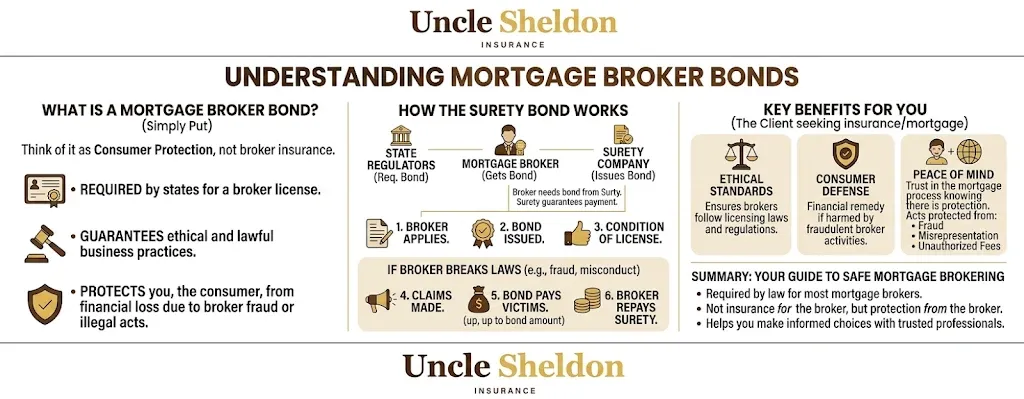

A mortgage broker bond is a type of surety bond. It’s different from insurance in a pretty fundamental way, and a lot of first-time applicants don’t realize that until they’re already in the process. Let’s start with the basics and work from there.

The Difference Between a Bond and Insurance

This trips people up all the time so it’s worth taking a real minute on it.

When you buy an insurance policy, you’re buying protection for yourself. If something goes wrong, the insurance company pays out and you’re made whole. That’s how it works for auto, home, liability — you file a claim, they pay, the loss is covered on your side of the ledger.

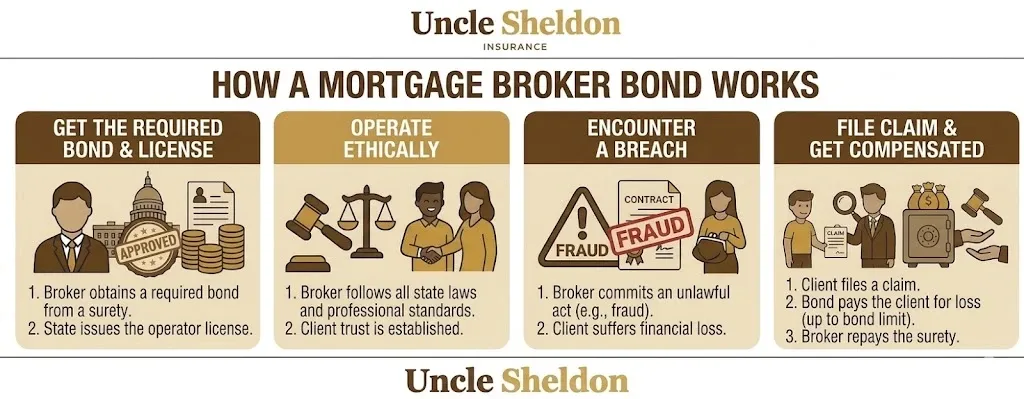

A surety bond works totally differently. It’s not there to protect you. It’s there to protect the public — in this case, your future clients and the state that issues your license. You’re basically making a promise to the state and your customers that you’ll operate legally and honestly. The bond backs up that promise with actual money.

There are three parties involved in every surety bond:

- The Principal — that’s you, the mortgage broker getting bonded

- The Obligee — the state licensing authority (or the federal level in some cases) that’s requiring the bond

- The Surety — the bonding company that issues the bond and backs it financially

If you do something wrong — mishandle client funds, violate lending regulations, commit fraud — a harmed party can file a claim against the bond. If the claim is valid, the surety company pays out up to the bond amount. Then the surety turns around and comes to you to be repaid. That last part is the big difference from insurance. With insurance, the company absorbs the loss. With a bond, you’re still ultimately on the hook. The surety is more like a line of credit guaranteeing your good behavior than a policy protecting you from loss.

Why States Require It

The mortgage industry has a rough history with bad actors. Predatory lending, fraudulent origination practices, steering borrowers into bad loan products — these things have caused real harm to real people, and the regulatory environment around mortgage origination reflects that.

State legislatures and regulators use the licensing process, including the bonding requirement, as a way to create financial accountability. If a mortgage broker operates improperly and harms a client or violates state lending laws, the bond provides a fund that harmed parties can actually recover money from. It’s a consumer protection mechanism built directly into the licensing system.

The NMLS — the Nationwide Multistate Licensing System — is the centralized platform that most states use to manage mortgage license applications. The NMLS doesn’t issue bonds, but it is where you’ll track and submit your licensing information, including your bond filing. Most states have their mortgage broker bond requirements posted within the NMLS resource center, and you’ll need to upload a copy of your bond certificate as part of the application.

Bond Amounts by State — What You’re Actually Looking At

Bond amounts are set by each state, and they vary quite a bit. Some states have a flat amount. Others base the required bond amount on your loan volume, the number of licensed locations you operate, or the number of originators you have working for you.

Here’s a rough look at some common state requirements. Note that these change — states update their requirements, so always verify the current amount with the NMLS or your state’s licensing authority before you apply.

| State | Typical Bond Amount |

|---|---|

| California | $50,000 |

| Florida | $35,000 |

| Texas | $50,000 |

| New York | $10,000 – $500,000 (volume-based) |

| Colorado | $25,000 |

| Georgia | $150,000 |

| Illinois | $25,000 |

| Virginia | $25,000 |

| Arizona | $10,000 |

| Michigan | $25,000 |

Some states have lower amounts that make the cost of the bond pretty manageable even if your credit isn’t perfect. Others, like New York, have volume-based requirements that can get significant for larger operations. If you’re licensed in multiple states, you’ll likely need a separate bond for each one — or in some cases, a single larger bond that covers your operations in all of them. That depends on the specific states involved.

How Much Does a Mortgage Broker Bond Cost

This is the first question almost everyone asks, and the answer is: it depends on your credit.

Surety bond premiums are almost entirely credit-driven. The bonding company is extending a guarantee on your behalf, and just like any other form of credit, they want to know whether you’re likely to cause a claim and whether you’d be able to repay them if one occurred. Your personal credit score is the primary factor in determining what percentage of the bond amount you’ll pay as an annual premium.

Generally speaking, here’s how the pricing tends to shake out:

| Credit Profile | Approximate Annual Premium Rate |

|---|---|

| Excellent credit (720+) | 1% – 2% of bond amount |

| Good credit (680 – 719) | 2% – 3% of bond amount |

| Fair credit (620 – 679) | 3% – 5% of bond amount |

| Poor credit (below 620) | 5% – 15% of bond amount |

So if your state requires a $50,000 bond and you have excellent credit, you might pay somewhere around $500 to $1,000 a year. If your credit is on the lower end, that same bond could run $2,500 to $7,500 annually. It’s the same bond amount, same coverage — the rate just reflects how the surety company views the risk of backing you.

A few other things that can affect pricing beyond credit:

- Prior claims on a surety bond

- Financial background and any history of bankruptcy

- Industry experience and how long you’ve been in the mortgage business

- The specific bonding company — rates genuinely vary between sureties, and shopping matters

For applicants with challenged credit, some sureties specialize in higher-risk bonds and can still get you covered, though the premium will reflect that risk. Don’t assume you can’t get bonded because your credit has some issues — the market for these bonds is broader than people expect.

The NMLS and Your Bond Filing

Getting bonded isn’t just about paying the premium. You also have to file the bond correctly with the NMLS and with your state’s licensing authority. Here’s generaly how that works:

- You apply for the bond through a surety or through an agent like Uncle Sheldon who works with sureties.

- The surety reviews your application and issues the bond.

- You receive a bond certificate — a document showing the bond amount, the effective dates, the surety company, and the obligee (your state licensing authority).

- You upload the bond certificate through the NMLS as part of your license application, or you submit it directly to your state depending on their process.

- Some states also require the original bond document to be mailed in — check your state’s specific requirements because this varies.

The bond has to be kept active for as long as you hold your license. Most mortgage broker bonds renew annually. Your state may require proof of renewal, and some states have a grace period for lapsed bonds while others will suspend your license if coverage lapses even briefly. This is not the kind of thing you want to let slip through the cracks.

One thing worth knowing — when your bond renews, the surety will typically review your credit and business situation again. If your credit has improved, your renewal rate might actually come down. If things have gotten more complicated, it could go the other way. Staying on top of your credit situation has a direct financial impact on what you pay for your bond.

What Happens When a Claim Is Filed

This is the part most people don’t think about when they’re getting bonded, but it’s worth understanding because it shapes how you should think about the bond as part of running your business.

If a client or the state believes you’ve violated your licensing obligations — say you misrepresented loan terms, failed to disclose fees, mishandled escrow funds, or engaged in any kind of deceptive practice — they can file a claim against your mortgage broker bond.

The surety company investigates the claim. If they determine it’s valid, they pay out to the harmed party up to the bond amount. Then they pursue reimbursement from you. This is called the indemnity provision, and it’s in every surety agreement you sign. The surety is not absorbing the loss — they’re fronting the money, and they expect it back.

This is why bonding companies care so much about who they’re backing. A claim against your bond is a bad situation for everyone — for the harmed client, for your business, for your license, and for your relationship with the surety.

The practical message here is that a mortgage broker bond is not a “get out of jail free” card or a way to cover business mistakes. It’s a consumer protection mechanism that holds you accountable. Running a clean, compliant operation is the best way to make sure the bond never becomes a problem.

Mortgage Broker vs. Mortgage Lender Bonds

There’s sometimes confusion between the bond required for a mortgage broker license and the bond required for a mortgage lender license. They’re related but different.

A mortgage broker is someone who originates loans and connects borrowers with lenders but doesn’t actually fund the loans themselves. The bond for a broker license is typically lower than for a lender.

A mortgage lender or banker actually funds the loans, which creates a much larger financial exposure. Accordingly, lender bonds tend to have higher required amounts and can be significantly more expensive.

If you’re applying for a loan originator license under an existing company rather than opening your own brokerage, you may not need a separate bond — the company holds the license and the bond covers the operation. Individual originators are typically covered under their employer’s license rather than needing their own bond.

If you’re starting your own brokerage, you will need the bond. If you’re unsure which category applies to your situation, that’s a good thing to figure out before you start the licensing process.

Renewing and Maintaining Your Bond

Once you have your bond and your license, the bonding relationship is ongoing. Here’s what to expect on an ongoing basis:

Annual renewal — Most mortgage broker bonds renew yearly. The surety will send a renewal notice, typically 30 to 60 days before expiration. You pay the renewal premium, the surety issues a continuation certificate, and you may need to file that with your state or NMLS depending on their requirements.

License renewal and bond alignment — Your license and bond should be kept aligned. If your license renews at a specific time of year, it can be helpful to have your bond renewing around the same time so you’re not managing them on different schedules.

Bond amount changes — If your state changes the required bond amount, you’ll need to adjust your bond accordingly. This sometimes comes up when states update their licensing statutes. Same thing if your loan volume triggers a higher required amount under a volume-based requirement.

Keeping your contact info current — The surety needs to be able to reach you at renewal. Keep your contact information up to date with your bonding agent so renewal notices don’t get lost.

Working With Multiple States

If you’re licensed in more than one state — or planning to be — the bonding situation gets a little more complicated because each state has its own bond requirements and its own required obligee name on the bond.

Some states participate in a compact or have reciprocal licensing arrangements that can simplify things, but you generally still need a bond filed in each state where you hold a license. Managing bonds across multiple states means tracking multiple renewal dates, potentially multiple sureties (though some can write bonds in multiple states), and making sure each state’s requirements are met independently.

It sounds like a lot of paperwork because, honestly, it is. Having an agent who understands the licensing landscape and can help coordinate across states makes this a much less painful process.

Common Mistakes First-Time Applicants Make

Seen these enough times that it’s worth calling them out directly:

Waiting too long to get bonded. The bond is required before your license application can be approved. If you’re counting on a specific start date for your brokerage, get the bond in process early — well before you need it — because sometimes the underwriting takes a few days, and you don’t want the bond to be the thing holding you up.

Not verifying the current required amount. States do update their bond requirements. Always confirm the current amount with your state licensing authority or through the NMLS resource center before applying. Getting bonded for the wrong amount means you have to get a new bond.

Assuming the bond covers your business losses. It doesn’t. A lot of people confuse the bond with E&O insurance or general liability. The bond protects your clients and the state, not you. If you want protection for your own business operations, errors and omissions insurance is what you’re looking for.

Letting the bond lapse. A lapsed bond = a licensing problem. Stay on top of renewal dates like you would any other compliance deadline.

Not shopping rates. Bond premiums vary between sureties. Especially if your credit is less than perfect, getting quotes from multiple sources can save you real money.

Getting Bonded Without the Headache

Getting your mortgage broker bond doesn’t have to be complicated, but it does help to work with someone who actually understands what’s involved. We help mortgage professionals get bonded every day — whether you’re applying for your first license, renewing a bond you already have, or trying to get bonded across multiple states.

We’re independant, which means we work with multiple surety companies and can shop your bond to find the best rate for your credit profile. We’re not tied to one carrier, so we’re always looking for the right fit for your actual situation rather than just the easiest option for us.

And we’re real people. If you have questions about what your state requires, how the bond works, what happens at renewal, or anything else — just ask. We’ll give you a straight answer and help you get this piece handled so you can focus on building your business.

Reach out and let’s get it done.