Got a Boat? Let’s Make Sure You’re Actually Covered

A lot of boat owners assume they’re covered under their homeowners policy. And technically, some of them are — a little bit. Most standard homeowners policies offer limited coverage for smaller watercraft, usually canoes, small sailboats, or motorboats under a certain horsepower. But the moment you get into anything bigger, faster, or more expensive, that coverage becomes pretty thin pretty fast. And if you’re storing your boat off-property, trailering it around, or taking it on open water, the gap gets even wider.

Boat insurance — sometimes called watercraft insurance or marine insurance — is a standalone policy designed specifically for the risks that come with owning and operating a boat. It covers what your homeowners won’t, and it’s built around the realities of being out on the water rather than sitting in your driveway.

We love boats here. And we want to help you protect yours the right way, with a policy that actually makes sense for how you use it.

What Kinds of Boats Can Be Covered

Boat insurance is a broad category that covers a wide range of watercraft. When people hear “boat insurance” they sometimes think it’s only for big expensive sailboats or offshore fishing rigs, but that’s not how it works. Coverage is available for all kinds of vessels, including:

- Pontoon boats

- Bass boats and fishing boats

- Ski boats and wakeboard boats

- Runabouts and bowriders

- Deck boats

- Personal watercraft (jet skis, Sea-Doos, WaveRunners)

- Jon boats

- Inflatable boats and rigid inflatables (RIBs)

- Canoes and kayaks (though these often have limited options)

- Sailboats

- Houseboats

- Yachts and larger cruisers

- Center consoles and offshore fishing boats

The type of watercraft you have affects how it’s underwritten, what coverage options are available, and what it costs. A 14-foot aluminum fishing boat is a very different insurance conversation than a 35-foot inboard cruiser, but both of them can be covered.

The Main Pieces of Coverage

A boat insurance policy typically has several distinct coverage components. Understanding each one helps you build a policy that actually fits your situation.

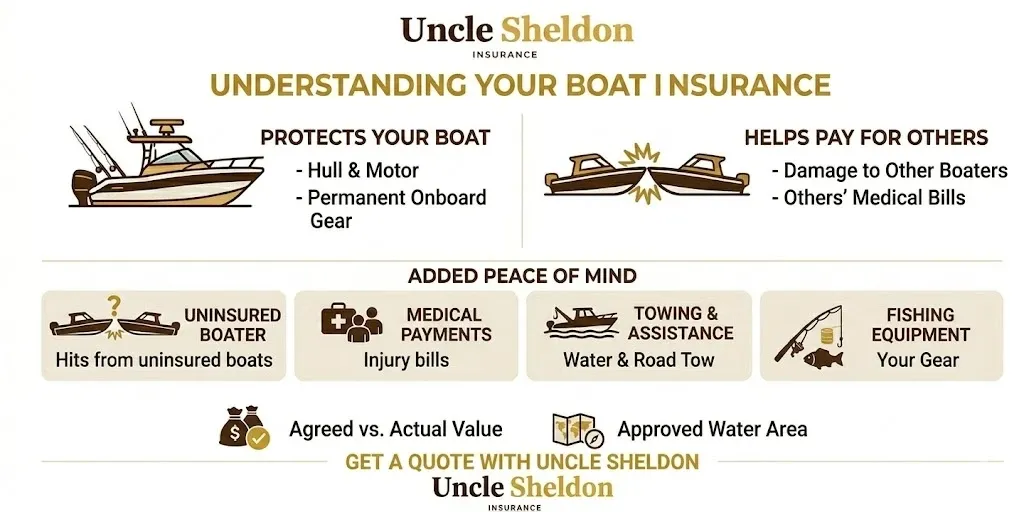

Hull Coverage (Physical Damage)

This is coverage for physical damage to the boat itself — the hull, motor, sails if it’s a sailboat, permanently attached equipment, and usually the boat’s standard gear and electronics. If your boat is damaged in a collision, storm, fire, sinking, or vandalism, hull coverage is what pays for repairs or replacement.

There are two ways hull coverage can be structured, and the difference is significant.

Agreed Value — You and the insurance company agree on the value of the boat at the time you buy the policy. If the boat is totaled, you get that agreed amount — no depreciation, no argument. This is the better option for most boat owners because you know exactly what you’re going to get if something goes wrong.

Actual Cash Value — The insurer pays what the boat is worth at the time of the loss, taking depreciation into account. An older boat might be worth significantly less than what you paid for it or what it would cost to replace it. ACV policies are typically cheaper upfront but can leave you short when it matters.

| Valuation Type | How It Works | Best For |

|---|---|---|

| Agreed Value | Pays the full agreed amount if total loss; no depreciation | Newer boats, boats holding their value, owners who want certainty |

| Actual Cash Value | Pays market value at time of loss after depreciation | Older or lower-value boats where premium savings matter more |

Liability Coverage

Liability is the part of your policy that protects you if you cause injury to someone else or damage their property while operating your boat. It covers medical expenses, property damage, legal defense, and settlements or judgments if you’re sued.

Boat accidents happen — and they can be serious and expensive. A collision with another vessel, someone getting hurt near your boat’s propeller, damaging a dock, or causing a wake that injures someone on a smaller craft — all of these are liability situations. Without coverage, you’re paying for all of it out of pocket.

Liability limits on boat policies typically start around $100,000 and can go much higher depending on what you want. For boats used frequently or in areas with heavy traffic, stronger liability limits are worth considering.

Medical Payments

This covers medical expenses for you and your passengers if there’s an accident on the water, regardless of who’s at fault. It’s a no-fault coverage — it doesn’t require a liability determination to pay out. The limits are usually modest ($1,000 to $10,000 per person is common), but it handles the smaller stuff quickly without a claim fight.

Uninsured/Underinsured Watercraft

Similar to uninsured motorist coverage in auto insurance, this protects you if you’re in an accident caused by another boater who has no insurance or not enough insurance to cover your losses. Not every boater on the water carries insurance, and if one of them hits you and causes significant damage or injury, this coverage is what makes you whole.

On-Water Towing and Assistance

This is one people don’t think about until they need it. If your boat breaks down on the water — engine trouble, dead battery, out of fuel, runs aground — on-water towing coverage gets you rescued and back to the dock. It’s the marine equivalent of roadside assistance. Some policies include it, others offer it as an add-on, and the cost is usually pretty modest.

| Coverage Type | What It Protects | Worth Having? |

|---|---|---|

| Hull / Physical Damage | Damage to the boat, motor, and equipment | Essential for any boat with significant value |

| Liability | Injury or damage you cause to others | Essential; you’re exposed without it |

| Medical Payments | Medical costs for you and passengers | Recommended; fills gaps quickly |

| Uninsured Watercraft | Accidents caused by uninsured boaters | Very useful; other boaters often carry no insurance |

| On-Water Towing | Breakdown or emergency assistance on water | Highly recommended for anything beyond calm inland lakes |

Personal Effects and Fishing Equipment

Standard hull coverage typically covers the boat and its permanently attached equipment, but not the stuff you bring on board. Your rods, reels, tackle, life jackets, coolers, water sports gear, GPS devices, and other personal property are usually not covered unless you specifically add coverage for them.

For avid anglers especially, the fishing gear you load on a boat can add up to quite a bit of money. Asking about coverage for personal effects and fishing equipment when you’re shopping for a policy is worth it.

Trailer Coverage

If your boat lives on a trailer and you tow it regularly, the trailer is worth thinking about separately. Some boat policies include the trailer, some don’t. When coverage is included, there are usually limits on how much the policy pays for the trailer specifically.

Your auto policy might cover the trailer while it’s attached to your vehicle, but once you unhook it, that coverage generally stops. If your trailer has any real value — and newer aluminum or tandem-axle trailers aren’t cheap — confirm it’s covered somewhere.

Navigating the Navigation Territory Question

One of the unique aspects of boat insurance is the concept of a navigation territory or coverage area. Your policy covers your boat while it’s within a defined geographic range — and operating outside that range can affect whether a claim is covered.

For most recreational boaters on inland lakes and rivers, this isn’t much of an issue. But if you plan to take your boat into coastal waters, run offshore, or cross into the Great Lakes or other large bodies of water, it matters a lot. Some policies restrict coverage to inland waters only. Others cover coastal areas up to a certain number of miles offshore. Offshore fishing boats and bluewater cruising sailboats need policies with broader navigation territories.

Be honest about where you take your boat. If you’re telling the insurer you stay on the lake but you regularly run out to the coast, you might have a coverage problem when you need it most.

Seasonal Lay-Up and Winterization

In colder parts of the country, boats get stored for winter and don’t go back in the water until spring. A lot of carriers offer a lay-up period discount — a reduced premium during the months when the boat is out of the water and not in use.

To get the discount, you usually have to agree not to operate the boat during the lay-up period. The coverage doesn’t disappear entirely — physical damage from fire, theft, and similar perils is still in place — but the on-water coverage is suspended. For boats that sit in storage from November through April, this can save a meaningful chunk of premium.

If you’re in a warmer climate and boat year-round, this doesn’t apply to you, but it’s worth asking about if you’re in the northern half of the country.

Is Boat Insurance Actually Required?

Unlike auto insurance, there’s no universal federal law requiring boat insurance. Requirements vary by state, and most states don’t mandatorily require it — though that doesn’t mean you can skip it without consequences.

A few situations where you effectively need it regardless of what the law says:

Marina storage — Most marinas require proof of liability insurance as a condition of a slip or storage agreement. If you keep your boat at a marina, you almost certainly need at least a liability policy.

Financed boats — If you have a loan on your boat, the lender is going to require physical damage coverage, similar to how an auto lender requires comprehensive and collision on a financed car. They want the collateral protected.

State minimums where they exist — A handful of states and specific bodies of water have minimum insurance requirements for certain types of watercraft. It’s worth checking the rules for your state specifically.

And beyond the legal and contractual requirements — if your boat is worth anything, going without insurance is just a significant financial risk. An accident, a bad storm, a fire in the marina — these things happen, and the costs can be substantial.

What Affects the Cost

Boat insurance premiums depend on a lot of factors specific to your situation. Here’s what underwriters generally look at:

Type and size of the boat — A small aluminum fishing boat and a 30-foot cabin cruiser have very different risk profiles and very different premiums. Larger, faster, and more powerful boats typically cost more to insure.

Boat value — The more the boat is worth, the more it costs to insure the hull. This is straightforward.

Your experience as a boater — How long have you been boating? Do you have safety courses on your record? Some carriers offer discounts for completing recognized boating safety courses like those offered through the US Coast Guard Auxiliary or US Power Squadrons.

Age and condition of the boat — Newer boats in good condition are generally easier to insure at competitive rates. Older boats, or boats with deferred maintenance, can be harder to place and more expensive.

Navigation area — Offshore and coastal coverage costs more than inland-only coverage because the risks are higher and rescue or salvage costs are much greater.

Where you store the boat — Boats stored in a secure facility are lower risk than boats sitting unprotected. Marina slip? Dry stack? Backyard on a trailer? These all factor in differently.

Your claims history — Prior claims, especially multiple ones, will affect your premium.

Coverage limits and deductibles — Higher liability limits and agreed value coverage cost more. Higher deductibles lower your premium.

Safety equipment — Fire extinguishers, GPS, VHF radio, life jackets, and other safety equipment onboard can sometimes affect the rate.

For most recreational boats in the 18-26 foot range, annual boat insurance premiums generally fall somewhere between a few hundred and a couple thousand dollars. Smaller simpler boats can be much less. Larger, higher-value vessels — offshore boats, yachts, houseboats — can be considerably more. The only way to know for your specific situation is to get actual quotes.

Personal Watercraft — The Jet Ski Question

Personal watercraft (PWC) — jet skis, Sea-Doos, WaveRunners — are a category of their own. They’re fast, they’re maneuverable, and they get into trouble easily. The liability exposure on a PWC is real, and they’re involved in a disproportionate share of boating accidents relative to their numbers.

Some boat insurance policies will cover PWC alongside a larger vessel, but most carriers prefer to write them separately. If you have a PWC in addition to a boat, ask specifically about how the coverage works — don’t assume the boat policy extends to it automatically.

Also worth noting: homeowners policies almost universally exclude PWC from any kind of meaningful coverage. If you’re riding a jet ski and assuming your homeowners has you covered, it probably doesn’t.

What’s Typically Excluded

Even a comprehensive boat policy has exclusions. Common ones to know about:

Wear and tear — Insurance is for sudden, accidental damage, not the slow deterioration that comes from normal use and age. If your engine fails because it wasn’t maintained, that’s not a covered loss. If it gets destroyed in a crash, that is.

Manufacturer defects — A manufacturing defect in the hull, motor, or components is a warranty issue, not an insurance issue.

Racing — Most standard boat policies exclude coverage when the boat is being used in racing or speed events. If you race your boat, you need to disclose that and make sure you have appropriate coverage for it.

Intentional damage — Damage you caused intentionally isn’t covered. This one should be obvious but is worth saying.

Commercial use — If you’re charging passengers for rides or using the boat for a charter fishing business, a standard recreational boat policy probably won’t cover it. Commercial use requires commercial marine coverage.

Gradual damage — Osmotic blistering in fiberglass hulls, gradual through-hull fitting corrosion, slow leaks — these fall outside the scope of sudden-loss coverage.

A Few Things That Catch Boaters Off Guard

The liveaboard situation — If you live on your boat, that changes everything about how it needs to be insured. Most recreational boat policies exclude liveaboard situations. If the vessel is your primary residence, you need a policy that specifically addresses that.

Salvage costs — If your boat sinks or runs aground and needs to be recovered, salvage costs can be significant and aren’t always fully handled the way you’d expect. Understand how your policy responds to salvage before you need it.

Pollution liability — If your boat leaks fuel or oil into the water and environmental cleanup is required, some policies include this coverage and some don’t. For larger vessels especially, this is worth checking on.

Named insured vs. permitted operators — If you regularly let friends or family take the boat out without you, make sure your policy covers other operators. Some policies restrict who can operate the vessel.

Why Shop Marine Coverage With an Independent Agency

We’re independent, which means we work with multiple carriers — not just one. When we shop your boat insurance, we’re actually comparing options for you instead of just plugging you into whatever one company has available. That matters in a specialty market like marine insurance because carriers can be pretty different in terms of what they cover, how they value boats, and what they charge.

More than that, we actually take the time to understand your situation. What kind of boat you have, how you use it, where you keep it, how often you’re on the water — all of that affects what kind of policy actually makes sense. We’re going to ask the right questions so we don’t end up finding you a policy that looks good on paper but leaves you exposed in some area that matters to you.

Boat insurance isn’t the most complicated thing in the world, but it’s also not something you want to get wrong. Give us a call or reach out online. We’d love to help you find something that actually protects the boat you worked hard for.