Starting a Livery Business Is Exciting — The Insurance Part Less So

Starting a limo or car service business is one of those things that sounds glamorous on the outside. Nice vehicles, happy clients, events, airport runs, weddings, corporate accounts — there is a lot to like about it. But then you start digging into the business side of things and realize pretty quickly that there is a whole other world of compliance, licensing, and insurance requirements waiting for you.

Livery insurance is one of the first and most important things you need to figure out before you put a single passenger in your vehicle. And it’s not something you can just skip or piece together with a regular personal auto policy. The moment you start carrying passengers for a fee, you are in commercial territory, and the insurance requirements change significantly.

That is exactly why Uncle Sheldon started working with livery operators. We are an independent insurance agency and brokerage, and we have access to many different carriers who write this class of business. We can help you understand what coverages you actually need, shop your options, and get you set up properly so you can focus on building your business instead of drowning in paperwork and confusing insurance jargon.

What Is Livery Insurance?

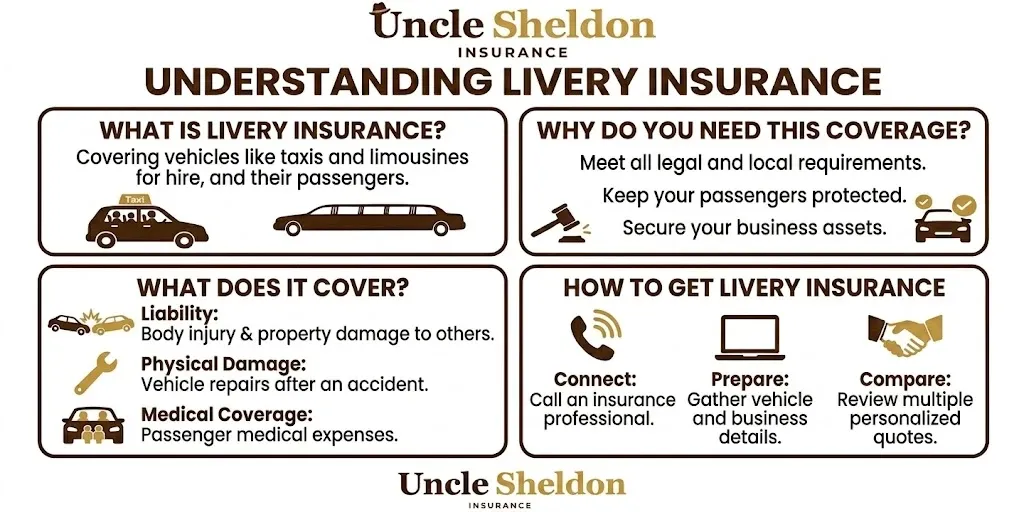

Livery insurance is a type of commercial auto and transportation insurance designed specifically for businesses that transport passengers for a fee. The word “livery” is an old term that originally referred to the horse and carriage businesses that would transport people from place to place — today it covers a wide range of for-hire transportation businesses.

If you are operating any of the following, you are likely in the livery category and need specialized coverage:

- Limousine services

- Black car or luxury car services

- Airport shuttle operations

- Charter bus or minibus businesses

- Sedan or car service companies

- Wedding and special event transportation

- Corporate transportation services

- Non-emergency medical transportation (NEMT)

- Tour buses and sightseeing operations

The common thread is that you are transporting paying passengers in a vehicle you operate as a business. That distinction — passengers for hire — is what takes you out of personal auto coverage territory and puts you squarely into commercial livery insurance.

Why a Regular Auto Policy Won’t Cut It

This is something a lot of new livery operators find out the hard way. A standard personal auto policy has language that specifically excludes coverage when the vehicle is being used to transport passengers for compensation. It doesn’t matter how good your personal auto policy is or how much you pay for it — if you are running a car service and something happens while you have a fare in the vehicle, that personal policy is almost certainly not going to respond to the claim.

The same is true for a standard commercial auto policy that isn’t written specifically for livery use. Not all commercial auto is the same. A contractor using a pickup truck for work has a very different risk profile than a limousine driver shuttling wedding guests around on a Saturday night. The insurance products that cover those two operations are different, and trying to cover a livery operation with the wrong type of commercial auto policy is a coverage gap waiting to cause problems.

A proper livery policy is written with the understanding that you are carrying fare-paying passengers, and it prices and covers the risk accordingly. It also satisfies the regulatory requirements that most states and municipalities place on for-hire transportation businesses.

The Coverages That Make Up a Livery Insurance Program

Like trucking or any other specialty transportation insurance, livery coverage is usually not a single policy but a combination of coverages that work together to protect your business, your vehicles, your drivers, and your passengers. Here’s what you’ll typically be looking at.

Commercial Auto Liability

This is the foundation. Commercial auto liability covers bodily injury and property damage that your business causes to third parties — other drivers, pedestrians, property — when one of your vehicles is involved in an accident where you are at fault. It’s the coverage that pays for the other person’s medical bills and vehicle repairs when your driver causes a collision.

The liability limits required for livery operations are typically higher than what you’d see in a personal auto policy, for good reason. You are responsible for passengers, and the potential for significant bodily injury claims is very real. Most state public utility commissions or transportation regulatory bodies that oversee for-hire vehicles set minimum liability requirements that are considerably higher than minimum personal auto requirements.

Depending on your state, the type of vehicles you operate, and who you are contracting with, you may need $1 million or more in per-occurrence liability coverage. Some large corporate contracts or venue contracts require even higher limits.

Uninsured and Underinsured Motorist Coverage

Even if your own drivers are excellent, not everyone else on the road is. Uninsured motorist coverage protects you and your passengers if you are hit by a driver who has no insurance. Underinsured motorist coverage kicks in when the at-fault driver has some insurance but not nearly enough to cover the full extent of the damages. Given that you are responsible for passengers who have hired you for safe transport, having solid UM/UIM coverage is important.

Physical Damage

Physical damage covers your actual vehicles — the limousines, sedans, shuttles, or buses that you own. Collision coverage takes care of accident damage, and comprehensive coverage handles theft, fire, vandalism, weather events, and other non-collision losses. If you have loans or leases on your vehicles, your lender is going to require you to carry physical damage coverage. And even if you own your fleet outright, losing a $70,000 or $100,000 vehicle to a total loss without coverage is a devastating financial event for any small operation.

Hired and Non-Owned Auto

If your operation ever involves drivers using vehicles that your business doesn’t directly own — renting vehicles, using a driver’s personal vehicle, contracting with outside drivers who use their own cars — you have exposure that your owned-auto policy doesn’t cover. Hired and non-owned auto coverage fills that gap. It covers liability arising from vehicles that are used in connection with your business but aren’t in your fleet.

General Liability

Commercial general liability protects your business from a range of incidents that don’t involve vehicle accidents. Slip and fall injuries on your premises, property damage you cause while not operating a vehicle, bodily injury claims that arise out of your business operations but not specifically from driving — these all fall under general liability. Many contracts with hotels, venues, event coordinators, and corporate clients will require you to carry a general liability policy as a condition of working with them.

Workers Compensation

If you have employees — including drivers you have on payroll — most states require you to carry workers compensation coverage. Workers comp covers medical expenses and lost wages for employees who are injured on the job. Driving for a living carries real physical risks, and an injured driver without workers comp coverage creates serious legal and financial exposure for your business.

If you are operating as a sole proprietor with no employees, you may be exempt from the workers comp requirement in your state. But the moment you hire someone, you almost certainly need it.

Umbrella and Excess Liability

For livery businesses that need higher overall liability limits than their primary policies provide, or for operators who carry passengers in large vehicles and face correspondingly large potential claims, an umbrella or excess liability policy sits on top of your underlying coverage and provides an additional layer of protection.

A large passenger van or charter bus involved in a serious accident could generate claims that exceed a standard primary policy limit. Umbrella coverage ensures you have adequate protection for those worst-case scenarios.

The Bond Question

If you are getting started in the livery business, there’s a reasonable chance you’ll encounter a requirement for a surety bond at some point. Certain state or municipal licensing bodies require livery or transportation network operators to carry a surety bond as part of getting licensed.

A surety bond is not the same as insurance, though the two are often discussed together. A bond is a financial guarantee — it tells the entity requiring it that your business will comply with the terms of your license or contract, and if it doesn’t, the bonding company will step in to cover any resulting losses up to the bond limit.

Uncle Sheldon can help you find a surety bond if your livery business requires one. It’s not something you have to figure out separately — we can work on both the insurance and the bonding side of things in one conversation, which makes the whole setup process a lot less painful.

State and Local Regulatory Requirements

One of the more frustrating aspects of getting into the livery business is that the regulatory landscape varies significantly from state to state, and even from city to city. What’s required to operate a limousine in one state might be completely different from what’s required two states over.

Most states have a public utilities commission, department of transportation, or similar regulatory body that oversees for-hire passenger transportation. These agencies typically require:

- Proof of insurance with specific minimum limits

- A business license or operating permit for transportation services

- Vehicle inspections and certifications

- Driver background checks and licensing requirements

- Sometimes a surety bond

Municipal regulations add another layer on top of state requirements. Operating in a major city often comes with its own permitting requirements, and certain airports and venues have specific insurance and credentialing requirements for transportation companies that want to operate on their premises.

This is one of the real practical advantages of working with an experienced independent agency when you are getting started. We have seen these requirements across different states and operations, and we can help you understand what filings and coverage documents you’ll likely need to satisfy your regulatory obligations. We don’t know every state’s requirements by heart, but we know how to work through them with you and find the right carriers that can issue the documentation regulators actually accept.

Types of Livery Operations and How Coverage Differs

Not all livery businesses are the same, and the coverage needs can differ in meaningful ways depending on what kind of operation you’re running.

Limousine and Luxury Car Services

Traditional limo services — stretch limousines, luxury sedans, high-end SUVs — are typically focused on events, special occasions, airport transfers, and corporate travel. The vehicles are high-value, which matters for physical damage coverage. The clientele often includes alcohol at events, which can raise liability considerations. Hours of operation tend to skew toward evenings and weekends for event work, though corporate accounts might be regular business-hours runs.

Premium vehicles and premium clients come with expectations of a professional, polished operation. Your insurance program needs to match that.

Airport Shuttle Operations

Shuttle businesses are often high-volume operations — lots of trips, lots of passengers, and very regular schedules. The per-trip revenue is lower than a limo run but the volume is higher. Shuttles often operate with set routes between hotels, parking facilities, and airport terminals.

Regulatory requirements around airports tend to be particularly specific. Many airports require operators to be credentialed and carry specific insurance limits before they can pick up passengers on airport property. If you are planning to run an airport shuttle, understanding the specific requirements of the airports you’ll be servicing is an early and important step.

Charter Bus and Minibus Operations

As you move from sedans and limos into vans, minibuses, and full-size motor coaches, the risk profile changes. You have more passengers per vehicle, which means more potential for large multi-party injury claims in an accident. Physical damage coverage values go up significantly for a full-size coach.

Charter bus operations also often cross state lines, which brings in federal regulatory considerations similar to commercial trucking. FMCSA operating authority and associated insurance filings may apply depending on how and where you operate.

Non-Emergency Medical Transportation

NEMT is a specialized segment of the livery world. These operations transport passengers — often elderly individuals, patients with disabilities, or people recovering from medical procedures — to and from medical appointments. It’s not emergency ambulance service, but it serves a genuinely vulnerable population.

NEMT operations often have specific state Medicaid program requirements around insurance coverage if they participate in those programs. The nature of the passengers being transported can also create specific liability considerations around assistance during boarding and exiting vehicles.

Rideshare and On-Demand Models

The rise of app-based rideshare services created some interesting insurance complications across the industry. If you are operating your own independent car service — not as a driver for a major rideshare platform — you are in the livery category and need commercial livery coverage.

If you are a driver for a major rideshare platform, those companies typically provide some coverage while you are actively on a trip, but there are coverage gaps — particularly between when you turn on the app and when you actually accept a ride — that personal auto policies often don’t cover either. Gap coverage products exist for rideshare drivers to fill those specific windows. This is a distinct situation from running your own livery business, but it’s worth mentioning because the two categories get confused.

Building Your Fleet and Insurance at the Same Time

A lot of people who start livery businesses start small — maybe one vehicle, maybe themselves as the only driver. The smart move is to get the insurance program right from day one, even when the operation is small. Here’s why.

First, it’s required. You can’t legally operate a for-hire passenger vehicle without the proper commercial insurance in place. Getting caught without it doesn’t just mean a claim gets denied — it means fines, potential suspension of operating permits, and personal liability exposure.

Second, your claims history matters. Starting a clean record as a livery operator and maintaining it is worth real money in premium savings over time. Insurers look at your loss history when they price renewals or when you move to a new carrier. Running a safe, professional operation from day one pays off financially.

Third, coverage gaps created by cutting corners early tend to reveal themselves at the worst possible moments. An incident with an injured passenger in month three of a new operation, with inadequate or wrong-type coverage, can be financially catastrophic. Getting the coverage right from the start avoids that scenario entirely.

What Livery Insurance Actually Costs

Livery insurance pricing is highly variable because the risk factors involved are highly variable. A single-vehicle sedan operation doing corporate airport transfers in a mid-sized city is priced very differently from a five-coach charter bus company running multistate tours.

The factors that most affect your premium include:

Vehicle type and value — A stretch limousine or a motor coach represents a much larger physical damage exposure than a standard sedan. The type of vehicle also signals the type of work being done and the potential severity of accident claims.

Number of vehicles and drivers — More vehicles and more drivers means more exposure and correspondingly higher premium. Fleet discounts can apply at certain size thresholds, but more units generally mean higher total cost.

Driver records — This is one of the most important factors. Clean driving records across your driver pool lower your cost significantly. Prior accidents, serious violations, or DUI history will raise your rates substantially or make certain carriers unwilling to write you at all.

Operating area — Urban operations with heavy traffic, higher accident frequency, and higher medical costs are priced differently than rural or suburban operations. Certain cities and states are simply more expensive to insure in.

Type of service — The nature of the trips you run matters. High-volume airport shuttles, event transportation with alcohol present, long-distance charter trips — these have different risk profiles and are priced accordingly.

Passenger counts — Larger vehicles carrying more passengers at once carry more liability exposure per accident. A van with fifteen passengers in an accident has more potential injury claims than a sedan with one passenger.

Annual mileage — More miles means more exposure. Carriers want to know how much you’re driving.

Prior claims history — If you’ve had prior claims, expect them to affect your pricing. If you are brand new with no history, that can actually be a neutral or even slightly positive factor with some carriers.

The honest answer on cost is that you need a real quote based on your real operation to get a meaningful number. Anyone who gives you a definitive price without knowing all these details isn’t being straight with you. At Uncle Sheldon, we gather the information we need to go out and actually shop your risk across carriers who write livery business, so the quotes you get are real and relevant.

The Difference Between Getting It Right and Getting Close

There is a meaningful difference between a livery insurance program that is genuinely right for your operation and one that looks adequate on paper but has gaps that matter when something goes wrong. The difference often lives in the details — the specific form language in a cargo or liability policy, whether your vehicle schedule is accurate and up to date, whether your driver list reflects everyone actually operating vehicles for your business, whether the coverage territory matches where you actually operate.

Working with an independent broker who understands transportation businesses means having someone in your corner who knows what those details are and pays attention to them. We use technology to make the quoting and documentation process more efficient, but the actual work of understanding your operation and making sure your coverage is right is done by real people who care about getting it right.

We are transparent with our clients. If we find that a carrier isn’t the right fit for your operation, we’ll tell you. If there’s a coverage gap we can’t fill with the markets we have access to, we’ll tell you that too and try to point you toward someone who can help. We’re not in the business of just getting your signature and moving on. We want your business covered properly and we want you to come back to us when your operation grows.

Getting Started

If you are starting a livery business or if you’ve been operating for a while and want to make sure your coverage is solid, the conversation starts the same way — we need to understand your operation. When you reach out, it helps to have a general sense of the following:

- What type of service you are running (limos, shuttles, charter buses, etc.)

- How many vehicles you have or plan to have, and the year, make, model, and value of each

- How many drivers you have, whether they are employees or contractors, and their general driving history

- Where you operate and what states or cities you work in

- The types of clients and events you typically serve

- Your annual or estimated mileage

- Any specific contracts or venues that have insurance requirements

- Whether you need a surety bond as part of your licensing

You don’t need to have every detail perfectly organized before you call. We can work through it together. The goal of that first conversation is just to understand what you’re doing well enough to go find the carriers and coverages that make sense for you.

Getting going in the livery business is an exciting adventure. Make sure that adventure is covered so that when something unexpected happens — and eventually, something always does — you have the protection in place to keep your business moving forward.

Give Uncle Sheldon a call or reach out online. We’re real people, and we’re here to help you get this right.