More Than Just Checking a Box

Car insurance is one of those things everyone has to have, so a lot of people treat it like a commodity — just find the cheapest option and move on. We understand that. But cheap coverage that doesn’t actually protect you when something happens isn’t really coverage at all. It’s a false sense of security.

The way car insurance works, the coverage types you carry, and the limits you set all matter a lot when you actually need to use it. An accident that costs $80,000 in medical bills and vehicle damage, and you’re carrying $25,000 in liability limits because that was the state minimum — that gap is coming out of your pocket personally. That’s the kind of thing people don’t think about until it’s too late.

At Uncle Sheldon, we’re an independent agency. We work with multiple carriers, which means we’re shopping for the right fit for you rather than pushing you toward one company’s product. And we’re real people who will take the time to explain what you’re buying. That’s the difference.

The Coverage Types That Make Up a Car Insurance Policy

Car insurance isn’t one single coverage — it’s a package of several different coverage types. Some are required by law, some are optional, and some depend on your specific situation. Here’s what each one does.

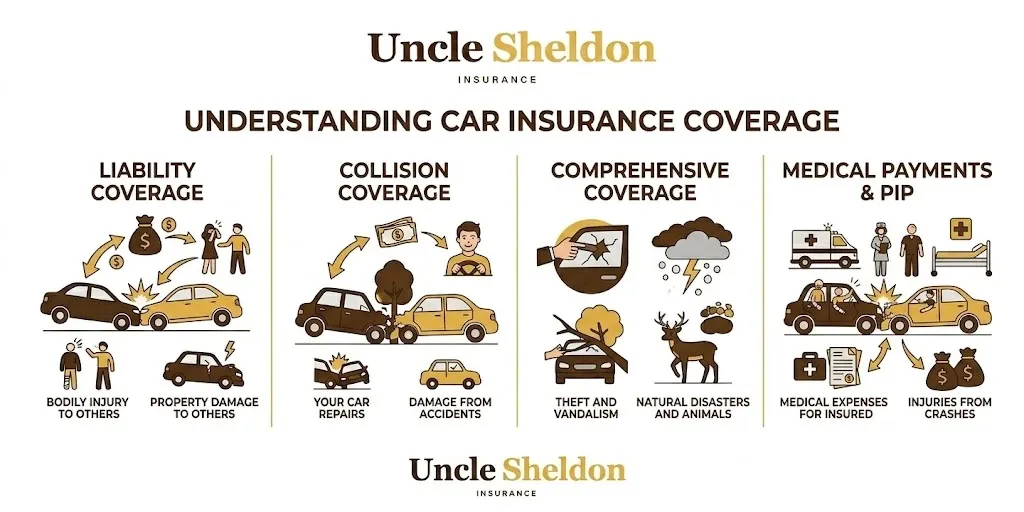

Liability Coverage

Liability is the foundation of any auto policy and it’s required in almost every state. It covers bodily injury and property damage you cause to other people when you’re at fault in an accident.

There are two components:

Bodily Injury Liability pays for injuries to other people — medical bills, lost wages, pain and suffering — when you cause an accident. It does not pay for your own injuries.

Property Damage Liability pays for damage to other people’s vehicles or property — their car, a fence, a building — when you’re at fault.

Liability limits are usually written as three numbers, like 50/100/50. That means $50,000 per person for bodily injury, $100,000 per accident for bodily injury, and $50,000 for property damage.

State minimum liability requirements are very low in most states. Like, uncomfortably low. A serious accident involving injuries can easily generate six figures in medical bills and damages. If your liability limits are exhausted, you’re personally responsible for the rest. This is one of the most important conversations to have when setting up an auto policy.

Collision Coverage

Collision coverage pays to repair or replace your own vehicle when it’s damaged in a collision — whether you hit another car, a tree, a guardrail, or another object. It also applies if your parked car gets hit by someone who drives off.

Collision coverage has a deductible — an amount you pay out of pocket before the coverage kicks in. Common deductibles are $500, $1,000, or $1,500. Higher deductible = lower premium but more out of pocket when you file a claim.

If you’re financing or leasing your vehicle, your lender almost certainly requires you to carry collision coverage. They have a financial interest in the vehicle and want to make sure it can be repaired or replaced.

For older vehicles with lower market value, the math on collision coverage sometimes doesn’t work out. If your car is worth $3,000 and your deductible is $1,000, the maximum you’d collect in a total loss is $2,000 — and you’re paying collision premiums for that. At some point it may make more sense to drop collision on an older, low-value car.

Comprehensive Coverage

Despite the name, comprehensive doesn’t cover everything. It covers damage to your vehicle from causes other than a collision — theft, vandalism, fire, flood, hail, falling objects, hitting an animal. The things that happen to your car that aren’t another vehicle collision.

Like collision, comprehensive has a deductible. And like collision, lenders require it if you’re financing.

Comprehensive and collision are often sold together and collectively referred to as “full coverage” — though that term isn’t really a precise insurance term. What people usually mean when they say full coverage is a policy that includes liability, collision, and comprehensive.

Uninsured and Underinsured Motorist Coverage

This one is more important than a lot of people realize. Uninsured motorist coverage (UM) protects you if you’re hit by a driver who has no insurance at all. Underinsured motorist (UIM) covers you when the at-fault driver doesn’t have enough liability coverage to fully pay for your injuries or vehicle damage.

The number of uninsured drivers on the road is significant. Depending on the state, estimates range from the mid single digits up to a quarter or more of drivers having no insurance. If one of them hits you and seriously injures you, without UM coverage you’re looking at recovering damages from someone who likely doesn’t have meaningful assets to go after.

UM/UIM is required in some states and optional in others. Even where it’s optional, it’s usually worth carrying.

Medical Payments and Personal Injury Protection

Medical Payments (MedPay) covers medical expenses for you and your passengers after an accident, regardless of who’s at fault. It’s a relatively simple coverage — it just pays medical bills up to the coverage limit.

Personal Injury Protection (PIP) is similar but broader. In addition to medical expenses, PIP can cover lost wages, rehabilitation costs, and in some cases even funeral expenses. PIP is required in no-fault states and optional or unavailable in others.

Whether you need MedPay or PIP on your auto policy depends partly on your health insurance situation. If you have solid health insurance with low out-of-pocket costs, MedPay may be less critical. If your health insurance has a high deductible, having MedPay to cover that gap after an accident makes more sense.

Gap Insurance

Gap insurance is relevant if you’re financing a vehicle and the loan balance is higher than the car’s current market value. This happens most often with new cars — the moment you drive off the lot, the vehicle depreciates and may be worth less than what you owe on it.

If your financed car gets totaled, your insurance pays the actual cash value of the vehicle at the time of loss — not what you paid for it, not what you owe on the loan. If that payout is less than your loan balance, you’re still responsible for the difference. Gap insurance covers that difference.

Many dealerships offer gap coverage when you finance, but it’s often available more affordably through your insurance carrier or a third party. Worth comparing before you just accept what the dealer offers.

Quick Coverage Reference

| Coverage Type | What It Pays For | Required? |

|---|---|---|

| Bodily Injury Liability | Injuries you cause to others | Yes, in almost every state |

| Property Damage Liability | Damage you cause to others’ property | Yes, in almost every state |

| Collision | Damage to your vehicle in a collision | Required by lenders; optional otherwise |

| Comprehensive | Non-collision damage (theft, weather, etc.) | Required by lenders; optional otherwise |

| Uninsured Motorist | Your injuries/damage caused by uninsured driver | Required in some states |

| Medical Payments / PIP | Your medical expenses after an accident | Required in no-fault states; varies otherwise |

| Gap Insurance | Difference between loan balance and car’s value | Never required; smart if you’re underwater on loan |

What Affects Your Car Insurance Premium

Rates vary a lot between drivers — even drivers in the same city with similar cars. Here’s what insurance companies look at when they price your policy:

Your driving record. Accidents and violations stay on your record for typically three to five years depending on the carrier and state. A DUI can affect rates for significantly longer. A clean record is one of the biggest factors in keeping premiums manageable.

Your age. Younger drivers, especially teens and early twenties, pay the highest rates because statistically they have more accidents. Rates generally improve as drivers build a clean record through their twenties and into their thirties.

Where you live. Your zip code matters — urban areas with higher traffic density, theft rates, and accident frequency result in higher premiums. Even moving a few miles can sometimes affect rates.

Your vehicle. What you drive affects both collision and comprehensive rates. Expensive vehicles cost more to repair or replace. Vehicles with poor safety ratings or high theft rates can cost more to insure. Safety features and anti-theft systems can sometimes help.

How much you drive. Annual mileage matters. Someone who drives 5,000 miles a year is a different risk than someone who drives 25,000.

Your credit score. In most states, insurance companies use a credit-based insurance score as a pricing factor. Better credit typically means better rates. This is separate from your financial credit score but is based on similar underlying data.

Coverage limits and deductibles. Higher limits cost more. Higher deductibles lower your premium. Both choices have real tradeoffs.

Your claims history. Prior claims — especially at-fault claims — can affect your rate for several years.

How Much Liability Coverage Is Enough

This is one of the most important questions in car insurance and there’s no perfect universal answer. But the thinking around it is pretty straightforward.

Your liability limits need to be high enough to protect your personal assets if you cause a serious accident. If your net worth is $500,000 — savings, investments, home equity, retirement accounts — and you’re carrying $50,000 in liability, a major accident could result in a judgment that puts all of that at risk.

Liability coverage is also one of the cheapest parts of your auto policy relative to the protection it provides. Doubling your liability limits often costs less than you’d expect in additional premium. It’s worth pricing out.

A 100/300/100 split limit — $100,000 per person bodily injury, $300,000 per accident, $100,000 property damage — is a common recommendation as a reasonable baseline for most drivers. Higher limits make sense if you have significant assets to protect.

For drivers with substantial assets, an umbrella liability policy that sits on top of both your auto and home policies is another option that can provide a million dollars or more in additional coverage for a relatively modest annual premium.

Discounts Worth Asking About

Most insurance companies offer a variety of discounts. Not all of them are advertised prominently, so it can be worth asking specifically about what’s available.

- Multi-policy (bundling) — insuring your car and home or renters policy with the same carrier

- Multi-car — insuring more than one vehicle on the same policy

- Good driver — maintaining a clean record for a certain number of years

- Good student — for younger drivers with qualifying grades

- Defensive driving course — completing an approved course

- Anti-theft devices — certain security features on the vehicle

- Low mileage — driving below a certain annual threshold

- Pay in full — paying the policy term upfront rather than monthly

- Paperless / automatic payment — some carriers offer small discounts for these

Discounts vary widely by carrier. One of the advantages of working with an independent agent is that we can compare how each carrier’s discount structure applies to your specific situation.

Switching Car Insurance Carriers

People switch car insurance companies for a lot of reasons — a rate increase at renewal, a bad claims experience, or just wanting to shop around. A few things to know if you’re considering switching:

You can switch at any time during your policy term. If you switch before the renewal date, you’re typically entitled to a prorated refund on the unused portion of your premium.

Don’t cancel your old policy until the new one is confirmed active. A lapse in coverage — even a short one — can affect your rates with future insurers.

If you’ve had continuous coverage for a number of years with no lapses, that’s actually a positive factor with many carriers. Don’t interrupt that history unnecessarily.

When comparing quotes, make sure you’re comparing equivalent coverage. A quote that looks dramatically cheaper might be carrying lower limits or a higher deductible. Make sure you’re looking at the same coverage levels before drawing conclusions about price differences.

Working With Uncle Sheldon on Car Insurance

We shop your auto insurance across multiple carriers to find the right combination of coverage and price for your situation. We’re not limited to one company’s products, which means we’re actually looking for what fits you rather than just what we have available.

We’ll also make sure you understand what you’re buying. Not everyone knows the difference between uninsured motorist and underinsured motorist, or why the numbers in a split limit work the way they do. We’ll walk through it so you’re not just signing up for something you don’t fully get.

Whether you’re insuring one car or a household with multiple vehicles, reach out to us. We’re here to help find coverage that makes sense — real agents, not a robot.