What a Performance Bond Is and Why It Exists

A performance bond is a type of surety bond that guarantees a contractor will complete a construction project in accordance with the terms of the contract. If the contractor fails to perform — whether because they abandon the job, go out of business mid-project, or simply don’t deliver what was promised — the surety company steps in to make the project owner whole.

It’s a protection mechanism for project owners, and it’s a pretty significant one. Construction projects involve large sums of money, long timelines, and a lot of moving pieces. The project owner — whether that’s a government agency, a school district, a municipality, a developer, or a private company — is taking on real risk when they award a contract. A performance bond transfers a significant portion of that risk to a third party, the surety, who has already vetted the contractor through an underwriting process.

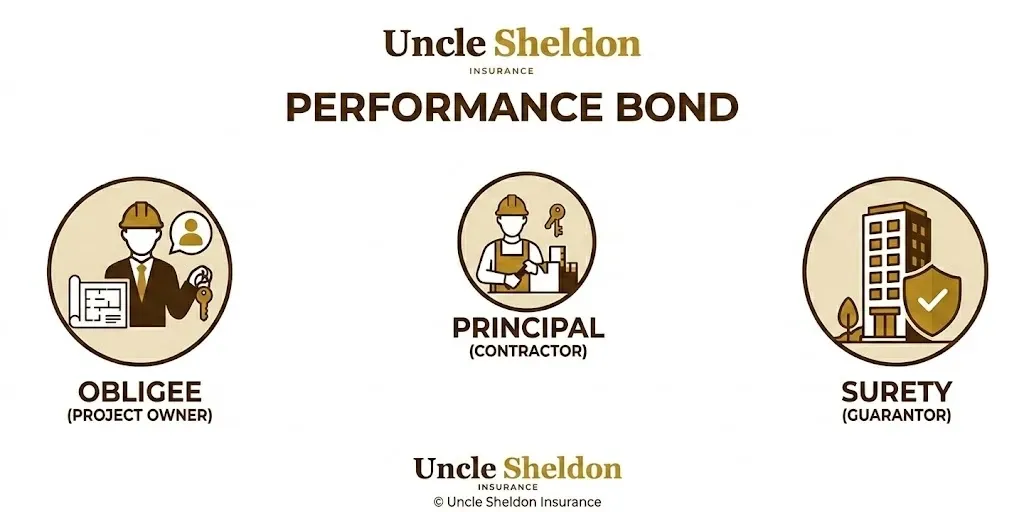

Like all surety bonds, a performance bond involves three parties. The principal is the contractor who is obligated to complete the work. The obligee is the project owner who is requiring the bond and who would benefit from a claim. And the surety is the bonding company that backs the guarantee.

Here’s the thing that trips people up when they’re new to surety bonds: a performance bond is not insurance for the contractor. It’s a financial guarantee. If the surety pays out on a valid claim, the contractor is still legally obligated to repay the surety. The risk doesn’t just disappear. The surety is not absorbing the contractor’s failure the way an insurance company absorbs a loss — they’re covering the project owner and then turning around and recovering from the contractor. Understanding that distinction matters a lot, especially when things go wrong.

Who Actually Needs a Performance Bond

The most common answer is contractors bidding on public construction work, but it goes beyond that.

Federal Construction Projects

At the federal level, the Miller Act is the governing law. It requires contractors who are awarded federal construction contracts valued above $150,000 to furnish both a performance bond and a payment bond. No exceptions. The bond amounts are typically set at one hundred percent of the contract value. If you’re doing work for the federal government above that threshold, performance bonds are non-negotiable.

State and Local Government Projects

Most states have what are called Little Miller Acts — state statutes that mirror the federal law and apply to state, county, and municipal projects. The specific thresholds vary by state. Some states set the threshold at $25,000, others higher. But if you’re pursuing public works contracts at any level of government in most of the country, you’re going to encounter performance bond requirements regularly. It’s just part of doing that kind of work.

Private Construction Projects

Performance bonds aren’t strictly a government thing. Large developers, commercial real estate owners, lenders financing construction projects, and private project owners who’ve been burned before often require performance bonds on private work too. If a bank is financing a major commercial build, they may require the general contractor to be bonded as a condition of the construction loan. It’s increasingly common in the private market for significant projects.

Subcontractors

General contractors who are bonded on a project sometimes require their key subcontractors to furnish performance bonds as well. If the GC is on the hook to the owner for completing the entire project, it makes sense for them to protect themselves on the subcontractor side. Subcontract performance bonds follow the same basic logic as prime contract performance bonds — they’re a guarantee of the sub’s performance on their scope of work.

Design-Build and Other Delivery Methods

As project delivery methods have evolved, so have bonding requirements. Design-build contracts, construction manager at-risk arrangements, and public-private partnerships all have their own bond structures. The underlying concept of a performance bond is the same, but the form and how it applies can differ. If you’re working in one of these delivery methods, it’s worth understanding how the bonding requirements are specifically structured for that contract type.

Performance Bonds and Payment Bonds — These Go Together

Performance bonds are almost always paired with payment bonds, and it’s important to understand the difference between the two because they protect different parties.

A performance bond protects the project owner. It’s a guarantee that the work will get done. If the contractor walks off the job or fails to deliver, the owner has a bond to make a claim against.

A payment bond protects the subcontractors, suppliers, and laborers who contribute to the project. It guarantees that these second and third-tier parties will actually get paid. This matters enormously on public projects because subcontractors and suppliers on government-owned property can’t file a mechanic’s lien the way they could on private property. The payment bond is their primary remedy when a general contractor doesn’t pay them.

On federal and most state public projects, both bonds are required together. The Miller Act requires both. The bond forms are separate, but they’re underwritten as a package and they’re typically issued at the same time, at contract award.

When contractors talk about “getting bonded” on a public project, they usually mean the full package — performance bond plus payment bond, both written for the full contract value.

How Performance Bond Claims Work

This is the part that matters most when things go wrong, and it’s worth understanding clearly even if you hope you never need to use this knowledge.

If a contractor defaults on a project — fails to make progress, abandons the work, becomes insolvent, is terminated for cause — the project owner notifies the surety in writing and makes a formal claim on the performance bond. The specific notice requirements and timing can matter, so project owners who find themselves in this situation should read their bond form and follow the required procedures carefully.

Once a valid claim is made, the surety has options. Under most modern performance bond forms, the surety has the right to investigate the claim before taking action. They’ll look at the project status, review the contract and correspondence, assess the contractor’s situation, and determine whether the default is legitimate and whether the owner has properly performed their own obligations under the contract.

If the surety accepts the claim, they typically have a few paths forward. They can arrange for the defaulted contractor to complete the work with surety financial support — sometimes the contractor is in a recoverable situation if they get help with cash flow. They can find a new contractor to complete the remaining work and manage that completion. They can tender a payment to the project owner to complete the work themselves. Or in some cases they can simply pay the project owner the damages up to the bond amount.

The surety’s choice of completion method matters a lot to the project owner. A surety that takes an active role in getting the project completed is more valuable than one that just writes a check and walks away, because getting the project done is usually what the owner actually needs. That’s one reason why the financial strength and reputation of the surety behind the bond matters.

From the contractor’s side: if you’re in financial trouble on a job and you think a default might be coming, the single most important thing you can do is contact your surety and your bonding agent immediately. Don’t wait for the owner to call the bond. Sureties often prefer to work with a struggling contractor to get a project completed rather than deal with a formal claim, and they may have resources — legal, financial, technical — that can help. But they can only help if they know there’s a problem. Surprises are bad in surety relationships.

The Underwriting Process for Performance Bonds

Getting a performance bond isn’t like buying a standard insurance policy where you fill out an application and get a quote in minutes. Surety underwriting is a real evaluation of your business, and for larger bonds it can be a pretty thorough one.

The framework underwriters use is often described as the three C’s: capital, capacity, and character. These aren’t just buzzwords — they’re actually the three things the surety is trying to evaluate when they decide whether to issue your bond and at what terms.

Capital

Capital means your financial strength. The surety is looking at your balance sheet, your working capital, your net worth, your debt levels, and your profitability history. They want to know whether your business has the financial resources to absorb problems and still complete a project if things don’t go perfectly.

For smaller bonds, a personal financial statement or basic company financials might be sufficient. For larger bonds — once you’re getting into six-figure and seven-figure bond amounts — most sureties want CPA-prepared financial statements. Depending on the size and the surety, that might mean compiled statements, reviewed statements, or in some cases audited statements. The larger the bond program you’re seeking, the more rigorous the financial requirements.

Sureties also pay attention to trends. A business that has been growing steadily and improving its financial position is viewed more favorably than one whose numbers are heading the wrong direction, even if the current balance sheet looks okay.

Capacity

Capacity is your ability to actually do the work. It’s not just about money — it’s about people, equipment, experience, and bandwidth. A contractor who is already at full capacity on existing projects and wants to bond another large job is creating real risk that the surety is going to look at carefully.

Underwriters look at your current work in progress, your backlog of contracted but not-yet-started work, and whether your organization has the supervisory and field resources to take on more. They look at the types and sizes of projects you’ve successfully completed before to understand whether the job you’re bidding is within your demonstrated capability. A contractor who has completed several similar projects at similar scale is going to have a much easier time getting a bond than one who is trying to step up significantly in project size or complexity all at once.

Character

Character in the surety context means your reputation and track record. Have you completed projects on time and on budget? Do you have good relationships with project owners, architects, and engineers? Do you pay your subcontractors and suppliers on time? Are there outstanding judgments, liens, or disputes in your history?

Your personal and business credit history feeds into this. Tax liens, collection accounts, or a pattern of late payments are red flags. So is a history of disputes with project owners or design professionals, even if you ultimately prevailed. Sureties want to bond contractors who are known for doing what they say they’re going to do.

Character is the softest of the three C’s but it’s real. A contractor with strong finances and plenty of capacity but a messy track record of disputes and non-payment is going to face skepticism in the surety market.

What Affects the Cost of a Performance Bond

Performance bonds are priced as a percentage of the contract amount. The rate depends on the contractor’s financial strength, their track record, the size and complexity of the project, and the competitive environment in the surety market. For well-qualified contractors, rates can be quite favorable. For contractors with weaker financials or limited track records, rates will be higher and terms may be more restrictive.

Common rate ranges run from less than one percent of the contract amount for very well-qualified contractors on standard projects, up to two or three percent or more for higher-risk situations. On a million dollar contract, the difference between a one percent rate and a two percent rate is ten thousand dollars, so the quality of your financial presentation and your overall bonding program matters to your bottom line.

One thing worth knowing: performance bonds and payment bonds are typically written together and the combined premium is what you pay. You’re not paying separate premiums for each bond — the surety prices the contract bond package as a whole.

Getting set up with a quality surety before you have a time-pressured project can help you negotiate better rates because you’re not in a rush and the surety has had time to really understand your business.

Bond Forms and What’s Actually in Them

Not all performance bond forms are the same, and the differences can actually matter when a claim is being handled.

The American Institute of Architects has published widely-used performance bond forms. The federal government has its own required forms for work under the Miller Act. Many state agencies have their own standardized forms. Some project owners use forms drafted by their attorneys that have language specific to that project. Surety companies have their own proprietary forms as well.

Some obligees — particularly government agencies — require specific approved bond forms and won’t accept anything else. If you’re told the bond must be on a specific form, take that seriously. Submitting a bond on the wrong form can result in the bond being rejected, which can hold up contract execution.

If there’s any question about whether a particular bond form will be accepted by the obligee, it’s worth clarifying before the bond is issued. It’s a much easier fix before the bond is written than after.

The conditions in the bond form — the notice requirements, the time the surety has to respond to a claim, the options available to the surety, the exclusions — vary meaningfully from form to form. Project owners and their attorneys pay attention to these details when evaluating whether a bond actually provides the protection they need. As a contractor, it’s worth understanding at least generally what the bond you’re issuing says, because those same terms govern what happens if you’re ever in a default situation.

Bonding Capacity and Knowing Your Limits

One of the most practical things a contractor can do is understand their bonding capacity before they’re in the middle of a bid situation. Bonding capacity refers to the maximum amount of work a surety is willing to support — both on a single project basis and in aggregate across all of your active work.

Sureties set these limits based on the underwriting of your business. A contractor with strong financials, deep experience, and good project management systems might have a single project limit of five or ten million dollars and an aggregate limit of twenty or thirty million. A newer or smaller contractor might have much lower limits. Those limits are not fixed forever — they grow as your business grows and as you demonstrate a track record — but at any given time, they define the scope of work you can realistically pursue.

Knowing your limits matters for a couple of reasons. First, it helps you bid strategically. There’s no point pursuing projects that are beyond your bonding capacity, because even if you win, you can’t execute the contract. Second, it protects you from overextending. Your bonding capacity is essentially an outside expert’s opinion of how much work your business can safely take on. Ignoring that guidance can lead to real problems.

Building a Bonding Program Over Time

Performance bonding isn’t a one-time transaction. Contractors who pursue bonded work regularly have ongoing relationships with their surety and their bonding agent. Building that relationship well over time has real value.

The foundation is keeping your surety and bonding agent informed. Major business changes — key personnel leaving, a significant acquisition or sale, a project that’s experiencing problems, a year that didn’t go the way you planned financially — these are things your surety should know about from you, not from a claim notification or a bad set of financials showing up at renewal. A relationship built on transparency and communication is a more durable one.

Providing timely and accurate financial statements every year is important. Sureties are underwriting a relationship, and they need current information to maintain that relationship. Contractors who are slow with their financials or who push back on providing information make underwriters nervous. Make it easy for them to support you.

Over time, as you complete bonded projects successfully and your financial strength grows, your bonding capacity grows with it. Contractors who manage this relationship well can build substantial bonding programs that let them compete for significant public and private work. That’s a real business asset.

Working With the Right Surety Market

The surety market has a range of companies, and they’re not all the same. Treasury-listed sureties — those approved by the U.S. Treasury Department — are required on federal projects. State projects may have their own requirements. Beyond the technical requirements, the financial strength and reputation of the surety company matter.

A bond is only as good as the company behind it. If a claim is made and the surety drags its feet, disputes the claim without basis, or doesn’t have the financial resources to back it up, the bond isn’t delivering what it was supposed to. Project owners and their advisors think about this when evaluating contractor bids, and sophisticated owners sometimes specify minimum A.M. Best ratings for sureties.

For contractors, working with a financially strong surety also matters at claims time if you’re ever in trouble on a job. A well-capitalized surety with real resources can help complete a struggling project. A weaker one may just pay out and move on.

As an independent agency, Uncle Sheldon works with multiple surety markets. We’re not tied to one company, which means we can find the right fit for your situation and shop for competitive terms. We pay attention to the quality of the sureties we work with, not just the price.

Getting Started With Uncle Sheldon

If you’re a contractor who needs a performance bond — whether it’s for a specific project that just got awarded or you’re looking to build bonding capacity for future work — we’re here to help you figure out the path forward.

We work with contractors at all stages. Some are well-established with existing surety relationships who want to see if there’s a better fit or more competitive terms available. Some are newer contractors who are trying to get into bonded work for the first time and aren’t sure where to start. Some are in the middle of a complicated situation and need help sorting it out.

Whatever your situation, the first step is a conversation. We’ll ask questions about your business, your financials, your history, and what you’re trying to accomplish. From there we can give you a realistic picture of where you stand and what it’s going to take to get you the bonding capacity you need.

We’re not here to sell you something that doesn’t fit. We’re here to help you find the right surety partner and the right bonding program for your business. We are real people who work with real contractors, and we’ll be straight with you about what we’re seeing and what we’d recommend.

Performance bonds are a serious part of the construction business. Getting them right — the right surety, the right terms, the right process — makes a real difference. We take that seriously.