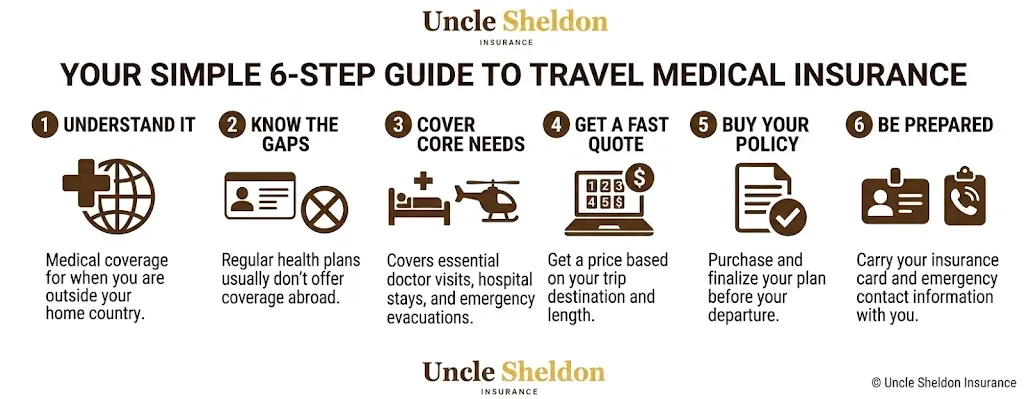

Thinking About Medical Coverage When You Travel

When most people start planning a big international trip, they spend months obsessing over the itinerary. They book the flights, find the perfect boutique hotels, and map out all the restaurants they want to hit. But what rarely makes the priority list is figuring out what happens if they get sick or injured halfway around the world.

It is easy to assume that your regular health insurance back home will just cover you if you break your leg in Costa Rica or get food poisoning in Thailand. But the reality is often a very rude awakening. Medical emergencies overseas can become absolute financial nightmares if you aren’t prepared.

That is where travel medical insurance steps in. It is a specific type of coverage designed to protect you from unexpected medical bills when you are outside your home country. We want to break down exactly what this coverage does, who actually needs it, and what you should look for when comparing options. The goal is to give you the facts so you can make a good decision and get back to planning the trip itself.

Will My Domestic Health Insurance Cover Me Overseas?

This is the most common question we get, and the answer is usually probably not, or at least not very well.

Most domestic US health insurnace plans including major carriers and employer sponsored plans provide little to no coverage outside the United States. Even if your plan does offer some international benefits, it is almost always treated as out of network. That means you are looking at massive deductibles, high co-pays, and a limit on what they will actually pay out.

If you have Medicare, the situation is even more strict. Original Medicare virtually never covers healthcare outside the US, except in very rare circumstances involving travel to Canada or Mexico. Some Medicare Advantage plans or Medigap policies offer a foreign travel emergency benefit, but it usually comes with a strict lifetime limit and requires you to pay a large deductible.

If you find yourself in a foreign hospital, relying on your domestic health insurance is a massive gamble. Travel medical insurnace is designed to fill that exact gap, acting as your primary health coverage while you are exploring the world.

Travel Medical Insurance vs Comprehensive Trip Insurance

It is really important to understnad the difference between travel medical coverage and comprehensive trip insurance. A lot of folks buy one thinking they have the other.

Travel Medical Insurance is focused purely on your health. It covers doctor visits, emergency room trips, hospital stays, and medical evacuations if you get hurt or sick on your trip. It usually does not cover the cost of your flights or hotels if you have to cancel the trip before you leave.

Comprehensive Travel Insurance covers the financial investment of your trip. It includes trip cancellation, trip interruption, and lost luggage. Most comprehensive plans also include travel medical coverage baked in.

If you are taking a cheap flight to stay with relatives in Europe, you might not care about trip cancellation because your financial risk is low. In that case, a standalone travel medical plicuy is incredibly cheap and does exactly what you need. But if you are dropping ten grand on a luxury African safari, you probably want a comprehensive policy that protects both your health and your financial investment.

What Does Travel Medical Insurance Actually Cover?

When you buy a travel medical policy, it generally covers the sudden, unexpected medical issues that pop up during your trip. It is not meant for routine checkups or elective procedures.

Emergency Medical Treatment

If you get hit by a scooter in Rome or come down with severe pneumonia in Tokyo, this coverage kicks in. It pays for your hospital room, the surgeon, the anesthesia, the nursing staff, and the medications they give you in the hospital. It functions very similarly to your normal health insurance, just localized to your trip.

Doctor Visits and Outpatient Care

It isn’t always a massive emergency. Sometimes you just get a nasty sinus infection or a bad case of travelers diarrhea and need to see a local clinic. Travel medical plans will cover these outpatient visits and the prescription drugs you need to get back on your feet.

Emergency Dental

Most plans include a small benefit for emergency dental care. This is strictly for the sudden relief of pain to sound, natural teeth. If you bite into a hard piece of bread in Paris and crack a tooth, this helps cover the emergency extraction or temporary crown. It won’t pay for you to get your teeth whitened or get a routine cleaning.

Emergency Medical Evacuation

This is arguably the single most important part of any travel medical policy. If you are trekking in a remote part of the Andes and suffer a severe injury, the local clinic probably isn’t equipped to handle complex surgery.

Emergency medical evacuation covers the massive cost of transporting you from that remote area to a hospital capable of giving you the care you need. Sometimes that means a helicopter ride to the capital city. If the situation is dire enough, it covers a medically staffed private jet to fly you all the way back to the United States. Without insurance, a medevac flight can easily cost anywhere from $50,000 to $250,000 out of pocket. We have seen it bankrupt families.

Repatriation of Remains

It is a morbid topic, but an essential one. If the unthinkable happens and you pass away while traveling, the cost of transporting your remains back to your home country is incredibly high and logistically complicated. This coverage handles the costs and coordinates with local authorities, sparing your famliy from having to navigate international mortuary laws during a time of grief.

How Much Coverage Do You Need?

When you look at different plans, you will see medical maximums ranging from $50,000 all the way up to $2,000,000. How do you know what to pick?

A good rule of thumb is to carry a minimum of $100,000 in medical coverage and $250,000 in medical evacuation coverage for most international trips.

However, you should adjust that based on where you are going. If you are traveling to a country with socialized medicine and relatively low healthcare costs, a $100,000 limit is likely plenty. But if you are traveling to a place where private healthcare is notoriously expensive, or if you are going somewhere extremely remote like Antarctica or deep into the Amazon basin, you want your medical evacuation limits to be as high as possible. A half million dollars in evacuation coverage is totally reasonable for an expedition trip.

The Pre-Existing Condition Limitation

This is where a lot of claims get denied, so it is vital to understand how it works.

A pre-existing condition is generally defined as any medical condition you had, were treated for, or took medication for during a specific look-back period before you bought the policy. That look-back period is usually 60 to 180 days.

If you have a heart attack on your trip, and the insurance company looks at your medical records and sees you were put on new heart medication 45 days before you bought the policy, they will likely deny the claim because it was a pre-existing condition.

The good news is that many comprehensive travel insurance plans offer a Pre-Existing Condition Waiver. If you buy your insurance policy quickly after making your first trip deposit, and you are medically fit to travel on the day you buy the policy, the company will waive the pre-existing condition exclusion. This means if that heart condition flares up on your trip, it is fully covered.

If you have any chronic health issues, getting a policy with that waiver is absolutely essential. Standalone travel medical policies rarely offer this waiver, which is why a comprehensive plan is often better for older travelers or those with medical history.

Adventure Sports and High-Risk Activities

A standard travel medical policy is designed for standard travel, walking around museums, eating at restaurants, maybe a light hike or a swim at the beach.

If you plan on doing anything that the insurance company considers high risk, you have to read the fine print. Most standard policies completely exclude injuries sustained while participating in extreme sports. This often includes:

- Scuba diving

- Skiing and snowboarding

- Mountaineering or rock climbing

- Bungee jumping

- Skydiving

- Riding motorcycles or mopeds

If you rent a scooter in Bali and wipe out, and you didn’t check your policy, you might be on the hook for the entire hospital bill.

If your trip involves adrenaline, you need to purchase an Adventure Sports Rider or find a policy specifically tailored to extreme activities. These add-ons cost a bit more, but they ensure that your medical coverage actually applies when you are out there pushing the limits.

Single Trip vs Multi-Trip Annual Plans

How often do you travel? The frequency of your trips should dictate how you buy your coverage.

Single Trip Policies are exactly what they sound like. You buy a policy for a specific trip, from the day you leave your house to the day you return. This is perfect for the person who takes one or two international vacations a year.

Annual Multi-Trip Policies are designed for frequent flyers. You pay one flat fee for the entire year, and it covers all the international trips you take during that 12 month period. The catch is that each individual trip usually has a maximum duration, like 30 or 45 days. If you are constantly hopping over to Europe for business or taking weekend trips to Mexico, an annual plan is vastly cheaper and means you don’t have to remember to buy a new policy every time you pack a bag.

How the Claims Process Works Overseas

Let’s say the worst happens and you end up in a hospital in Berlin. What do you do?

The very first thing you or a traveling companion needs to do is call the emergency assistance number provided by your insurnace company. Every legitimate travel medical provider has a global assistance hotline.

You need to open a case with them immediately. They will coordinate with the local hospital, provide translation services if necessary, and attempt to set up direct billing.

Direct Billing vs Pay Upfront In an ideal world, the insurance company will arrange a Guarantee of Payment with the foreign hospital. This means the hospital bills the insurance company directly, and you don’t have to put massive charges on your credit card.

However, you need to be prepared for the reality that many foreign hospitals, especially smaller clinics in developing nations, do not want to deal with American insurance companies. They want cash or a credit card before they treat you or let you leave.

If that happens, you will have to pay the bill out of pocket and submit a claim for reimbursement when you get home. If you have to do this, save every single piece of paper. Get itemized receipts, medical reports, diagnosis codes, and proof of payment. If the documentation isn’t complete, your reimbursement will be significantly delayed.

Common Exclusions to Watch Out For

Insurance companies aren’t in the business of paying for foolish behavior. Aside from extreme sports, there are a few standard exclusions you will find in almost every travel medical policy.

Alcohol and Drugs If you get drunk, fall off a balcony, and break your arm, the insurnace company is probably going to deny the claim. Medical emergencies caused by intoxication or illegal drug use are standard exclusions.

Mental Health and Psychological Disorders Historically, travel insurance has excluded care for mental health crises. If someone suffers a severe panic attack or psychiatric emergency abroad, it is often not covered. A few modern policies are starting to change this, but it is still a very common exclusion.

Routine Care and Pregnancy You cannot use travel medical insurance to get cheaper dental cleanings in Mexico or a routine physical in Costa Rica. It is strictly for emergencies.

Normal pregnancy is also generally excluded. If you give birth prematurely on a trip, the medical costs for the birth and the newborn are almost never covered. Some policies will cover complications of pregnancy, but standard maternity care is a hard no. If you are traveling while pregnant, you have to read the policy language very carefully.

Traveling Against Medical Advice If your doctor tells you not to travel because of a health condition, and you go anyway and get sick, the insurance company won’t pay.

Making the Right Choice for Your Trip

Buying travel medical coverage is one of those things you hope you are wasting your money on. You want to buy it, never use it, and come home healthy.

But when things go wrong abroad, the stress of navigating a foreign healthcare system in a different language is intense. Adding a massive financial burden to that stress can ruin you.

When you are comparing plans, don’t just look at the cheapest premium. Look at the medical evacuation limits, check if they offer a pre-existing condition waiver if you need it, and make sure any activities you have planned aren’t excluded. Taking a few minutes to understnad what you are buying ensures that your epic vacation doesn’t turn into a massive headache of medical debt.