Why You Need A Cyber Security Broker

The internet has completely changed the way we all do business. Whether you are running a local bakery, managing a law firm, operating a mid-sized manufacturing company, or running a small digital agency, you rely heavily on technology. You send emails, you process online payments, you store customer data, and you probably use cloud-based software to keep everything organized. That is just the reality of the modern world. But with all that incredible convenience comes a whole new set of risks. You need cyber security insurance to help get you covered when the unexpected happens.

At Uncle Sheldon Insurance, we talk to hardworking business owners every single day who think they are simply too small to be a target for hackers. They watch the news and think cyber attacks only happen to massive global corporations, banks, or big tech companies with millions of customers. That couldn’t be further from the truth. All business sizes need cyber security these days, not just big ones. In fact, small and medium-sized businesses are often targeted specifically because they might not have the massive IT budgets or complex security walls that the big guys do. To a hacker, a small business is often seen as low-hanging fruit.

We are here to help you make sense of all this. Uncle Sheldon is your local independent agency that can help you find the right Cyber Security coverage you need with a real insurance agent. We aren’t robots, and we won’t put you through an endless, frustrating automated phone tree when you need help. We are real people who care about protecting your business just like it was our own.

What Exactly Is Cyber Liability Insurance?

If you are new to exploring this type of coverage, you might be wondering what cyber insurance even is and how it actually works. Think of it as a crucial safety net for your digital assets and your bottom line. Just like your commercial property insurance covers your physical building, inventory, and equipment if there is a fire or a storm, cyber security insurance protects your business from the financial fallout of digital disasters.

A cyber policy is specifically designed to help your business recover financially from a data breach, a ransomware attack, a phishing scam, or other cyber incidents. It steps in to cover the extensive costs associated with these events, which can be absolutely devastating if you have to pay for them entirely out of your own pocket.

Understand the benefits and downsides to not being covered. The benefit of having a solid policy is knowing that you have the financial resources and expert assistance available to survive if you get hacked. The downside of not having it? One bad click on a deceptive phishing email could potentially bankrupt your business. The out-of-pocket costs of recovering lost data, paying hefty legal fees, managing PR nightmares, and notifying customers add up faster than you might think. A single breach can easily cost tens of thousands, if not hundreds of thousands, of dollars. For many small businesses, that is a fatal blow.

Understanding the Types of Cyber Security Risks

Understanding the types of cyber security risks is essential when you are trying to figure out what kind of coverage you actually need. The digital landscape is always shifting, and cybercriminals are constantly finding new, clever ways to cause trouble and extort money. You can’t protect yourself if you don’t know what you’re up against. Here are some of the most common threats that businesses of all sizes face today:

Ransomware Attacks

This is arguably one of the most frightening scenarios a business owner can face. A hacker gains unauthorized access to your computer system and completely locks you out of your own files. They encrypt your critical data—your client lists, your financial records, your operational software—and demand a ransom, usually in untraceable cryptocurrency, in exchange for the decryption key to unlock it. If you don’t pay, your data is effectively gone forever. Even worse, modern hackers often employ “double extortion,” where they not only lock your data but also threaten to publish your highly sensitive customer information online if you refuse to pay up.

Data Breaches and Exposures

A data breach happens when sensitive, protected, or confidential data is copied, transmitted, viewed, stolen, or used by an unauthorized individual. If your business stores credit card numbers, social security numbers, detailed medical records, employee tax information, or even just detailed customer contact lists, you are at significant risk. Data breaches don’t always happen through a malicious hack; sometimes they occur because a well-meaning employee accidentally emails a spreadsheet full of sensitive client data to the wrong person. Regardless of how it happens, the financial and reputational consequences are severe.

Phishing and Social Engineering

You have almost certainly seen these types of scams. It’s an email or a text message that looks incredibly convincing. It might look like it’s from your bank, a regular vendor, a software provider like Microsoft, or even your own boss, urgently asking you to click a link, update a password, or wire money. Hackers are getting incredibly good at making these look perfectly legitimate. One momentary lapse in judgment by a single employee can open the door to your entire company network. Social engineering relies on manipulating human psychology rather than breaking through technical firewalls.

Business Email Compromise (BEC)

Similar to phishing but often much more targeted and sophisticated, this is when a cybercriminal successfully hacks into a legitimate corporate email account. Once inside, they monitor communications to learn how the business operates. Then, at the perfect moment, they use that trusted email account to conduct unauthorized transfers of funds. For example, they might email the accounting department from the CEO’s account, urgently requesting a large wire transfer to a “new vendor” which is actually the hacker’s bank account. Because the email comes from a known, trusted internal source, these scams are highly effective and incredibly costly.

What Does Cyber Security Insurance Actually Cover?

Cyber insurance policies can be notoriously complex, and they aren’t all created equal. That is exactly why working with an independent agency like Uncle Sheldon is so important. We can help you break down the confusing insurance jargon and understand exactly what you are actually buying. We want you to know exactly how the policy will respond when you need it most. Generally speaking, comprehensive cyber insurance is broken down into two main categories: First-Party Coverage and Third-Party Coverage.

First-Party Coverage (Your Direct Costs)

This covers the direct financial costs your business incurs as a result of a cyber incident. It’s all about getting your business back on its feet and operating normally again. This typically includes:

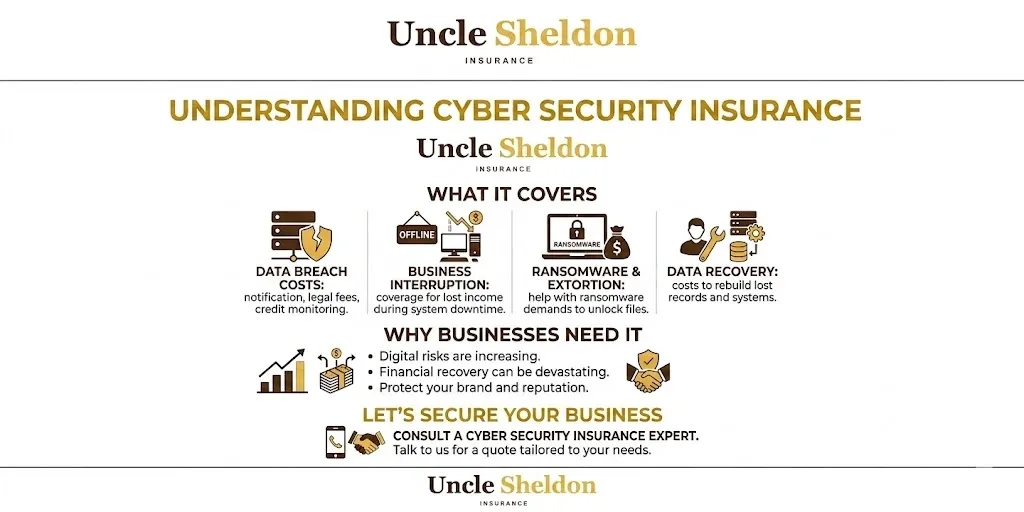

- Data and System Recovery: The high cost of hiring specialized IT forensic experts to investigate the breach, stop the attack, and painstakingly restore your compromised data and computer systems.

- Business Interruption: If your systems are down due to a hack and you simply can’t operate or generate revenue, this coverage helps replace the income you lose during that period of downtime. It can also cover extra expenses you incur to keep the business running, like renting temporary equipment.

- Ransomware and Extortion Payments: If a hacker demands a ransom and it is determined by experts that it’s the only viable way to get your critical data back, some policies will actually cover the cost of the ransom payment itself, as well as the cost of the negotiators hired to handle the situation.

- Breach Notification Costs: Every state now has a law requiring you to formally notify customers, employees, and sometimes regulators if their personal data has been compromised in a breach. This coverage handles the significant costs of drafting those notifications, mailing letters, setting up call centers, and managing the communication process.

- Public Relations and Crisis Management: A major data breach can severely damage your hard-earned reputation. This coverage pays for the cost of hiring a professional public relations firm to manage the crisis, control the narrative, and help restore trust with your valued customers.

- Credit Monitoring Services: It is standard practice to provide free credit monitoring or identity theft protection services to the customers whose sensitive data was exposed in your breach. Your policy can cover these expenses.

Third-Party Coverage (Liability to Others)

This part of the policy covers you if someone else—like a customer, a vendor, or a partner—sues you because of a cyber incident. If you failed to adequately protect their data and they suffer financial harm as a result, they might hold you legally responsible. This includes:

- Legal Defense Fees: The exorbitant cost of hiring specialized attorneys to defend your business in court against lawsuits arising from a data breach or privacy violation.

- Settlements and Judgments: If you lose the lawsuit in court or your legal team advises you to agree to a financial settlement, the cyber policy helps pay those costs so they don’t bankrupt your company.

- Regulatory Fines and Penalties: If a state or federal government agency investigates your breach and fines you for failing to comply with data protection regulations (like HIPAA in healthcare, or PCI-DSS for credit card processing), some cyber policies can help cover these costly penalties.

What Isn’t Covered by Cyber Insurance?

Just as important as knowing what is covered is having a clear understanding of what is excluded. Insurance policies have firm boundaries, and it’s our job as your transparent advisor to make sure you know exactly where those boundaries are before a claim happens. Typical exclusions on a cyber policy might include:

- Prior or Known Breaches: If your system was already hacked or compromised before you officially bought the policy, the insurance company isn’t going to cover the fallout. You can’t buy insurance for a house that is already on fire.

- Property Damage and Physical Loss: If an employee accidentally drops a crucial server and it physically breaks, or a fire destroys your computers, that is a claim for your commercial property insurance, not your cyber liability policy. Cyber covers digital assets, not physical hardware.

- Upgrading Systems (Betterment): If a forensic investigation after a hack reveals that your company’s security software is hopelessly outdated and weak, the insurance will pay the costs to help you recover from that specific hack. However, it usually will not pay for you to buy brand new, top-of-the-line software or hardware to replace the old stuff. It covers restoration to your previous state, not betterment or system upgrades.

- Intellectual Property Theft: If a sophisticated hacker steals your highly guarded secret recipe, your proprietary manufacturing algorithm, or your unreleased product designs, placing a definitive financial value on that loss is incredibly difficult. Because of this difficulty, standard cyber policies often exclude the loss of intellectual property.

- Intentional Dishonest Acts: If you or a top executive intentionally cause a breach or commit fraud, the policy will not protect you.

Busting Common Small Business Cyber Myths

We hear a lot of misconceptions from business owners who are hesitant to look into cyber coverage. Let’s clear up a few of the most common myths we hear at the agency.

Myth 1: “My general liability policy already covers this.” This is a dangerous assumption. Most standard Commercial General Liability (CGL) policies specifically exclude cyber risks and data breaches. They are designed for physical injuries and property damage (like someone slipping in your store), not digital data loss.

Myth 2: “We outsource our IT, so it’s their problem if we get hacked.” Even if you hire a fantastic third-party IT company to manage your network or a reputable cloud provider to host your data, the liability still ultimately rests with you. It is your business and your customers’ data. If there is a breach, your customers are going to look to you for answers, and regulators will hold you responsible. You need your own coverage.

Myth 3: “We don’t collect credit cards, so we don’t have any data worth stealing.” Hackers aren’t just looking for credit cards anymore. They want employee W-2s, social security numbers, driver’s license numbers, personal email addresses, medical information, and simple contact lists. Any personally identifiable information (PII) has value on the dark web. Furthermore, ransomware doesn’t care what kind of data you have; it just wants to lock you out of it so you can’t run your business until you pay up.

How to Prepare Your Business for a Cyber Policy

Getting a cyber insurance policy isn’t quite as simple as just signing a piece of paper. Insurance carriers want to know that they are insuring a business that takes its security seriously. When we help you apply for coverage, the carriers will ask some detailed questions. By implementing a few basic security protocols now, you not only make your business safer, but you also make yourself a much more attractive candidate for insurance, which often leads to better premium rates.

Here are a few things carriers like to see:

- Multi-Factor Authentication (MFA): This is becoming a non-negotiable requirement for many insurance carriers. MFA means requiring a second form of verification (like a code sent to a phone) in addition to a password when logging into company systems, email, or VPNs.

- Regular Data Backups: You should be backing up your critical data frequently, and crucially, those backups should be stored offline or completely segmented from your main network. If ransomware locks your main network, it will lock your connected backups too unless they are segmented.

- Employee Training: Human error is the leading cause of cyber incidents. Carriers want to see that you are regularly training your employees on how to spot phishing emails and avoid basic security blunders.

- Endpoint Protection: Having robust, up-to-date antivirus and anti-malware software installed on all company computers and devices.

- A Basic Incident Response Plan: Just knowing who to call and what immediate steps to take if you suspect a breach can dramatically limit the damage.

The True Cost of Cyber Security Insurance

This is usually the very first question we hear, and the honest answer is that it depends entirely on your specific business. Because we are an independent agency that works with multiple carriers to find clients the right fit, we see a very wide range of pricing. The cost of your premium is going to be based on several different risk factors.

- Your Industry: Some industries are just inherently bigger targets. Healthcare facilities, financial advisory firms, and large retail businesses handle massive amounts of highly sensitive data, so their premiums are generally higher than a local landscaping company or a small consulting firm.

- The Volume of Sensitive Data You Store: The more data you have, the bigger the overall risk. If you have a database with 100,000 sensitive client records, your policy is going to cost more than a business with only 500 records.

- Your Current Security Posture: As mentioned above, insurance companies reward good behavior. Businesses with strong security measures, like strict MFA enforcement and rigorous employee training, often get significantly better rates than businesses with lax security.

- Your Past Claims History: If your business has already suffered multiple data breaches in the last few years, insurance carriers are going to naturally view you as a much higher risk, which means higher premiums or stricter policy terms.

- The Coverage Limits You Choose: Naturally, a policy with a massive $5 million limit is going to cost more than a policy with a $500,000 limit. We can help you look at your overall risk profile, estimate potential costs of a breach in your specific industry, and decide what limit makes the most sense for your budget and your appetite for risk.

Why Choose Uncle Sheldon for Your Cyber Coverage?

Buying cyber insurance shouldn’t feel like you are just picking a random product off a shelf online or dealing with an emotionless chatbot. It requires a real conversation. It requires truly understanding your specific vulnerabilities, your business model, and your budget.

Find and compare the best rates in cyber security insurance with your Uncle in insurance, Uncle Sheldon. We aren’t tied to just one big insurance company. We are a proud, independent brokerage. That means we have the freedom to take your application and shop it around to multiple top-tier, highly-rated insurance carriers. We do the shopping around and the tedious comparison work to find the policy that offers the most robust coverage for the most competitive price.

More importantly, we believe in straight answers. We use technology to make the quoting and application process easier and more efficient, not to replace the essential human element of our business. We won’t ever try to aggressively upsell you or push you into buying coverage you truly don’t need. But we will strongly advise you to protect yourself where you are genuinely vulnerable.

We want you to feel confident that if the absolute worst happens and your business falls victim to a cyber attack, you have a dedicated team of real humans ready to step in, answer the phone, and help you clean up the mess. You won’t be navigating the crisis alone.

Once that red screen shows up on your computer telling you your files are locked, it is too late to buy the insurance. Be proactive about protecting the business you have worked so hard to build. Let’s sit down, review your digital risks, and find a cyber security policy that lets you focus on growing your business while sleeping a little easier at night. Give us a call or schedule a review today, and let’s make sure you’re covered.