This Is Not the Coverage Most People Think They Have

One of the most common surprises we see when businesses come to us to review their insurance is that their general liability policy excludes liquor-related claims. It’s right there in the policy language, usually buried in a section most people never read — the liquor liability exclusion. If your business is in the business of selling, serving, or furnishing alcohol, standard commercial general liability won’t cover you when a claim arises from that activity.

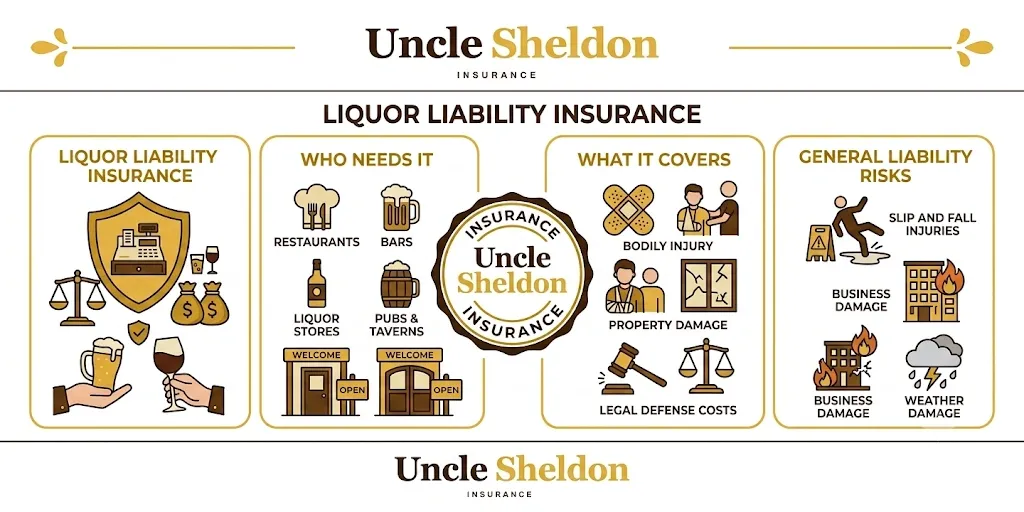

That’s where liquor liability insurance comes in. It’s a separate line of coverage specifically designed for the risks that come with alcohol. Whether you run a bar, a restaurant, a liquor store, a brewery, a catering company, or an event venue, if alcohol is part of what you do — even occasionally — this coverage deserves a close look.

And even if you think alcohol is a small part of your business, the law in your state might have a different view of your exposure.

Dram Shop Laws — The Legal Foundation

Liquor liability insurance exists largely because of something called dram shop laws, and these laws are what make the exposure very real for businesses.

Dram shop laws (the term comes from the old practice of selling spirits by the “dram”) hold businesses legally responsible for serving alcohol to someone who then causes harm to a third party. In most states, if a bar serves an already visibly intoxicated customer and that customer later causes a car accident, the bar can be sued alongside the drunk driver. The business that served the alcohol shares liability for the damage caused.

The scope and severity of these laws varies quite a bit by state. Some states have relatively broad dram shop liability. Others have caps on damages or more limited applicability. A handful of states have minimal or no dram shop statute at all, though common law negligence claims can still apply even without a specific statute.

What this means practically is that the legal exposure for alcohol-serving businesses is not just theoretical. These cases happen, they result in real judgments, and the amounts involved can be significant — especially when there’s serious injury or death involved.

| State Category | General Approach |

|---|---|

| Broad dram shop liability | Business can be held liable for third-party harm caused by intoxicated patrons; minimal caps on damages |

| Moderate dram shop liability | Liability exists but with some limitations on when or how it applies |

| Limited or no statute | No specific dram shop law, but negligence claims can still arise under common law |

It is worth talking to an agent familiar with your state’s rules, because the specific laws where you operate directly affect your exposure and what coverage you actually need.

Who Actually Needs This Coverage

The obvious businesses are bars, taverns, nightclubs, and restaurants with full liquor service. But the list goes beyond those.

Liquor stores and off-premise retailers — If you sell alcohol to be consumed elsewhere, you have exposure. In many states, off-premise retailers can also face dram shop liability if they sold to a visibly intoxicated person or a minor.

Breweries, wineries, and distilleries — Especially if you have a taproom or tasting room where alcohol is served on-site.

Caterers — If you provide alcohol service at events as part of your catering operation, you can be held liable for what happens after guests leave.

Event venues — Venues that allow outside caterers or that provide bar service themselves have real exposure whenever alcohol is flowing on their property.

Hotels and hospitality — Properties with bars, restaurants, or room service liquor have the same exposure as any other food and beverage operation.

Country clubs and private clubs — The private nature of the facility doesn’t eliminate the liability.

Convenience stores and grocery stores — Any retail location with a beer and wine license needs to think about this.

Special events with alcohol — This one catches people off guard more than any other. If you’re hosting a company event, a festival, a fundraiser, or any gathering where alcohol will be available — even if it’s just beer at a company picnic — there is some level of liquor liability exposure that your standard general liability policy likely won’t address.

The bottom line is that if alcohol is present and your business has any role in providing, serving, or permitting it, you should at least have a conversation about your exposure.

What Liquor Liability Insurance Covers

The core purpose of liquor liability insurance is to cover claims arising from the service or sale of alcohol when an intoxicated person causes harm to someone else.

Third-party bodily injury — The most common and serious claim type. If a patron leaves your establishment intoxicated and causes an accident that injures another driver, pedestrian, or anyone else, your liquor liability policy is what responds to the claims from those injured third parties.

Third-party property damage — Same concept applied to property. If an intoxicated patron damages someone’s vehicle in your parking lot, or causes damage to a neighbor’s property after leaving your bar, property damage liability coverage applies.

Legal defense costs — This one matters more than people sometimes realize. Defending a lawsuit costs real money regardless of the outcome. A liquor liability policy covers the cost of your legal defense even if the claim against you is ultimately without merit. Legal fees in these cases can run into the tens of thousands of dollars before a case ever reaches a verdict.

Settlements and judgments — If a claim is resolved by settlement or results in a judgment against your business, your policy pays those damages up to your policy limit.

Assault and battery — Many liquor liability policies can be extended to cover claims arising from assault and battery. This is relevant for bars and nightclubs where altercations do sometimes happen. Not all policies include this automatically, so it’s worth asking about specifically.

What It Does Not Cover

Understanding the exclusions helps you see where other coverage is needed.

Your own property — Liquor liability is third-party coverage. If an intoxicated customer damages your bar, your tables, your equipment, that comes under your commercial property coverage, not liquor liability.

Employee injuries — Workers compensation handles on-the-job injuries to your employees, not liquor liability.

Your own intoxication — If you’re the one who caused harm while intoxicated, don’t look to this policy for help.

Underage drinking you knew about — Knowingly serving a minor is generally excluded from coverage. Most policies won’t respond to claims where the business deliberately or knowingly served someone under legal drinking age. This is also why training programs matter so much — both for risk management and for maintaining your coverage.

Intentional acts — Like most liability policies, intentional harm is excluded.

First-party claims — If a patron injures themselves rather than a third party, that’s not typically a liquor liability claim. (That said, your general premises liability coverage may respond depending on the circumstances.)

Social Host Liability — A Separate but Related Topic

A lot of people ask whether they need liquor liability if they’re not a business, just someone hosting a party. This falls under something called social host liability, and it’s worth addressing.

Many states also have laws that hold private individuals responsible for harm caused by guests they provided alcohol to. If you host a party, a guest becomes visibly intoxicated, you continue letting them drink, they get in their car, and cause an accident — depending on your state, you may have legal exposure.

Social host coverage is sometimes available as an endorsement to a homeowner’s or renter’s policy, or through a one-time special event policy. It’s not the same as commercial liquor liability, but if you’re hosting large events at home where alcohol will be served, it’s worth knowing your exposure.

For businesses hosting one-time events — a holiday party for employees at a rented venue, a product launch with open bar — short-term event liquor liability policies are available. These cover a single event rather than requiring an annual commercial policy.

How Much Coverage Is Enough

There’s no universal right answer here, but there are some guidelines that help frame the question.

Serious liquor liability claims — cases involving DUI accidents with injuries or fatalities — can result in multi-million dollar verdicts. The exposure in these cases can be very large. Minimum policy limits may satisfy a legal requirement or a landlord’s lease clause, but they might not provide real protection in a worst-case scenario.

For most small bars, restaurants, and liquor retailers, a $1 million per occurrence limit with a $2 million aggregate is a common starting point. For businesses with higher volume, later hours, or a history of incidents, higher limits are worth considering. A commercial umbrella policy can also sit on top of your liquor liability to extend your overall coverage further.

Contracts matter here too. If you’re a venue, caterer, or retailer who works under contracts with clients or landlords, those contracts often specify minimum liquor liability limits. Know what those requirements are before you buy.

Premiums — What Drives the Cost

Liquor liability premiums vary a lot depending on the nature of your operation. Underwriters look at several factors to understand your exposure.

Type of establishment — A quiet neighborhood wine bar has very different risk characteristics than a late-night nightclub. The type of business is one of the biggest drivers of premium.

Percentage of revenue from alcohol — For restaurants especially, underwriters want to know what percentage of your revenue comes from alcohol sales versus food. Higher alcohol revenue percentage means more exposure.

Hours of operation — Businesses that operate late into the night, especially those with after-midnight hours, are viewed as higher risk. More late-night alcohol service generally means higher rates.

Annual sales volume — More revenue usually means more coverage and higher premium.

Number of seats or capacity — More patrons means more potential exposure.

Prior claims history — A clean loss history helps. Prior liquor-related claims push premiums up significantly and can affect your ability to find coverage at all in standard markets.

Location — Venues in states with broader dram shop liability generally pay higher premiums. Density of nearby competition and the character of the surrounding area can also factor in.

Staff training programs — Some carriers give credit for certified alcohol service training programs. TIPS (Training for Intervention ProcedureS) and ServSafe Alcohol are the most common. Having trained staff who know how to recognize intoxication and how to refuse service can reduce your exposure and sometimes your premium.

| Business Type | Typical Annual Premium Range |

|---|---|

| Small restaurant with beer and wine only | $500 – $1,500 |

| Full-service restaurant with liquor | $1,000 – $3,000+ |

| Bar or tavern | $2,500 – $7,000+ |

| Nightclub or high-volume bar | $5,000 – $20,000+ |

| Liquor store | $800 – $2,500 |

| Catering company | $1,000 – $4,000+ |

| Brewery or winery with taproom | $1,500 – $5,000+ |

These are ballpark ranges only — your actual quote depends entirely on the specifics of your operation, your state, and your claims history.

The Server Training Angle

This is worth spending a moment on because it genuinely matters for both risk management and your insurance situation.

Server training programs teach staff how to identify signs of intoxication, how to slow service before a customer reaches impairment, and how to safely refuse service when necessary. It’s also good practice to train staff on how to handle a situation when an intoxicated patron insists on driving — knowing how to call a cab or rideshare for a customer, or even how to contact family, can prevent a serious incident.

Beyond the safety and liability benefits, some carriers specifically ask about training programs as part of their underwriting process. A business with trained staff and written policies around alcohol service can present a better risk profile than one without those things in place.

If you haven’t looked into TIPS certification or something similar, it’s worth doing regardless of insurance. But it can also help you with your coverage situation.

Certificates of Insurance and Lease Requirements

If you’re operating a bar or restaurant in a leased space, your landlord almost certainly requires liquor liability coverage and will want to see a certificate of insurance showing you have it. Same goes for caterers working events at venues — the venue often requires the caterer to carry liquor liability and name the venue as an additional insured.

This is normal and manageable, but you need to know the requirements before you’re asked for a certificate you don’t have. If you’re negotiating a lease or a catering contract, it’s worth reviewing the insurance requirements in the agreement before you sign so there are no surprises.

Off-Premise Liquor Liability

One situation that sometimes gets overlooked is off-premise service. If you cater an event at a client’s location, host a pop-up, or serve alcohol in any context other than your normal business premises, check whether your policy covers that activity.

Some policies are limited to the described premises on the declarations page. Others have broader language that follows the business wherever it operates. This distinction matters if you’re a restaurant doing off-site catering, a brewery doing events at outside venues, or any business with alcohol service that happens in multiple locations.

Getting the Right Policy

Shopping for liquor liability isn’t quite like shopping for standard commercial general liability. Not all carriers write this coverage, and the ones that do have different appetites depending on the type of business and risk profile.

For higher-risk operations — nightclubs, late-night bars, businesses with prior claims — you may need to look in specialty markets or with surplus lines carriers rather than standard admitted markets. These policies can be more expensive and may have different terms, but they exist for a reason. The coverage is out there.

Working with an independent agent who understands this line of coverage is genuinely useful here. An agent who places this type of business regularly knows which carriers are competitive for different types of establishments and what underwriters are going to ask. That background knowledge saves time and usually gets you to a better result than going directly to a general carrier who may not specialize in hospitality risks.

Talk to an Agent Who Knows Liquor Liability

We work with bars, restaurants, liquor stores, caterers, event venues, and all kinds of businesses that have alcohol as part of what they do. We understand the coverage, we know which carriers are a good fit for different types of operations, and we’re going to give you an honest picture of your exposure rather than just putting a policy in front of you and calling it done.

If you’re not sure whether your current coverage actually includes liquor liability — or if you’re just getting started and trying to figure out what you need — reach out. We’ll take a look at your situation and tell you exactly where you stand. No runaround, no algorithm, just a real agent who knows this stuff and wants to help you get it right.