Your Agent for Airbnb and Short Term Rental Insurance

Turning a property into a short term rental can be an incredibly rewarding investment. Whether you are renting out your basement, listing a cozy cabin in the mountains, or managing a whole portfolio of vacation homes on platforms like Airbnb or VRBO, it’s a fantastic way to generate income.

But here is what a lot of hosts discover the hard way. The moment you hand over the keys to a paying guest, your risk profile completely changes. You are no longer just a homeowner; you are running a hospitality business. And running a business means you need the right kind of protection.

At Uncle Sheldon Insurance, we talk to hosts all the time who are unknowingly operating with massive gaps in their coverage. They assume their standard homeowners policy or the platform’s built-in protections have them fully covered. Unfortunately, that is rarely the case. Let’s break down everything you actually need to know about Airbnb and short term rental insurance, without all the confusing jargon.

The Big Myth About Homeowners Insurance

Let’s start by tackling the most common misunderstanding we see. Many hosts simply assume that their existing homeowners policy will protect them if a guest damages the property or gets hurt.

In almost all cases, this is completely false.

Standard homeowners insurance is designed for owner-occupied properties. The moment you start charging money for people to stay there on a regular, short-term basis, insurance companies view it as a commercial enterprise. If a guest accidentally burns down your kitchen and you try to file a claim on your personal homeowners policy, the insurance carrier will likely deny the claim the second they find out it was a short term rental. They might even cancel your entire policy for misrepresenting how the property is being used.

Some homeowners policies might allow for very rare, occasional rentals (like renting out your house for one weekend a year during a major local event), but if you are actively listing it online and hosting guests regularly, you absolutely need a specialized policy.

What About Landlord Insurance?

Okay, so if a homeowners policy won’t work, what about landlord insurance?

Landlord policies (often called dwelling fire policies) are designed for long-term rentals. Think of a property where a tenant signs a 12-month lease. These policies cover the physical structure and provide liability protection if someone gets hurt on the property.

However, landlord policies usually exclude coverage for properties rented on a short-term basis. The risk is just fundamentally different. Long-term tenants treat the property like their own home. Short-term guests are on vacation, passing through, and statistically much more likely to cause accidental damage or get injured because they aren’t familiar with the property. Plus, short term rentals are often fully furnished, and landlord policies generally don’t cover personal property to the extent a fully furnished vacation rental requires.

How Short Term Rental Insurance is Different

This is where true short term rental (STR) insurance comes in. This is a specialized hybrid policy designed specifically for the unique risks of platforms like Airbnb, VRBO, and direct booking sites. It essentially combines the elements you need from a commercial policy, a landlord policy, and a homeowners policy into one neat package.

To help visualize the differences, here is a quick breakdown of how these policies compare:

| Feature | Homeowners Policy | Landlord Policy | Short Term Rental Policy |

|---|---|---|---|

| Primary Purpose | Owner-occupied home | Long-term leases (6+ months) | Regular short-term guests |

| Liability for Paying Guests | Usually Excluded | Covered | Fully Covered |

| Guest-Caused Property Damage | Usually Excluded | Limited | Fully Covered |

| Loss of Rental Income | Not Covered | Covered (long-term only) | Covered (short-term income) |

| Extensive Furnishings Coverage | Covered | Limited or Excluded | Fully Covered |

| Commercial Use Permitted | No | Yes (Residential only) | Yes (Hospitality) |

As you can see, a dedicated STR policy is the only one truly designed to handle the reality of running an Airbnb.

Does AirCover Provide Enough Protection?

This is the second biggest myth we hear. Airbnb offers a program called AirCover for Hosts, and VRBO has its own liability protection program. These programs are heavily marketed to make hosts feel safe and secure.

Don’t get us wrong, these platform protections are a great perk, and they do pay out for many minor incidents. But you should never treat them as a replacement for your own independent insurance policy. Here is why:

1. It’s Not Actual Insurance

Programs like AirCover are technically “host protection programs” or “guarantees,” not formal insurance policies. They are controlled entirely by the platform. If Airbnb decides your claim doesn’t meet their specific criteria, they can deny it, and you have very little recourse. You don’t have a state insurance commissioner to appeal to if things go wrong.

2. Gaps in Coverage

AirCover only applies while an actual Airbnb guest is staying at the property. What if a pipe bursts while the property is sitting empty between bookings? What if a tree falls on the roof during a massive storm? What if you are staying there yourself for a weekend and accidentally start a fire? AirCover won’t cover any of those scenarios because they aren’t related to a guest stay.

3. Direct Bookings Aren’t Covered

If you ever decide to take a direct booking outside of the platform—maybe renting to a friend of a friend, or setting up your own website to save on fees—you are completely unprotected.

4. Loss of Income Limits

If a guest causes a major fire and your property is unrentable for six months while it’s being rebuilt, AirCover might cover the physical damage, but their coverage for your lost business income is often limited or capped. A robust independent policy can provide much stronger protection for your lost revenue.

Think of AirCover as a nice secondary backup layer, but your own STR insurance should be your primary shield.

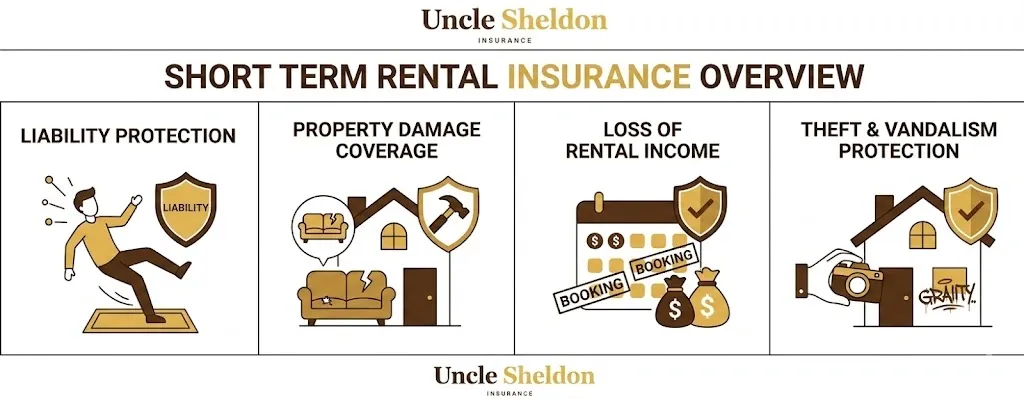

What Does an Airbnb Insurance Policy Actually Cover?

When you work with an independent agency to get a proper short term rental policy, you are buying a comprehensive package. While policies differ between carriers, here are the core components you can expect to be covered.

Building and Property Coverage

This is the foundation. It covers the physical structure of your rental property—the roof, walls, floors, plumbing, and electrical systems. If there is a fire, a windstorm, or severe vandalism, this part of the policy pays to repair or completely rebuild the structure.

Contents and Personal Property

This is huge for vacation rentals because they are usually fully furnished. This covers everything inside the house that isn’t nailed down: your expensive couches, big screen TVs, the high-end mattress, the fully stocked kitchen, and even the linens. If a guest completely trashes the living room or steals your brand new appliances, this coverage kicks in.

Liability Protection

This might be the most critical piece of the puzzle. Liability covers you if a guest (or someone they invited over) gets injured on your property and decides to sue you.

If a guest slips on an icy walkway you forgot to salt, falls down a poorly lit staircase, or gets hurt in the hot tub, the medical bills and legal fees can easily reach hundreds of thousands of dollars. Liability coverage pays for your legal defense team and covers any settlements or judgments against you up to your policy limit.

Loss of Business Income

This is what separates a true business policy from a personal one. If a covered peril (like a major kitchen fire or a massive plumbing leak) makes your property uninhabitable, you have to cancel all your upcoming reservations. You aren’t just dealing with repair costs; you are bleeding money every day it sits empty.

Loss of income coverage reimburses you for the money you would have made from those cancelled bookings while the property is being repaired. It keeps your business afloat during a crisis.

Additional Specialized Coverages

Depending on the carrier and your specific property, you might also have or need endorsements for things like:

- Liquor Liability: If you provide complimentary wine or beer to your guests.

- Pet Damage: If you run a pet-friendly rental.

- Amenities: Specific coverage for things like swimming pools, hot tubs, bicycles, or kayaks that you let guests use.

- Bed Bug Extermination: A growing concern for hosts, some policies help cover the extensive costs of removing an infestation and the lost income during the process.

Who Actually Needs This Type of Coverage?

The short answer is: anyone who is collecting money for short-term stays. But it really applies to several different scenarios:

The Dedicated Investor: You own a property (or several) solely for the purpose of running them as vacation rentals. This is a full-time business endeavor, and a commercial STR policy is absolutely mandatory to protect your investment portfolio.

The Snowbird or Part-Timer: You have a secondary vacation home that you use for a few months a year, but you rent it out on VRBO for the rest of the year to help cover the mortgage and taxes.

The House Hacker: You own a duplex, live in one half, and Airbnb the other half. Or maybe you just rent out the finished basement or a spare bedroom in your primary residence. Even though you live there, the portion being rented out creates commercial risk that your standard homeowners policy probably won’t touch.

How Much Does Airbnb Insurance Cost?

This is always the first question we hear, and it’s a perfectly fair one. Because we are an independent brokerage, we work with multiple carriers and see a wide range of pricing.

The honest truth is that a true short term rental policy is generally going to be more expensive than a standard homeowners or long-term landlord policy. Why? Because the risk is simply much higher. You have a constantly rotating door of strangers living in your property, which naturally leads to more accidents, more wear and tear, and more liability exposure.

While it’s impossible to give an exact number without running a quote, there are several key factors that influence the premium you will pay:

Location, Location, Location: Just like real estate, insurance is local. A beachfront condo in a hurricane zone is going to cost significantly more to insure than a quiet cabin in the Midwest. Areas prone to wildfires, floods, or heavy snowstorms have naturally higher premiums. Property Value and Replacement Cost: A massive 6-bedroom luxury estate costs more to rebuild and furnish than a 1-bedroom city apartment, so the coverage limits and premiums will be higher. Amenities: Having a swimming pool, a hot tub, a trampoline, or providing things like golf carts or kayaks drastically increases your liability risk, which will bump up the cost of the policy. Deductible: This is the amount you pay out of pocket before the insurance kicks in. Choosing a higher deductible (say, $2,500 instead of $1,000) will usually lower your annual premium. Occupancy Rate: Some carriers look at how often the property is actually rented out versus sitting vacant or being used by the owner.

Expect a true STR policy to cost noticeably more than a standard homeowners policy on the exact same property. How much more depends on everything above, which is why we always run actual quotes instead of guessing. But when you factor in the massive financial risks of operating underinsured, it’s a necessary cost of doing business.

Steps to Getting the Right Policy

The insurance side of hosting can feel overwhelming, especially when you are busy managing bookings, cleaning schedules, and guest communications. That is exactly why Uncle Sheldon is here to help. Here is the general process for getting your rental properly insured:

1. Be Completely Honest About Your Operations The worst thing you can do is hide the fact that you are running an Airbnb from your current insurance company. If you have a claim and they discover the commercial use, they will deny it. Be upfront with your agent about exactly how the property is used, how many days a year it’s rented, and what amenities you offer.

2. Evaluate Your Current Setup Are you currently relying entirely on AirCover? Are you just crossing your fingers that your homeowners policy won’t notice? Take an honest look at where your vulnerabilities are.

3. Determine Your Replacement Costs Take the time to do a thorough inventory of everything inside the rental. If you had to replace every bed, couch, television, fork, and towel tomorrow, how much would it cost? You need to make sure your contents limit is high enough to cover a total loss.

4. Work With an Independent Agent Don’t just go online and click the first thing you see. Short term rental insurance is a highly specialized niche. Working with a local, independent agency means you have an expert in your corner. We can take your specific property details and shop them around to the carriers who actually specialize in STRs, comparing coverages and rates to find the perfect fit. We do the legwork for you.

Busting More Common Myths

We’ve covered the homeowners policy myth and the AirCover myth, but there are a few other dangerous misconceptions floating around host forums and Facebook groups. Let’s clear those up.

”I require a security deposit, so I don’t need extensive coverage.”

Security deposits are great for minor things—a broken lamp, a stained rug, or a lost key. But what happens if a guest throws a massive unauthorized party and causes $30,000 in damage to your hardwood floors and drywall? A $500 security deposit isn’t going to make a dent in that. You need the deep pockets of an insurance policy for the big disasters.

”I only rent to people with great reviews, so my risk is low.”

Even the nicest, most highly-rated guests can have accidents. They can accidentally leave a stove burner on, slip in the shower and break a leg, or flush something they shouldn’t down the toilet and flood the bathroom. Accidents don’t care about a 5-star rating profile. Liability is liability, regardless of how nice the person is.

”My LLC protects my personal assets, so I don’t need high liability limits.”

Setting up an LLC for your rental business is a very smart legal move, and we always recommend consulting a lawyer about it. However, an LLC is not a magical force field. If you are sued for a major injury and your business doesn’t have adequate insurance to cover the judgment, plaintiff attorneys can try to “pierce the corporate veil” and go after your personal assets anyway. A robust insurance policy with high liability limits is your first and most vital line of defense, whether you have an LLC or not.

What to Do If You Have a Claim

If the worst happens and your property is damaged or a guest is injured, how you handle the immediate aftermath is critical.

First, prioritize safety. If there is a fire, a break-in, or a serious medical emergency, call 911 immediately. Don’t worry about the property until the humans are safe.

Once the immediate danger has passed, document absolutely everything. Take dozens of photos and videos of the damage from every angle before you clean anything up. Do not throw anything away until the insurance adjuster has seen it or given you permission.

If the damage was caused by a guest, communicate through the platform’s messaging app so there is a written record. If it’s a major issue, ask for a police report.

Then, call your insurance agent immediately. Don’t wait. The sooner we know about the situation, the sooner we can help you navigate the claims process, get an adjuster assigned, and get the ball rolling on repairs and loss of income reimbursements. It’s an incredibly stressful time, but having a real human to talk to makes a world of difference compared to filing a claim through an online portal.

The Bottom Line for Hosts

Running a successful short term rental business takes a massive amount of hard work, dedication, and investment. You spend hours agonizing over the decor, responding to guest inquiries at all hours of the night, and coordinating cleaners to make sure every stay is perfect.

Don’t let one bad guest, one freak accident, or one nasty storm wipe out all of that hard work.

Trying to save a few bucks by relying on a standard homeowners policy or crossing your fingers with platform guarantees is simply a gamble you cannot afford to take. Knowing you have a comprehensive, specialized policy designed exactly for what you do is worth every penny.

Uncle Sheldon was started with the simple idea to help our community with insurance, whether it be for personal or commercial needs. We are here to help you find the right fit. Our team is upfront with all of our clients. If you have questions about your current setup, or if you are just starting out and want to make sure you do it right from day one, reach out to us. We will review your situation, explain your options clearly, and help you secure the coverage you need to keep your rental business thriving for years to come.