Mobile Homes in Colorado Have Their Own Risk Profile

Colorado has a lot of manufactured and mobile homes spread across the state — in mountain communities, on the Eastern Plains, in the suburbs of the Front Range cities, and in rural areas where land is available and housing costs have driven people toward more affordable options. There’s nothing wrong with that. But what matters from an insurance standpoint is that those homes face a set of risks that are pretty specific to Colorado, and the coverage needs to reflect that.

The main difference between insuring a manufactured home in Colorado versus, say, Florida or Texas isn’t the policy structure — it’s the hazards. Colorado’s combination of hail frequency, wildfire exposure, high-wind events, and in some mountain areas, real snowload concerns, creates a coverage picture that has some unique angles.

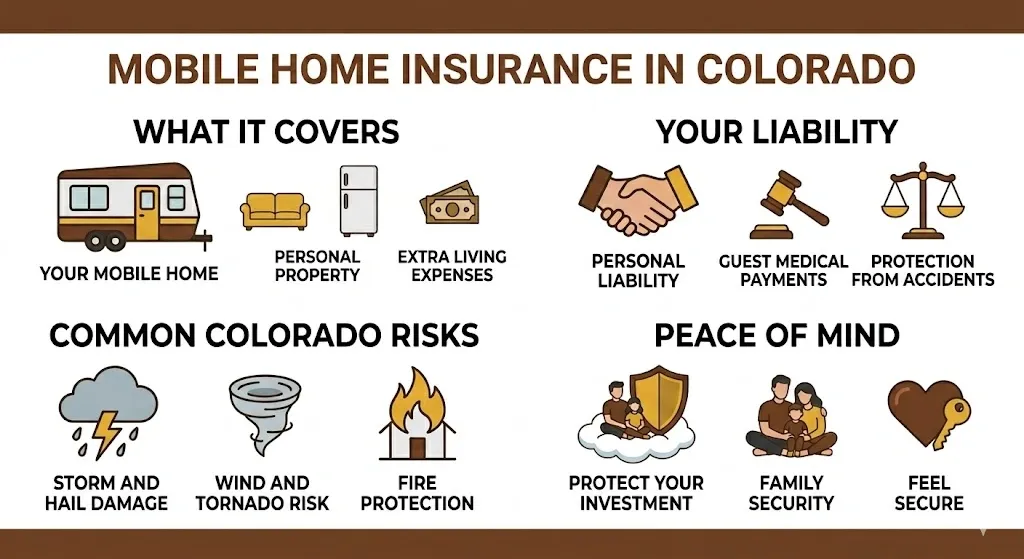

The main topic page on mobile home insurance covers the basics of how these policies work — dwelling coverage, contents, liability, additional living expenses, the difference between actual cash value and replacement cost, the 1976 HUD standard cutoff that affects what carriers will write. All of that still applies and is worth reading if you haven’t already. What this page covers is what mobile home insurance looks like specifically in Colorado, broken down by the areas of the state where people are actually living in manufactured homes.

What Makes Colorado Different for Mobile Home Coverage

A few things stand out about insuring manufactured homes in this state.

Hail is a serious issue here. The Front Range of Colorado — the corridor running from Fort Collins down through Denver and Colorado Springs — has some of the highest hail frequency in the entire country. Hailstorms in Colorado can produce hail that damages roofs, siding, and everything else exposed. Mobile and manufactured homes are often more susceptible to hail damage than traditionally built homes because of differences in roofing materials and siding types commonly used in manufactured construction. Making sure your policy has solid comprehensive coverage that handles hail properly, and that the claim settlement is on replacement cost terms rather than actual cash value, is genuinely important on the Front Range.

Wildfire exposure is real and it’s growing. Colorado has had devastating wildfire seasons. The Marshall Fire in December 2021 was eye-opening because it burned through suburban areas in Boulder County that nobody thought of as wildfire territory. The state has burned across Front Range foothills, mountain communities, canyon areas, and rural grasslands. Manufactured homes in the wildland-urban interface — the places where development meets open land — face the same wildfire risk as any other structure, and in some cases manufactured homes are more vulnerable because of their construction and the way they’re often sited on lots. Getting real coverage in place for fire loss, including loss of use coverage that handles the displacement period, is not optional in Colorado.

Wind matters differently in different parts of the state. On the Eastern Plains, high winds are a constant. The chinook winds that come off the Rockies and accelerate across the plains can be genuinely destructive. Manufactured homes that aren’t anchored properly or that are older and less structurally robust can sustain wind damage in those events. Making sure your policy actually covers wind damage and that the claim limits are adequate to handle a meaningful event is important in those areas.

Mountain communities have their own considerations. Mobile homes in mountain towns face snowload, temperature extremes, and compressed building seasons that affect how quickly repairs can happen after a covered loss. If your home is damaged in November at 8,000 feet, the repair timeline is different than the same loss in suburban Denver. Additional living expenses coverage that actually lasts long enough to cover a protracted displacement matters in mountain settings.

Denver

Denver’s manufactured home communities are spread across the metro and some of them are in neighborhoods that have been there for decades. Within the city and in suburbs like Lakewood, Arvada, Commerce City, and parts of Aurora, there are mobile home parks and communities where residents are paying lot rent and owning their homes.

Hail is the number one weather risk for Denver-area manufactured homes. The Front Range hailstorms that blow through from spring through early fall are severe enough that they’ve become a reliable annual event. If your policy is on actual cash value terms and has depreciation factored in, a hail event on a manufactured home that’s fifteen years old might pay out a fraction of what it costs to repair or replace the damaged components. Replacement cost coverage makes a real difference when you’re dealing with a hail claim.

Theft is also relevant in urban Denver. High-value items like HVAC equipment, appliances, and electronics stored in or attached to the home are targets in some parts of the metro. Comprehensive personal property coverage matters.

Manufactured home communities in Denver proper have been facing land pressure as the city has grown. Some residents are in communities where the land ownership situation has changed or where the long-term future of the park is uncertain. That doesn’t affect your insurance directly, but it’s worth knowing that your policy covers the structure and your belongings — the land underneath is separate.

Denver

- Main risks: Hail, urban theft, wildfire smoke events

- Coverage focus: Replacement cost dwelling and contents, comprehensive for hail

- Community context: Established manufactured home communities across the metro facing land value pressure

- Season: Year-round occupancy, hail season spring through fall

Colorado Springs

Colorado Springs has manufactured home communities spread through the city and in communities like Fountain, Security-Widefield, and Manitou Springs. The area south and east of the Springs is among the most affordable manufactured housing markets on the Front Range.

Wildfire risk is a real consideration in the Colorado Springs area. The Waldo Canyon Fire in 2012 and the Black Forest Fire in 2013 both caused significant residential losses in the Springs area, including in communities adjacent to the urban core. The western and northern edges of the city are in terrain where wildfire risk is genuine. If your manufactured home is in those areas, making sure fire coverage is solid — and that you have adequate loss of use coverage for a displacement scenario — is important.

Hail is the other significant risk. Colorado Springs sits right in the heart of the Front Range hail corridor and the storms that come through in spring and summer are the same ones that hit Denver. Manufactured home roofing and siding materials take hail damage the same way as any other structure.

Colorado Springs

- Main risks: Wildfire (western and northern edges), hail, wind in open areas

- Coverage focus: Fire and loss of use coverage for wildfire exposure, replacement cost for hail

- Community context: Active manufactured housing market in affordable areas south and east of the city

- Season: Year-round, wildfire season peaks June through September

Aurora

Aurora has manufactured home communities primarily in the eastern and southern portions of the city, in areas that developed during earlier waves of manufactured housing growth on the Front Range. The eastern Aurora communities sit in flat terrain where wind is less blocked than in areas closer to the foothills.

DIA sits in the Aurora area and the land use around the airport corridor includes some manufactured housing. The region overall is flat and open, which means both wind and hail exposure are as real as anywhere else on the Front Range.

Aurora’s manufactured home community residents face the same urban considerations as Denver — theft, urban liability exposures, and the need for coverage that actually holds up when you file a claim. Working with an agent who will actually shop your policy across multiple carriers matters in urban areas because pricing and terms vary.

Aurora

- Main risks: Hail, wind on eastern plains edge, theft

- Coverage focus: Replacement cost, wind and hail coverage, personal property

- Community context: Established manufactured home communities in eastern Aurora

- Season: Year-round

Fort Collins

Fort Collins and Larimer County have manufactured home communities in and around the city, with some of the older communities located in the southern and eastern parts of town. The Cache la Poudre River runs through the area and there are some manufactured home communities in lower-lying areas that have faced flooding questions over the years — worth noting that flood damage requires separate flood coverage, not your manufactured home policy.

Hail is a consistent risk in Fort Collins. The northern Front Range gets the same hailstorm patterns as the rest of the corridor. Wind coming off the foothills to the west can be significant during certain weather patterns.

Fort Collins’ manufactured home market has been under price pressure as the broader Northern Colorado housing market has gotten more expensive. Communities that have been there for decades are sometimes the target of redevelopment pressure. None of that affects your insurance directly, but it’s background worth knowing.

Fort Collins

- Main risks: Hail, wind, localized flooding in lower areas (requires separate flood policy)

- Coverage focus: Replacement cost for hail, wind coverage, liability

- Community context: Northern Front Range market with established communities in and around the city

- Season: Year-round

Pueblo

Pueblo and Pueblo County have a significant manufactured housing market. Lower land costs and historically more affordable living conditions have made Pueblo one of the places in Colorado where manufactured homes are a real part of the housing landscape, not just a small niche.

The Arkansas River runs through Pueblo and has a history of flooding. Manufactured home communities in lower-lying areas near the river should take flood coverage seriously — it’s not included in a manufactured home policy and needs to be purchased separately. Pueblo also gets hailstorms, though the frequency is somewhat lower than the northern Front Range.

Wind on the open eastern plains east of Pueblo is significant. High wind events can damage manufactured homes that aren’t anchored adequately, and wind coverage is something to make sure you have clearly in your policy.

Pueblo

- Main risks: Flooding near the Arkansas River (needs separate flood policy), wind, hail

- Coverage focus: Wind coverage, replacement cost dwelling, flood policy separately

- Community context: One of the more significant manufactured housing markets in southern Colorado

- Season: Year-round, flooding risk highest in spring snowmelt

Grand Junction

The Grand Junction area and Mesa County are home to a substantial manufactured housing population. Lower land costs in the Grand Valley and a history of more affordable living on the Western Slope have made manufactured homes a real part of the housing market here.

Grand Junction and the surrounding area deal with significant heat in summer — temperatures regularly well above 100 degrees. That affects HVAC systems and places stress on materials in ways that matter for maintenance and for the background of claims. It’s not a specific coverage item but it’s part of the context.

Wind is a significant factor in the Grand Valley. The terrain channeling and pressure systems that create wind events in that part of the state can be intense. Manufactured homes on open lots or in communities with less windbreak are exposed.

Hail is somewhat less frequent than on the Front Range but still happens. And the overall coverage picture — replacement cost, adequate dwelling limits, liability — is the same priority it is everywhere.

Grand Junction

- Main risks: High wind, heat stress on materials, hail

- Coverage focus: Wind coverage, replacement cost, adequate dwelling limits

- Community context: Western Slope manufactured housing market with lower costs and different risk profile than Front Range

- Season: Year-round, summer heat is extreme

Greeley and Weld County

Weld County deserves specific mention because it’s one of the more significant manufactured housing markets in the state. The combination of available land, agricultural character, and more affordable housing economics has made Greeley and the surrounding Weld County communities home to a large number of manufactured homes.

The oil and gas activity in Weld County has over the years brought workers and families to the area, and manufactured housing has been part of how that population surge was accommodated. Some of those communities are on relatively flat terrain with full Eastern Plains wind exposure.

Hail on the Northern Plains and in the Greeley corridor is serious. Some of the most damaging hailstorms in Colorado history have tracked through Weld County. Manufactured homes in this county need real hail coverage — and replacement cost terms matter here more than almost anywhere else in the state.

Tornado risk also exists in Weld County at a level that doesn’t exist in the mountain areas. This is rare but not zero on the Colorado plains, and wind damage from severe storms is a real exposure.

Greeley and Weld County

- Main risks: Hail (severe frequency), wind, tornado risk on open plains

- Coverage focus: Strong hail coverage with replacement cost, wind damage, adequate dwelling limits

- Community context: One of the largest manufactured housing markets in Colorado outside the major metro areas

- Season: Year-round, severe weather peaks spring and early summer

Steamboat Springs

Manufactured homes in Steamboat Springs and the Yampa Valley serve a function that people don’t always think about when they picture resort towns — workforce housing. Mountain resort communities are expensive, and manufactured homes in areas around Steamboat serve workers, longtime locals, and people who want to live in the valley but can’t afford the luxury home market.

Mountain manufactured home insurance has some specific wrinkles. Snowload is real at the elevations around Steamboat — roofs need to handle significant snow accumulation over a winter. Standard manufactured home policies may not always account for this the way mountain owners need them to. Asking specifically about snowload coverage and what your policy covers in a roof collapse or snow damage scenario is a real conversation to have with your agent.

The compressed construction season in Steamboat also matters for claims. If something happens to your home in November or March, the repair process takes longer and finding contractors available for the work takes more effort than in the city. Additional living expenses coverage that can actually sustain you through a longer displacement is worth having.

Steamboat Springs

- Main risks: Snowload, extreme cold, fire, compressed repair season

- Coverage focus: Snowload and structural coverage, extended loss of use, fire

- Community context: Workforce and long-term local housing in an expensive resort market

- Season: Year-round, winter conditions are serious

Aspen

Affordable housing in the Aspen area is one of the consistent challenges of living in one of the most expensive real estate markets in the country. Manufactured and modular homes play a role in some workforce and affordable housing situations in and around Pitkin County, particularly in communities away from the Aspen core.

The considerations are similar to Steamboat — snowload, extreme cold, short construction seasons for repairs, and the general cost of everything in the area. Labor costs for repairs in and around Aspen are among the highest in the state, which makes having adequate dwelling coverage limits and replacement cost terms especially important. A claim settlement that falls short of actual repair costs is a bigger problem in a market where contractors charge what the market bears.

Aspen

- Main risks: Snowload, high labor costs for repairs, extreme cold

- Coverage focus: Replacement cost with adequate limits for high-cost market, loss of use, snow and ice damage

- Community context: Workforce and affordable housing context in an ultra-high-cost area

- Season: Year-round, heavy winter conditions

Breckenridge and Summit County

Summit County has both a permanent population and a significant second-home population, and affordable housing options in the county have included manufactured homes in some communities. Workforce housing in this part of Colorado is a persistent challenge given how expensive everything has gotten.

Breckenridge sits at 9,600 feet. The manufactured homes at that elevation deal with significant snowpack, cold temperatures, and a short summer window for any exterior work or repairs. Snowload coverage is a must in this environment. The cost of repairs at altitude with limited contractor availability makes adequate coverage limits and replacement cost terms the baseline expectation.

Hail even at higher elevations can be an issue in Summit County during summer months when afternoon thunderstorms roll through. The coverage picture — fire, wind, hail, snow, cold — is comprehensive and the mountain context adds urgency to having all of it in place properly.

Breckenridge and Summit County

- Main risks: Snowload, extreme cold, short repair season, hail in summer

- Coverage focus: Snowload and structural coverage, replacement cost, extended loss of use

- Community context: Workforce and affordable housing in a very high-cost, high-altitude resort market

- Season: Year-round, winters are extended and severe at 9,600 feet

Durango

Durango and La Plata County have manufactured homes in communities around the city and in the more rural parts of the county. The southern Colorado market has lower costs than the resort areas further north, but the risks are real — wildfire, wind, and the general Colorado weather picture all apply.

Wildfire in the San Juan Mountains and the surrounding region is a serious threat. La Plata County has seen significant fire activity over the years. Manufactured homes in or near the wildland-urban interface need solid fire coverage and loss of use coverage that accounts for the possibility of displacement during fire season.

The Animas River runs through Durango and some areas near the river have historical flood exposure. Flood coverage needs to be purchased separately — your manufactured home policy won’t handle it.

Durango

- Main risks: Wildfire, wind, flooding near Animas River (separate flood policy needed)

- Coverage focus: Fire and loss of use, wind coverage, flood policy separately

- Community context: Southern Colorado manufactured housing market in a regional hub

- Season: Year-round, wildfire season June through September

What to Look for in a Colorado Manufactured Home Policy

Across all of these markets, a few things consistently matter for Colorado mobile and manufactured home owners.

Replacement cost vs. actual cash value. This is the most important decision in your policy. Replacement cost pays what it actually costs to repair or replace damaged parts of your home and belongings. Actual cash value factors in depreciation and can leave you significantly short — a roof that’s ten years old might get paid out at a fraction of replacement cost even if replacing it costs the full amount. In Colorado, where hail claims are common, this distinction is very real.

Adequate dwelling limits. Your coverage limit needs to reflect what it actually costs to replace your home, not what you paid for it or what it might sell for on the current market. Manufactured homes that were purchased years ago for less money might cost significantly more to replace with comparable construction today. Don’t underinsure.

Loss of use coverage. If your home becomes uninhabitable after a covered loss, this coverage pays for temporary housing while repairs are being made. In Colorado, where contractors can be backed up and repair timelines can be extended by weather and season, having enough loss of use coverage matters. Mountain areas especially.

Wildfire coverage and exclusions. Read your policy and understand what it says about fire. Most standard policies cover fire, but if you’re in a high-risk wildfire area, carriers may have limitations or specific exclusions. Know what you have.

Uncle Sheldon is independent, which means we work with multiple carriers and we’re not going to give you one option and call it a day. We’ll look at your situation — where you live in Colorado, what your home is worth, what your real risks are — and find coverage that actually fits. Reach out and talk to a real agent. We’re here to help you figure this out.