Condo Ownership in Colorado Has a Lot of Variables

Colorado is a state where condo ownership looks really different depending on where you are. A Denver urban infill condo in a newer midrise building is a completely different situation from a slopeside ski unit in Breckenridge that you rent out half the season. A Boulder condo in a converted Victorian-era building operates under a different set of risks than a Grand Junction condo in the high desert. The insurance picture changes with all of those variables.

The basics of how condo insurance works — the split between what the HOA covers and what you cover as an individual unit owner — are the same everywhere in Colorado. But the specific risks, the HOA structures, the rental considerations, and the things that affect your premium are very much tied to location. That’s what this page is about.

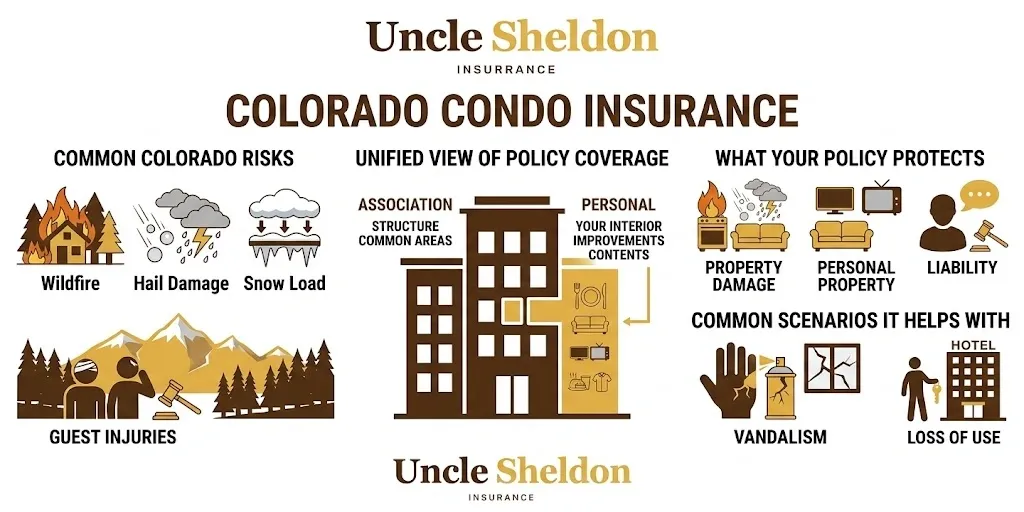

Colorado has its own condo ownership landscape that comes with some things people from other states don’t always expect. Hail is a real issue across the Front Range in ways that surprise people new to the area. Wildfire has affected neighborhoods in the foothills and even suburban areas that didn’t historically feel like they were in fire country. Short-term rental activity in ski resort towns changes the whole insurance conversation. And the HOA master policy setup at any given building can vary widely, which is the first thing you really need to understand before you figure out what your personal policy has to do.

The HOA Master Policy Question — and Why It Matters Even More in Colorado

Regardless of what city or town you’re in, the most important first step with condo insurance in Colorado is understanding what your HOA’s master policy actually covers. This determines how much dwelling coverage your own HO-6 policy needs to carry.

There are two main types of master policies out there. A bare walls-in policy covers the building structure — the exterior, the roof, the shared walls, the hallways, the lobby — but not the interior finishes of individual units. Your flooring, your cabinets, your countertops, your bathroom tile, your built-in appliances — those fall to your own policy under a bare walls-in setup. Most HOAs in Colorado use this structure, which means most condo owners here need meaningful dwelling coverage on their personal HO-6.

An all-in master policy covers the original installed finishes within each unit in addition to the building structure. If your building has this type, the HOA’s policy handles the original flooring, built-ins, and fixtures. Any improvements or upgrades you’ve made above the original spec are still your responsibility.

Get a copy of your HOA’s master policy declarations page. The HOA is required to provide this, and it tells you exactly where their coverage ends and yours begins. Without that document, you’re guessing — and guessing wrong on dwelling coverage is one of the most common and most costly mistakes condo owners in Colorado make.

One thing worth knowing about Colorado specifically: the state has a body of law called the Colorado Common Interest Ownership Act, which governs HOA-owned properties including condos. This law affects how HOAs operate and what they’re required to do, but the specifics of insurance are still primarily determined by the individual HOA’s documents and master policy — not state law mandating specific coverage terms. Don’t assume that Colorado law guarantees a certain level of HOA coverage. Read your specific HOA’s documents.

Hail in Colorado — A Bigger Deal Than Most States

Colorado is one of the most hail-prone states in the country, and the Front Range corridor from Fort Collins down through Denver and Colorado Springs is in the thick of it. Hail events in this part of Colorado are not rare occurrences — they’re a recurring seasonal reality.

For condo owners, the direct hail risk to your unit depends on your HOA structure. Roof and exterior damage from hail typically falls under the HOA’s master policy. But the downstream effects of hail — water intrusion, damage to HVAC equipment that may be your responsibility, damage to windows or skylights that are in a gray area between your unit and the building — can end up affecting you even when the primary building damage is an HOA claim.

The bigger issue is that Colorado’s hail environment affects insurance pricing and carrier availability across the board. Insurers operating in Colorado have to factor in hail exposure, and that shows up in premiums — particularly for condos in the Denver metro, the Boulder area, and Colorado Springs. If your condo insurance seems more expensive than you expected compared to a previous state you lived in, hail exposure is often part of the explanation.

Wildfire Risk and What It Does to Coverage

Wildfire has become a real insurance factor in Colorado in a way that it wasn’t twenty years ago. The Marshall Fire that tore through neighborhoods near Boulder in December 2021 was a wake-up call — it destroyed hundreds of homes, including attached units and townhomes in areas that weren’t traditionally considered high fire risk.

Mountain and foothills condo owners have always needed to think about wildfire. But increasingly, the fire risk conversation extends into suburban and exurban communities that sit at the wildland-urban interface — places where neighborhoods meet undeveloped open land.

If your condo is in a mountain town, a foothills community, or anywhere that backs up to open space or wildland, wildfire should be part of your coverage conversation. A few things worth talking through with your agent:

- Does your HOA’s master policy include wildfire rebuilding coverage and are those limits adequate

- What does your own dwelling coverage look like in a total-loss scenario

- Are there carriers who are limiting wildfire coverage in your area or not writing new policies there

The insurance market for wildfire-exposed properties in Colorado has gotten more difficult in recent years. Some carriers have pulled back or restricted coverage in certain zip codes. An independent agent who can shop across multiple carriers is genuinely valuable in this environment because the options vary significantly by carrier.

Short-Term Rentals in Colorado Ski Towns

A big chunk of condos in Colorado’s ski resort markets — Vail, Breckenridge, Aspen, Telluride, Steamboat Springs — are used as short-term rentals at least part of the year. It’s just how those markets work. Owners buy a unit, use it some weekends, and put it on VRBO or Airbnb or a local property management program the rest of the time.

Standard condo insurance is designed for owner-occupants, not rental activity. If you’re renting your unit to guests — even occasionally — your standard HO-6 policy may not respond to claims that arise during a rental period. That’s a real problem if a renter damages the unit or if a guest gets injured and you assumed your insurance covered it.

Short-term rental insurance options have gotten better in recent years. Some carriers offer endorsements specifically for short-term rental activity. There are also standalone short-term rental policies designed for this use case. If you own a mountain condo that you rent out, even just a handful of times a year, this is a conversation you need to have with your agent before something happens. Finding out your policy doesn’t cover a rental situation after a claim is a bad way to learn this.

Denver

The Denver condo market has grown substantially over the past fifteen years and the range of condo types in the city is wide. Older converted buildings in Capitol Hill and Congress Park. New urban infill midrise construction in RiNo, the Highlands, and LoHi. High-rise buildings downtown and in the Cherry Creek area. Each building type comes with its own HOA structure and master policy setup.

Denver condos on the Front Range deal with hail exposure. The storms that roll through the Denver metro in late spring and summer can drop significant hail, and while the building’s exterior damage goes to the HOA’s master policy, unit owners need to understand their own exposure for window damage, skylights, and anything considered part of their unit.

Liability coverage matters in Denver’s urban condo buildings. Multi-unit buildings with shared hallways, elevators, and amenities create scenarios where a claim can involve multiple parties. If water from your unit damages the unit below, your liability coverage responds to that. Make sure your liability limits are set thoughtfully — the default starting limit on many policies isn’t always enough.

Denver also has a significant short-term rental activity in some neighborhoods. If you’re renting your Denver condo through a platform or privately, make sure your coverage is structured for it.

Colorado Springs

Colorado Springs has a growing condo market with units ranging from affordable complexes on the eastern and northern parts of the city to more upscale developments near Broadmoor and Monument. The city’s growth has brought more condo development and with it more HOA-governed properties.

Hail exposure in Colorado Springs is real — the city sits in the same Front Range hail corridor as Denver. The eastern and southern parts of the city can be particularly exposed to summer hail events. If your condo is in a building that has had hail claims in recent years, that history can affect master policy renewal pricing and potentially trickle down to loss assessment considerations for unit owners.

The wildland-urban interface is present in parts of Colorado Springs as well, particularly in the northwest and west parts of the city where development meets mountain terrain. Wildfire coverage conversations are relevant for condos in those areas.

Fort Collins

Fort Collins has a strong condo and attached home market driven partly by Colorado State University and partly by the city’s general desirability. Student-area condo buildings near the university have their own insurance character — high turnover, common rental activity, buildings that see a lot of use.

Rental activity is probably the most common insurance consideration to address in Fort Collins condos. Whether you’re renting to a student, a working professional, or listing on a short-term platform, standard HO-6 coverage may not be the right fit. Knowing what your HOA’s documents say about rental activity is also worth checking — some Colorado HOAs restrict rental use and that can have insurance implications.

Hail is part of the Fort Collins weather picture too, particularly in spring and early summer. Building damage goes to the HOA, but unit owners should know where their exposure starts.

Aspen

Aspen is one of the most expensive real estate markets in the country, and the condo market here is no exception. Slopeside and in-town condos in Aspen carry values that are high enough to make getting the dwelling and personal property coverage right genuinely important.

Most Aspen condos see significant short-term rental use. Whether managed through a private management company or a direct platform, rental activity in Aspen is the norm rather than the exception. Insurance needs to be structured accordingly — standard owner-occupant HO-6 coverage is almost certainly not adequate for a condo that’s rented regularly.

Personal property coverage in Aspen should be reviewed carefully. High-value furnishings, ski equipment, art, and other valuables in luxury mountain units can exceed standard policy limits without proper scheduling. Talk through what you actually own and make sure the policy accounts for it.

Wildfire exposure in the Aspen area and surrounding Roaring Fork Valley is worth a conversation with your agent. Mountain terrain and dry summers are part of the picture.

Vail

Vail is primarily known as a ski resort but it’s also a genuine residential community with condos in the village, along Gore Creek, and in the surrounding areas. A lot of Vail condo owners are not full-time residents — they’re using units as part-time vacation properties and offsetting the cost with rental income.

The short-term rental situation in Vail is essentially the same as Aspen — if you’re renting, your insurance needs to be structured for it. The combination of high unit values, vacation rental activity, and mountain weather exposure makes getting the right coverage important.

Loss assessment coverage is worth paying attention to in Vail. HOA assessments in resort property buildings can be substantial, and standard loss assessment limits on many policies may not be adequate. Ask specifically about this when you’re setting up coverage.

Breckenridge

Breckenridge is one of the most popular ski resort towns in Colorado and the condo market is enormous — everything from budget-friendly slopeside studios to large multi-bedroom units in newer developments. The range of property values and HOA structures across Breckenridge’s condo inventory is significant.

Almost every condo in Breckenridge deals with the short-term rental question. The town’s economy is built around tourism and most unit owners have rental activity at some point. If you own a condo in Breckenridge and it’s ever rented to guests, your insurance structure needs to account for that.

Weather at 9,600 feet elevation means snow loads on roofs, ice dam risks in winter, and freeze-pipe events in units that sit unoccupied. Most of the structural stuff falls to the HOA’s master policy, but unit owners can face their own exposure — pipes that freeze within the unit, water damage from ice dam intrusion, or damage to personal property during a weather event. Make sure your policy covers water damage from sudden and accidental pipe failures, which is one of the most common condo claims in mountain communities.

Telluride

Telluride combines extreme scenery, extreme property values, and extreme remoteness. Getting repairs done in Telluride after a loss is more expensive than in accessible markets because of the logistics of getting contractors and materials into a canyon town. That’s worth factoring into dwelling coverage amounts — rebuilding costs in remote mountain locations can be higher than standard estimates.

Short-term rental activity in Telluride is common. Same story as the other ski resort markets — standard HO-6 coverage is designed for owner-occupants, and rental use needs to be specifically addressed.

Mountain Pack personal property exposure exists here too. Ski equipment, gear, and outdoor adventure equipment is often stored in or around units, and the value of that equipment can add up. Review your personal property coverage and any sub-limits for specific categories.

Steamboat Springs

Steamboat Springs is a ski resort town with a slightly more accessible and relaxed character than Aspen or Vail. The condo market here has significant vacation property and short-term rental activity, particularly around the ski resort base area.

Same core considerations apply — short-term rental coverage, loss assessment coverage, weather-related risks from snow and freeze events, and wildfire awareness in the surrounding terrain. The Yampa Valley location means some parts of the broader Steamboat area have wildfire exposure worth discussing.

Estes Park

Estes Park at the entrance to Rocky Mountain National Park attracts vacation property ownership and short-term rental activity. Condo ownership here is often tied to the tourism economy, and insurance coverage needs to reflect rental use.

Wildfire risk around Estes Park and the surrounding mountains is real. The area has seen fire activity in recent years and the proximity to Rocky Mountain National Park and forested terrain means fire exposure should be part of the conversation with your agent.

The short tourist season and the remote mountain setting mean that winter vacancy is common for some Estes Park condo owners. Unoccupied units in cold mountain settings have freeze-pipe risk during vacancy periods. Some policies have vacancy clauses that can affect coverage if a unit sits empty for extended periods — worth knowing about before you find out the hard way.

Durango

Durango has a condo market that serves both full-time residents and second-home buyers who want southwestern Colorado mountain character without the resort-town prices. The area has a mix of in-town properties and more rural settings in the San Juan Mountains.

Wildfire exposure in the Durango area and the broader San Juan region is a real consideration. The surrounding terrain is heavily forested and fire has affected the area over the years. For condos in or near wooded terrain, wildfire coverage is a serious topic.

Durango’s short-term rental market exists but is smaller than the major ski resort markets. Standard condo coverage may be adequate for owner-occupants, but rental activity should still be disclosed to your agent.

Grand Junction

Grand Junction is the largest city on the Western Slope and has a growing condo market serving both full-time residents and people connected to the energy industry and agricultural sector that drives much of the regional economy. It’s a more affordable market than the mountain resort towns.

The climate in Grand Junction is semi-arid with hot summers. The fire risk picture here is different from the mountain forests — more open terrain, grass fires — but it’s still worth knowing your exposure. Water damage from summer thunderstorm activity is also worth having covered.

Grand Junction sits in the Colorado River Valley and some areas have flood risk associated with the river system. Standard condo insurance doesn’t cover flood — that requires a separate flood policy through the National Flood Insurance Program or a private flood insurer. If your unit is in a lower-lying area near the river, it’s worth knowing whether you’re in a flood zone.

Aurora

Aurora is a major Denver suburb with a large and diverse housing market. Condo construction in Aurora covers a wide range — affordable developments on the eastern end of the city, newer construction near the light rail lines, and older buildings in the central parts of town.

Hail exposure is the same as the broader Denver metro — it’s a recurring risk in summer and affects Front Range insurance pricing across the board. Loss assessment coverage matters here because a major hail event on a large condo complex can generate significant assessments to individual unit owners if the master policy limits or deductibles don’t fully cover the damage.

Lakewood

Lakewood is a western Denver suburb with a mix of condo types, from older garden-style complexes to newer urban-format buildings. The proximity to the foothills gives some Lakewood properties an elevated wildfire exposure compared to central metro locations.

Storm and hail risk is consistent with the Denver metro pattern. Properties near the foothills can get more intense storm activity than properties further east. Coverage should reflect the actual location and exposure.

Pueblo

Pueblo in southern Colorado has a more affordable housing market than the Denver metro or resort towns, and the condo market here is primarily oriented toward residents rather than vacation buyers. Insurance is generally more accessible and less expensive in Pueblo than in higher-risk or higher-value markets.

Southern Colorado weather — hot summers, occasional severe storms, some winter weather — is the main consideration. Pueblo sits near the Arkansas River and some areas carry flood risk. As with Grand Junction, standard condo insurance doesn’t cover flood, and knowing whether your unit has flood zone exposure is worth checking.

Centennial

Centennial is a planned city in the south Denver suburbs with a lot of newer construction, including condo developments that serve young professionals and downsizers who want to stay in the metro area. It’s a well-maintained community with generally newer HOA-managed properties.

Insurance considerations in Centennial follow the Denver metro pattern — hail exposure, loss assessment coverage for front-range weather events, and standard personal property and liability coverage. Newer buildings tend to have more predictable HOA master policies, but the specific terms still need to be reviewed.

The Rental Condo Question in Colorado — One More Time

It’s worth saying clearly one more time because it comes up so often in Colorado: if you rent your condo at all — to a long-term tenant, a short-term guest, through a property manager, through Airbnb, through any arrangement — your standard HO-6 owner-occupant policy may not cover claims arising during that rental period.

This is especially true in mountain resort markets where rental activity is the norm, but it applies across the state. The fix isn’t complicated — it’s just about making sure your policy is structured correctly for how you actually use the property. An agent who understands rental activity and has access to carriers that properly cover it can set this up without a lot of drama.

| Property Use | Typical Coverage Approach |

|---|---|

| Full-time owner-occupied | Standard HO-6 condo policy |

| Part-time owner use, no rentals | Standard HO-6 with vacancy considerations |

| Occasional short-term rental | Short-term rental endorsement or standalone rental policy |

| Frequent short-term rental | Dedicated short-term rental or landlord policy |

| Long-term tenant year-round | Landlord or dwelling fire policy |

A Note on Loss Assessment Coverage in Colorado

Loss assessment coverage is something a lot of condo owners overlook and it can matter a lot in Colorado. Here’s why it’s worth paying attention to specifically here:

Large hail events on the Front Range can affect entire condo complexes at once. If a major storm generates significant roof and exterior damage across a large building and the repair costs approach or exceed the HOA master policy limits, or if the master policy has a large deductible, individual unit owners can be assessed for a portion of the remaining cost. That assessment can be meaningful.

The same principle applies to wildfire rebuilding scenarios — if a major fire event generates claims that push against HOA coverage limits, assessments to unit owners are a real possibility.

The default loss assessment limit on many HO-6 policies is low — sometimes only $1,000 to $2,000. Given the types of large-scale loss events that can happen in Colorado, it’s worth talking to your agent about whether your loss assessment coverage is set at a level that actually provides meaningful protection.

Working With Uncle Sheldon on Colorado Condo Coverage

Look, condo insurance in Colorado isn’t one-size-fits-all. A resort condo in Breckenridge needs different coverage than an urban condo in Denver, which needs different coverage than a Pueblo unit that’s been owner-occupied for fifteen years. The HOA setup matters, the rental situation matters, the location and its specific risks matter.

Uncle Sheldon is an independent agency and we work with multiple carriers. We’re not stuck pushing one company’s policy — we can shop across the market to find coverage that fits what you actually need. And we work with real people. You’ll talk to a human agent who can ask the right questions, understand your situation, and put together something that makes sense. Not a robot, not an algorithm.

If you own a condo anywhere in Colorado and want to make sure you’re covered the right way — whether you’re buying for the first time, switching carriers, or you just want a second set of eyes on what you have — reach out to us. We’ll work through it with you.