Running a food truck is essentially taking a fully functioning commercial kitchen, strapping it to a truck chassis, and driving it through city traffic. It’s a great way to build a food business without taking on the massive rent and overhead of a brick-and-mortar restaurant. But from an operational standpoint, it combines the risks of a commercial vehicle with the constant hazards of a high-volume kitchen.

You are dealing with open flames, deep fryers, and heavy equipment, all while trying to handle potholes, tight event spaces, and terrible drivers on the highway. Then you park, pop the window open, and serve hundreds of people as fast as humanly possible.

Because of this unique setup, food truck insurance isn’t just one standard policy you pull off a shelf. It is a mix of different coverages designed to address both the driving side and the serving side of the business. How these coverages fit together matters quite a bit. If you just buy a basic auto policy, you leave the kitchen completely exposed. If you just focus on the liability of serving food, you are in trouble if the truck itself gets wrecked on the way to a gig.

Here is a plain-English look at how the different pieces of food truck insurance actually work, what the coverages do, and what you need to be thinking about when putting your protection together.

The Auto Side of the Business

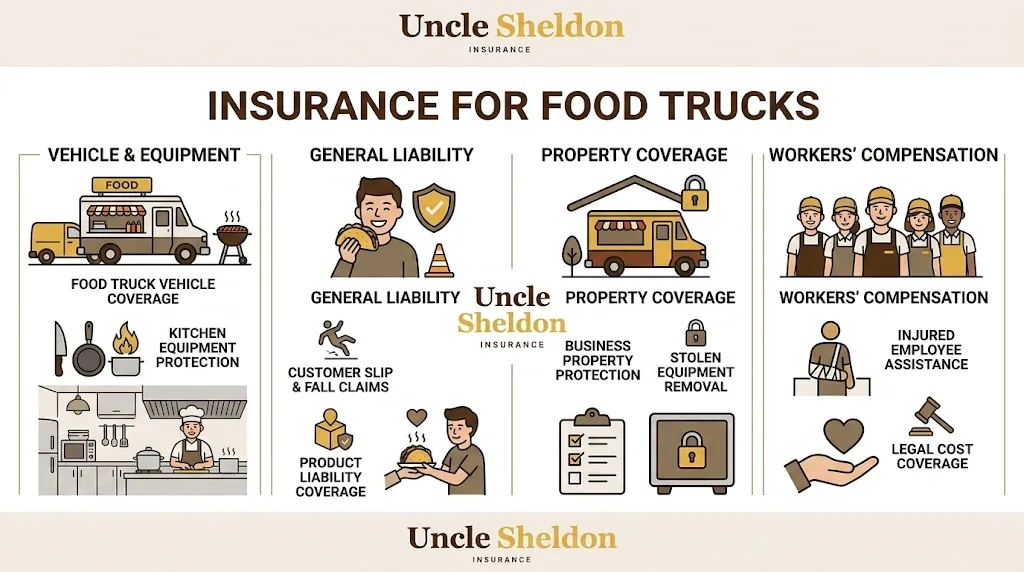

Since your entire business is built on a vehicle, the truck itself is usually the first thing owners think about. A personal auto policy will absolutely not cover a food truck. Once you use a vehicle primarily for commercial purposes—especially one modified with commercial cooking equipment—you need a dedicated commercial auto policy. If you try and slide a food truck under a personal auto policy, any claim is just going to get denied.

Commercial Auto Liability

If you are driving to a music festival and rear-end another car, or if you accidentally back into a parked vehicle while trying to squeeze into a tight spot downtown, commercial auto liability kicks in. It covers the bodily injury and property damage you cause to other people while driving the truck. Most event organizers, commissary owners, and city permit offices require a specific minimum amount of auto liability just to let you operate on their property.

Physical Damage Coverage

Liability covers the other guy, but physical damage coverage protects your truck. If you get into a wreck, or if a severe hail storm batters the side of the truck and ruins the custom wrap, this covers the cost to repair your vehicle.

There is a critical detail here for food truck owners that gets messed up a lot. You need to make sure the policy actually accounts for the value of the kitchen build-out. A standard used box truck might be worth $30,000 on its own. But with the fryers, the flat top grill, the fire suppression system, the plumbing, and the custom wrap, your food truck might easily be worth $100,000 or more. If the insurance company only values it as an empty delivery truck, a total loss could wipe you out. Make sure the stated amount on the policy reflects the true replacement cost of the fully built truck, not just the base vehicle.

The Restaurant Side of the Business

Once the truck is parked, the engine is off, and the window is open, the auto policy largely goes to sleep and the business liability policies take over.

General Liability

This is the absolute foundation for any food business. General liability covers you if a third party—meaning a customer, a vendor, or just a bystander—gets hurt or their property is damaged because of your business operations.

For food trucks, the classic example is a slip and fall. Someone spills a greasy drink in front of your window, the next customer slips on the wet pavement, hits their head, and needs an ambulance. General liability covers those medical bills and your legal defense if they decide to sue the business.

It also covers property damage you might cause at a location. If you accidentally scrape the side of a building while setting up, or if your generator leaks oil all over a client’s expensive stamped concrete driveway during a private catering gig, general liability handles the cleanup and repair costs so you don’t have to pay out of pocket.

Product Liability

This is usually bundled right inside your general liability policy, and it is arguably the most critical coverage for anyone serving food to the public. Product liability protects you if the food or drink you serve actually causes harm.

If a batch of chicken isn’t held at the proper temperature and a dozen people get severe food poisoning, or if an allergen cross-contaminates a dish despite your best efforts and a customer has a severe reaction, product liability steps in. It handles the medical claims, the settlements, and the legal fallout. In the food world, this is a risk that never goes away, no matter how clean your kitchen is or how careful your prep process is.

Protecting the Equipment

Your truck is full of incredibly expensive gear. While physical damage coverage on the auto policy covers the vehicle if it crashes, what happens to the equipment if something else goes wrong?

Inland Marine Coverage

In a normal restaurant, commercial property insurance covers the ovens and fridges inside the building. But food trucks are mobile, which means standard property insurance often doesn’t apply because the property isn’t staying at a fixed address.

Instead, food trucks usually rely on something called Inland Marine coverage. It’s an old insurance term that basically just means “property in transit.” This covers your cooking equipment, POS systems, generators, and inventory while it is moving around the city or parked at different locations. If someone breaks into the truck overnight and steals your high-end generator and your espresso machine, or if a grease fire damages the interior of the kitchen without destroying the whole truck, inland marine coverage pays to replace the stolen or damaged items.

Equipment Breakdown

Standard property or inland marine coverage handles external events like fire or theft. It does not handle mechanical failure. If your walk-in cooler compressor just burns out on a 100-degree day in July, or your primary generator suffers a massive internal electrical failure, standard insurance won’t help you at all. That is considered a maintenance issue.

Equipment breakdown coverage specifically steps in for these sudden mechanical or electrical failures. It helps pay for the repairs or replacement so you aren’t completely sidelined by a dead motor or a fried electrical panel.

Spoilage

When that fridge compressor dies, you don’t just have a broken fridge—you have a fridge full of warming meat, dairy, and prepped ingredients. Food trucks carry thousands of dollars of inventory in a very tight space. Spoilage coverage reimburses you for the cost of the perishable goods you lose because of a power outage or equipment failure. Replacing a weekend’s worth of inventory entirely out of pocket can be devastating to your cash flow, so adding spoilage coverage is a very practical move.

Keeping the Business Alive

When things go wrong, the physical repairs are really only half the problem. The other half is the money you are losing while you can’t operate.

Business Interruption

If a distracted driver hits your parked truck and puts it out of commission for a month, the auto liability might pay for the truck repairs, but you are still losing a month of revenue. You still have to pay your commissary rent, you might have monthly loan payments on the truck itself, and you obviously need to pay yourself.

Business interruption insurance (often called business income coverage) is designed to replace your lost net income and cover your ongoing fixed expenses while your operations are suspended due to a covered claim. For a business where your entire ability to generate revenue is tied to one single vehicle, being down for a month without cash coming in can easily sink the operation.

Protecting the People

Working on a food truck is physically demanding. It gets incredibly hot, the quarters are cramped, and people are moving fast with sharp knives and boiling oil. Injuries are going to happen.

Workers Compensation

If you have employees, almost every state requires you to carry workers compensation insurance. Even if it’s just one or two part-time helpers working the window on weekends, you need it.

If an employee slips on a greasy floor and breaks their arm, or gets a severe burn from the fryer splashing during a rush, workers comp pays for their medical treatment and a portion of their lost wages while they heal. It also fundamentally protects the business. In most states, an employee who accepts workers comp benefits gives up the right to sue the employer directly for the injury.

Given the environment inside a food truck, minor burns and cuts are just part of the job. But severe injuries happen more often than people like to admit. Having this coverage in place is legally necessary in most places, but it’s also just important for protecting your crew.

Employment Practices Liability

This is something small food truck operations often ignore, thinking it’s only for big corporate offices. Employment Practices Liability Insurance (EPLI) protects the business against claims made by employees alleging wrongful termination, discrimination, sexual harassment, or wage and hour disputes.

In a high-stress, fast-paced environment where tempers can flare and turnover is high, these types of claims do happen. Defending against an employee lawsuit can cost tens of thousands of dollars in legal fees, even if you did nothing wrong. EPLI covers those defense costs and any settlements.

Liquor Liability

A lot of food trucks don’t serve alcohol, but if you do, or if you partner with a brewery and sometimes pour under a special permit, you have to think about liquor liability.

Standard general liability policies almost universally exclude claims related to the sale or service of alcohol. If you serve a customer who is already intoxicated, and they get in their car and cause a wreck, your business can be sued under state dram shop laws. Liquor liability steps in to cover the legal defense and the massive potential damages in those scenarios. If you serve booze, you need it. Period.

Navigating Events and Commissaries

One of the biggest headaches for food truck owners isn’t actually buying the insurance—it is dealing with the paperwork required just to do your job.

Almost every festival, private catering client, city permit office, and commissary kitchen will require you to provide a Certificate of Insurance (COI) proving you have coverage. They don’t just take your word for it, they want the actual document.

Very often, these entities will also ask to be named as an “Additional Insured” on your policy. This basically means your insurance policy extends some protection to them if your truck causes a problem on their property. For example, if you are at a local food truck rally and your fryer starts a fire that damages the organizer’s event tent, naming the organizer as an additional insured means your policy will handle the damages, rather than the organizer’s insurance having to step in.

When you set up your policy, it is worth knowing that you will be asked for these certificates constantly. Having an insurance provider or broker that can easily and quickly generate COIs and additional insured endorsements will save you hours of frustrating administrative work over the course of a season. Missing out on a lucrative event because you couldn’t get a certificate in time is incredibly frustrating.

What to Look for When Setting Things Up

Putting together a solid insurance program for a food truck takes a little bit of careful tuning. You don’t want to buy off-the-shelf restaurant policies that don’t account for the mobile nature of the kitchen, and you definitely don’t want an auto policy that undervalues the expensive custom build you paid for.

Take the time to look closely at the deductibles across your coverages. A higher deductible will definitely save you money on the monthly premium, but you have to be completely honest with yourself about your cash flow. If having to front a $2,500 deductible to get your fridge fixed would cripple the business, it is better to pay a slightly higher premium for a $500 deductible.

The risks on a food truck are incredibly tangible. You deal with fire, heavy traffic, perishable food, and unpredictable crowds every single day. Getting the coverage right isn’t just a regulatory hoop to jump through so you can park at a festival; it is the safety net that ensures a bad day on the road doesn’t wipe out the business you’ve worked so hard to build.