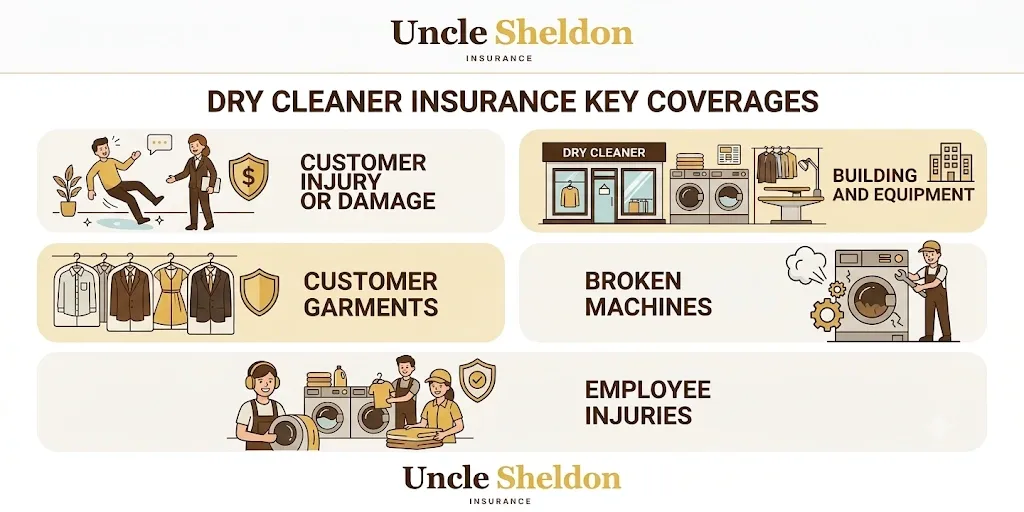

Operating a dry cleaning business means taking physical possession of other people’s property every single day. You take in expensive garments, subject them to chemical solvents, heavy agitation, and high heat, and then you are expected to return them in perfect condition. It is a business model with a lot of inherent risk before you even consider the heavy machinery and environmental factors.

Most small business owners think about protecting their building and maybe some general liability for slip and fall incidents. For a dry cleaner, the picture is much broader. You have thousands of dollars of customer clothing hanging on your conveyors. You operate complex industrial equipment that relies on high pressure steam. You might use cleaning solvents that environmental regulators watch very closely.

The insurance program for a dry cleaning operation has to address all of those specific realities. A massive central plant with multiple routes needs a different structure than a single suburban drop store, even though the basic building blocks of the coverage are similar.

Plants Versus Drop Stores

The first thing an underwriter looks at is whether the location actually processes garments or just takes them in.

A drop store simply takes in clothes, holds them, and sends them out to a central plant for cleaning. The risks here are relatively mild. You have basic premises liability, the risk of a break in, and the bailee exposure of holding customer clothes overnight.

An active plant is an entirely different situation. A plant has boilers, industrial presses, spotting chemicals, and dry cleaning machines running solvent. The risk of fire is higher. The risk of an employee injury is much higher. The environmental exposure is significant.

If you own a central plant and several drop locations, the policies are usually structured to reflect the heavy exposure at the main facility and the lighter exposure at the retail fronts.

The Foundation of General Liability and Property

For the vast majority of dry cleaners, the baseline policy is a Business Owner Policy, which is almost always called a BOP. This package combines your commercial property coverage with your general liability coverage.

The general liability side protects the business if a third party gets hurt or their property is damaged. If a customer slips on a wet spot near the counter on a rainy day, general liability handles the medical bills and the potential lawsuit. If your delivery driver accidentally knocks over a valuable vase while dropping off a VIP customer’s laundry, general liability covers the property damage.

The commercial property side covers your physical assets. This includes the building if you own the real estate. If you lease your space, it covers your tenant improvements, your counters, your computers, and your machinery.

The equipment in a dry cleaning plant represents a massive capital investment. Between the primary dry cleaning machines, the boilers, the air compressors, the tensioning equipment, and the conveyors, a single plant can easily hold hundreds of thousands of dollars in machinery. The property portion of the BOP is what replaces this equipment if it gets destroyed by a fire, a severe storm, or vandalism.

Protecting Customer Property with Bailee Coverage

Standard property insurance covers stuff you own. It absolutely does not cover the property of others that happens to be in your shop.

For a dry cleaner, this is where the biggest daily exposure lives. On any given Tuesday, you might have five hundred garments hanging on the slick rail waiting for pickup. A single rack of designer dresses, custom suits, and high end coats could be worth tens of thousands of dollars.

Bailee coverage specifically protects customer property while it is in your care, custody, or control. If a fire breaks out overnight and destroys the entire plant, bailee coverage is what pays to compensate your customers for their ruined clothing.

This coverage usually operates on a no fault basis. You do not have to be proven negligent for the policy to pay out. The customer entrusted their property to you, the property was destroyed, and the policy compensates them.

Setting up bailee coverage requires looking at the limits carefully. A policy might have a total limit for a catastrophic loss, but it might also have a per garment limit. If your per garment limit is capped at a low number and you routinely process luxury brand clothing or wedding dresses, you have a problem. The limits must reflect the actual value of the inventory you hold during your absolute busiest season of the year.

The Environmental Reality and Pollution Liability

The dry cleaning industry has a complicated history with environmental regulations, primarily surrounding the use of perchloroethylene, commonly known as perc. Even as the industry shifts toward hydrocarbon solvents, silicone alternatives, and professional wet cleaning, the environmental exposure remains a serious concern for any active plant.

A standard general liability policy almost universally excludes pollution and environmental contamination. If a solvent spill reaches a floor drain or slowly leaks into the soil behind your building, standard insurance will not help you.

Environmental remediation is staggeringly expensive. State environmental agencies have strict protocols for cleaning up soil and groundwater contamination. The process can literally take years and cost hundreds of thousands of dollars. It is the kind of expense that easily bankrupts a small family business.

Pollution liability coverage is specifically designed to handle these environmental incidents. It covers the cleanup costs mandated by regulators and can also cover third party lawsuits if contamination from your plant affects a neighboring property.

Operating an active plant with solvent on the premises means you really need to look at pollution liability. Furthermore, leasing a space for a new plant usually means dealing with a commercial landlord who requires pollution liability before they will hand over the keys. Landlords do not want to be left holding the bag for a cleanup if your business goes under.

Equipment Breakdown Keeps the Plant Running

A dry cleaning plant is entirely dependent on its equipment. If the boiler goes down, the presses stop working and the entire production floor grinds to a halt.

Standard commercial property insurance covers your machines if they burn in a fire or get smashed by a collapsing roof. It does not cover them if a motor simply burns out or a boiler cracks from internal pressure.

Equipment breakdown coverage fills this specific gap. It pays to repair or replace mechanical, electrical, and pressurized systems that fail due to an internal breakdown. In a dry cleaning plant, the boiler is the heart of the operation, but you also have chillers, heavy duty air compressors, and the dry cleaning machines themselves.

A major machinery failure brings expensive repair bills, but the lost production time is often worse. Equipment breakdown coverage can help cover the cost of expediting replacement parts. That is a massive help when you have hundreds of dirty garments piling up in the back room and angry customers waiting at the front counter.

Business Interruption Coverage

A fire sweeping through your plant means the commercial property policy handles the cost to rebuild the structure and buy new equipment. However, rebuilding a specialized facility takes a long time. Heavy three phase electrical work, specialized plumbing, and specific ventilation systems must be installed before you can reopen.

During those months of downtime, your business generates zero revenue. The fixed costs do not stop. Rent is still due, equipment loans still require monthly payments, and you probably want to keep your best spotter and your lead presser on the payroll so they do not find jobs at a competing plant.

Business interruption coverage replaces the income your business loses during a forced closure. It is designed to keep the business financially viable while the physical location is being rebuilt. Discussing this with an agent requires honesty about how long a rebuild would actually take. Many standard policies offer twelve months of coverage. That sounds like a lot until you start dealing with city permitting offices and commercial contractors.

Workers Compensation for a Demanding Environment

Working on the floor of a dry cleaning plant is a tough job. The environment is hot, the work requires repetitive motion, and employees are constantly moving heavy bins of wet clothing.

Injuries happen. Employees get burned on steam pipes or hot presses. They pull muscles lifting bags of garments. They might suffer from chemical exposure or repetitive strain injuries from standing at a pressing station for eight hours a day.

Workers compensation covers the medical expenses and a portion of lost wages when an employee gets hurt on the clock. It is a mandatory requirement in almost every state if you have employees on the payroll.

Beyond being a legal requirement, it is a crucial financial shield for the business owner. In most situations, workers compensation acts as an exclusive remedy. This means that if an injured employee accepts the workers compensation benefits, they generally cannot turn around and file a separate civil lawsuit against the business for the injury.

Handling the Delivery Route Exposure

Pickup and delivery routes have seen a massive resurgence as customers demand more convenience. Running a fleet of branded box trucks or having an employee use their personal sedan to drop off clean clothes creates a serious auto exposure.

A personal auto policy will not cover a vehicle that is being used for business deliveries. If your driver rear ends someone while running a route, their personal insurance carrier will likely deny the claim the moment they find out the vehicle was doing commercial work.

Businesses that own their route vehicles need a commercial auto policy. If your employees use their own cars to run errands, go to the bank, or drop off garments, you need hired and non owned auto coverage. This protects the business if the business is sued over an accident caused by an employee driving a personal vehicle for work.

What Impacts the Cost

The price of a dry cleaner insurance program varies wildly based on the specifics of the operation.

An operation with a central processing plant and fifty employees pays significantly more than a single location drop store with two part time workers. The gross revenue and total payroll are the primary metrics that insurance companies use to scale the pricing.

The type of solvent used at the plant makes a big difference, particularly for pollution liability pricing. A plant running perc is generally viewed as a higher risk than a plant running silicone or water based cleaning systems.

Your history of claims matters. Frequent bailee claims for lost or damaged garments or a history of workers compensation injuries will cause underwriters to price the policy higher or decline to offer coverage entirely.

Building construction plays a role. An older building with outdated electrical panels and no fire sprinkler system costs more to insure than a modern facility built with fire resistant materials and robust suppression systems.