Running a catering business is a heavy lift. You aren’t just cooking food in a controlled, predictable environment. You are packing up an entire commercial kitchen operation, driving it across town, and setting it up in places you don’t control. You could be working out of a pristine, high-end hotel ballroom one day, and a makeshift tent in a muddy field the next. It takes an incredible amount of logistics, planning, and sheer physical work just to pull off a single successful event.

Because you are constantly moving and working in third-party spaces, the risks you face are fundamentally different than a traditional brick-and-mortar restaurant. A restaurant has its hazards mostly contained within its four walls. A caterer carries those hazards onto the highway, into someone else’s expensive property, and right into the middle of large, unpredictable crowds of guests.

When you are looking at catering service insurance, you can’t just buy a generic, off-the-shelf business policy and hope it sticks. You need to look closely at the different phases of your operation—the prep kitchen, the transport, and the actual service at the venue—and make sure the coverage actually lines up with what you are doing.

Here is a straightforward look at how the different pieces of catering insurance work, what they actually protect, and what you need to be thinking about to keep your business safe from the very real things that can go wrong.

The Foundation of Your Coverage

If there is one thing venues and clients care about, it’s this. Before they even let you back your van up to the loading dock, they are going to ask for proof that you have a solid foundation of liability coverage.

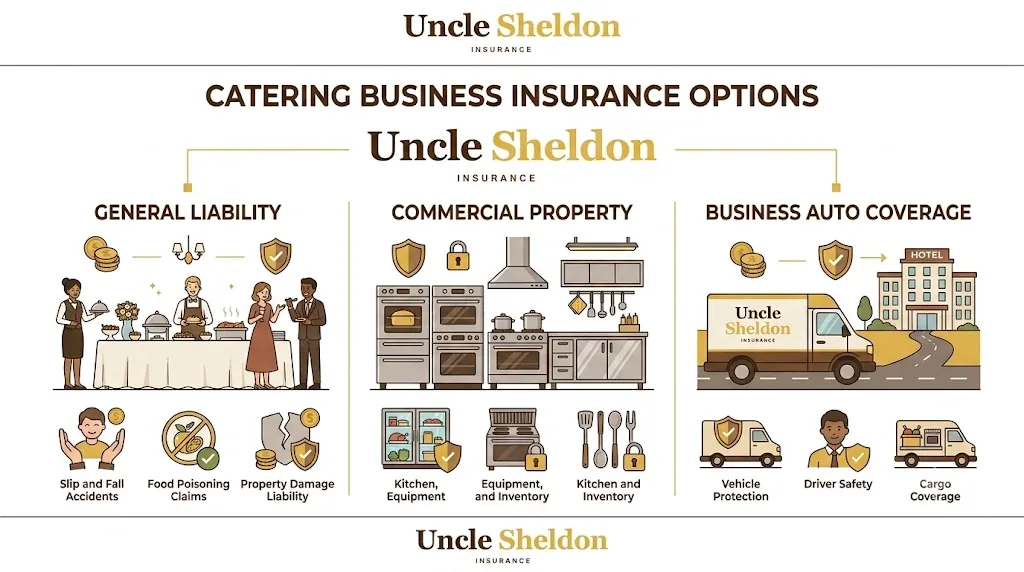

General Liability

General liability is the core policy for basically any business, but for a caterer, it carries most of the weight. It covers you if a third party—meaning a client, a guest, or the venue owner—gets injured or their property gets damaged because of your business operations.

Let’s talk about property damage first, because this is where caterers tend to get nervous. You are constantly hauling heavy equipment, hot food, and liquids through tight doorways, down narrow hallways, and across expensive floors. If one of your servers drops a heavy chafing dish and shatters an antique tile floor in a historic venue, or if a spilled tray of red wine ruins the carpet in a corporate office boardroom, general liability is what steps in to handle the repair and replacement costs. Without it, you are paying out of pocket to fix someone else’s expensive building, which can eat the profit from a dozen gigs in a matter of seconds.

Then there is bodily injury. A classic catering example is a guest slipping on a patch of floor where a server spilled some water near the buffet line. If they fall and break a wrist, general liability covers their medical bills and your legal defense if they decide to sue your business over the injury. You are bringing the hazards into the venue, so you need the coverage to handle the fallout if someone gets hurt because of your setup.

Product Liability

This is usually built right into your general liability policy, and it is arguably the most critical protection you have as a food business. Product liability specifically covers you if the product you sell—in this case, the food—causes actual harm to a customer.

You do everything you can to keep the food safe. You check the temperatures of the meats, you keep the cold stuff cold on ice during transport, and you manage allergens meticulously during prep. But the reality is, foodborne illness and severe allergic reactions do happen, sometimes despite your best efforts. If a batch of chicken isn’t held at the right temperature during a long outdoor summer event and a large group of guests gets severe food poisoning, product liability is the coverage that handles the fallout. It covers the medical claims, the settlements, and the lawyers you will need to defend the business. In the catering world, the risk of serving a bad batch of food to a large group of people is probably the single biggest threat to the survival of the company, making this coverage absolutely essential.

Transporting the Operation

A huge part of your job is just getting the food, the gear, and the staff from point A to point B. This introduces a whole different set of risks that standard property policies just do not cover.

Commercial Auto Insurance

If you use a vehicle primarily for business—like hauling food, staff, and equipment to a venue—you need a commercial auto policy. It is a very common mistake for new caterers to use their personal van or SUV to run the business, assuming their personal auto insurance will cover them if something goes wrong. It won’t. If you get into a wreck while delivering trays of food to a wedding, a personal auto policy will almost certainly deny the claim once they find out you were using the vehicle for commercial purposes.

Commercial auto liability covers the bodily injury and property damage you cause to other people if you cause an accident while driving for work. This is critical because catering vans are heavy, visibility is often poor, and you are usually driving in unfamiliar areas or trying to navigate tight loading zones while under a severe time crunch.

You also need physical damage coverage on that commercial auto policy to protect the van itself. If someone rear-ends you on the highway and totals the catering van, you need that vehicle repaired or replaced fast so you don’t miss the upcoming weekend’s events. The van isn’t just a way to get around; it is a vital piece of the business infrastructure.

Inland Marine Coverage

This is an old insurance term that trips people up, but it basically just translates to “property in transit.”

Your standard commercial property insurance usually only covers your equipment while it is physically sitting inside your designated prep kitchen. But as a caterer, your most expensive gear is constantly on the move. You have commercial coffee makers, expensive chafing setups, portable ovens, POS systems, and thousands of dollars worth of serving ware moving from the kitchen, to the van, to the venue, and back again.

Inland marine coverage protects that equipment while it is away from your primary premises. If someone breaks into the catering van overnight while it is parked outside a hotel and steals your high-end portable espresso setup, or if a rack of expensive custom plates is destroyed in a traffic accident on the way to a venue, inland marine coverage pays to replace it. It bridges the gap between your prep kitchen and the event site.

The Risks in the Prep Kitchen

Whether you own a large commercial kitchen or rent space in a shared commissary, you have significant money tied up in the food and the equipment before it ever leaves the building.

Spoilage Coverage

Caterers buy ingredients in massive quantities. When you are prepping for a 300-person wedding, your walk-in coolers are absolutely packed with expensive meats, dairy, and fresh produce.

If a summer storm knocks out the power to your kitchen for two days, or if the compressor on your main walk-in simply dies overnight, you can lose thousands of dollars in perishable inventory in a matter of hours. Standard property insurance doesn’t usually cover food spoilage caused by mechanical breakdown or power failure. Adding spoilage coverage reimburses you for the cost of the ruined ingredients so you have the cash to go out and restock immediately. It’s a very practical coverage that can literally save a weekend’s profit margin from being entirely wiped out.

Equipment Breakdown

Building on that scenario, what happens when the compressor on the walk-in dies? Property insurance covers external events like a fire destroying the cooler, but it doesn’t cover mechanical failure. If a motor burns out, or an electrical surge fries the control panel on your massive commercial convection oven, standard policies treat that as a wear-and-tear maintenance issue.

Equipment breakdown coverage specifically steps in for those sudden, accidental mechanical or electrical failures. Commercial kitchen equipment is notoriously expensive to repair, and this coverage helps pay for the parts and labor to get your vital appliances running again so you aren’t completely sidelined by a dead motor.

Business Interruption

If a fire damages your prep kitchen and you can’t operate for a month while repairs are being made, the property insurance pays to rebuild the kitchen. But what pays the bills while you are shut down?

Business interruption insurance (often called business income coverage) is designed to replace your lost net income and cover your ongoing fixed expenses—like rent, loan payments, and key payroll—while your operations are suspended due to a covered claim. If you can’t prep food, you can’t cater events, which means the cash flow completely stops. This coverage helps keep the business alive while you get back on your feet.

Protecting Your Team

Catering is a physically demanding job. Your staff is lifting heavy trays, working around open flames and boiling water, and often rushing through unfamiliar kitchens or outdoor spaces in poor lighting.

Workers Compensation

If you have employees, almost every state requires you to carry workers compensation insurance. It covers their medical bills and a portion of their lost wages if they get hurt on the job.

Injuries in catering are incredibly common. A prep cook slicing their hand open while rushing through prep, a server slipping on a wet kitchen floor and tearing a knee ligament, or a team member throwing their back out while loading heavy coolers into the van—these things happen regularly. Workers comp ensures your injured employees get the care they need without bankrupting themselves.

It also fundamentally protects the business. In the vast majority of cases, an employee who receives workers comp benefits cannot turn around and sue the business directly for the injury. It is a crucial safety net for both sides.

One thing to keep in mind is that catering relies heavily on temporary or seasonal workers, especially during the busy summer wedding season. You need to make sure your payroll estimates for workers comp accurately reflect those seasonal spikes so you aren’t hit with a massive surprise audit bill at the end of the year when the insurance company reconciles your actual payroll against what you estimated.

Employment Practices Liability

In a high-stress, fast-paced environment where tempers can flare during a busy service, conflicts happen. Employment Practices Liability Insurance (EPLI) protects the business against claims made by employees alleging wrongful termination, discrimination, sexual harassment, or wage and hour disputes. Defending against an employee lawsuit can cost tens of thousands of dollars in legal fees alone, even if the business did absolutely nothing wrong. EPLI covers those defense costs and any settlements, which is particularly relevant when you are dealing with a constantly rotating roster of part-time and seasonal staff.

The Alcohol Factor

If your catering services include providing or serving alcohol, the risk profile of your business changes significantly.

Liquor Liability

Standard general liability policies specifically exclude claims related to the sale or service of alcohol. If you are just a standard food caterer who drops off sandwiches, this doesn’t matter much. But if you are managing the bar at a wedding, or supplying the beer and wine for a corporate retreat, you need liquor liability insurance.

If a bartender on your staff overserves a guest, and that guest later gets into their car and causes a severe accident on the way home, your business can be dragged into a massive lawsuit under state dram shop laws. The argument will be that you contributed to the accident by serving someone who was visibly intoxicated. These lawsuits can be devastatingly expensive. Liquor liability steps in to cover your legal defense costs and any settlements or judgments against you.

Even if the client is buying the alcohol and you are just providing the bartenders to pour it (sometimes called “host liquor” scenarios), you still carry significant risk. You need to be extremely clear with your insurance provider about exactly what your role is regarding alcohol so they can make sure the right coverage is in place. Never assume you are covered just because you didn’t physically buy the kegs.

Dealing with Venues and Paperwork

One of the most frustrating parts of running a catering business has nothing to do with food—it’s dealing with the administrative hurdles required by venues and event organizers.

Certificates of Insurance (COI)

Basically, any venue worth working at is going to require you to prove you have insurance before you can work there. They will ask for a Certificate of Insurance, or a COI. This is a one-page document from your insurance provider that summarizes your coverage limits and policy dates.

You will be asked for these constantly. A bride will book you six months out, and then a week before the wedding, the venue coordinator will suddenly demand a COI by 5 PM on a Friday. Having an insurance setup where you can easily request and receive these certificates quickly is vital. If your broker takes three days to return a simple email, it is going to cause you massive headaches and potentially cost you jobs.

Additional Insured Endorsements

Venues don’t just want to know you have insurance; they usually want to be protected by it. They will frequently ask to be listed as an “Additional Insured” on your general liability policy.

This means that if you cause a problem at the venue—like a grease fire that damages their kitchen—your insurance policy extends to cover the venue as well, so their own insurance doesn’t have to take the hit. Adding venues as additional insureds is incredibly common in the catering world, but it sometimes costs a little bit of money to add each one depending on how your policy is structured.

Some policies offer a “blanket” additional insured endorsement, which automatically extends this status to any venue that requires it in a written contract. If you work at dozens of different venues a year, a blanket endorsement can save you a lot of time and administrative hassle.

Figuring Out What Makes Sense

Putting together the right coverage for a catering business isn’t about buying the most expensive policy out there. It’s about being realistic about what can actually go wrong when you are hauling food, heavy equipment, and stressed-out staff all over the city.

You need to look hard at your specific operation. Are you doing high-end weddings with massive setups, huge guest counts, and a full bar staff? Or are you doing drop-off corporate lunches where you just leave the food in the breakroom and walk away? The risks are completely different, and your insurance should reflect that reality.

Take a close look at your deductibles as you build the policy. A higher deductible will lower your monthly premium, but you have to be completely honest about your cash flow. If coughing up a $2,500 deductible to fix a broken walk-in cooler would severely stress the business, it might be better to pay a slightly higher premium for a $500 deductible so you have more predictability when things break.

The catering business is unpredictable enough as it is. You deal with bad weather, demanding clients, traffic jams, and equipment that decides to quit at the worst possible moment. Getting the insurance sorted out is just a way of putting a solid floor under the business, making sure that when the unexpected does happen, it’s just a frustrating day to deal with, and not something that threatens everything you’ve worked so hard to build.